FX Daily Strategy: APAC, October 15th

ECB meeting to deliver expected rate cut

EUR/USD risks still on the downside

UK data to support weaker GBP tone

JPY to remain soft in the absence of news

Focus on UK labour market data and Canada CPI

GBP risks on the downside as market has scope to price in more UK easing

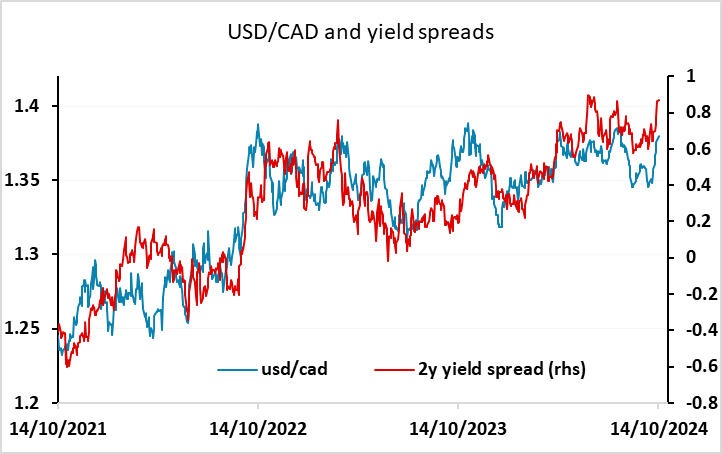

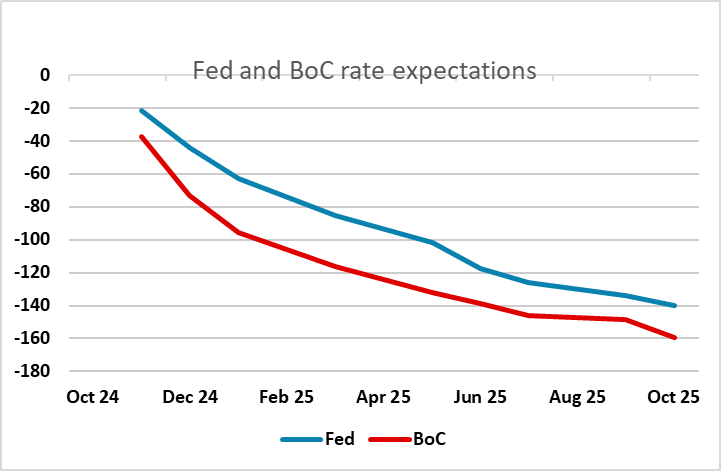

USD/CAD currently biased higher…

…but stronger CPI data may turn the trend

After a quiet Monday with the US, Canada and Japan on holiday, Tuesday offers a little more to go on with labour market data in the UK and CPI data in Canada. UK labour market data may show a fresh rise in the jobless rate and higher inactivity, but there will be as much weight on HMRC numbers regarding job dynamics which have suggested clearer slowing in private sector employment, if not an actual contraction. However, the average earnings figures will be the most closely watched. We see a further slowing in both regular pay growth (3 mth mov avg) down to 4.8% and the headline rate down to around 3.7 % on base effects.

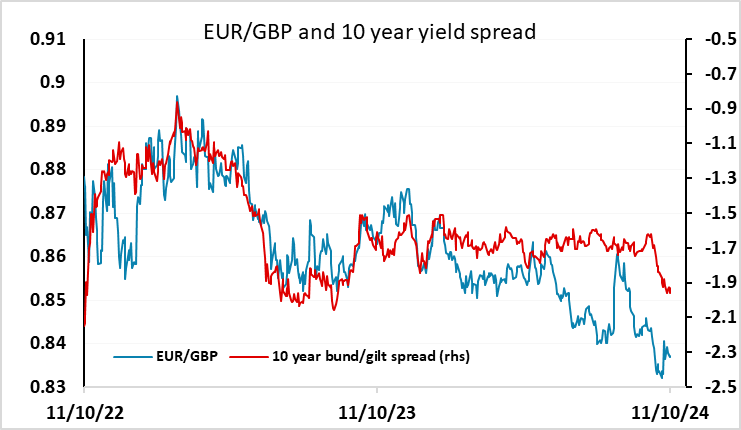

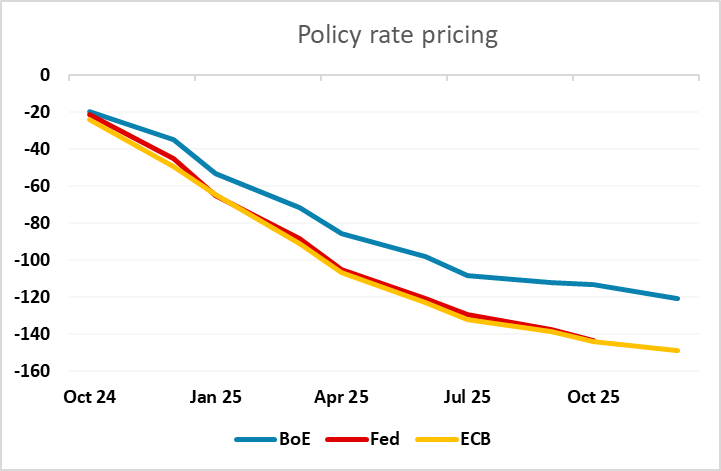

Regardless, with even the BoE (belatedly) casting doubt on the validity of these numbers, more attention may be paid to the PAYE pay data where a clear(er) slowing may be on the cards. We continue to see scope for the market to increase expectations of UK rate cuts to be more in line with the profile expected in the US and Eurozone, which would suggest EUR/GBP upside risks from here. EUR/GBP looks to have established a base near 0.83, and with the pound expensive against the EUR by historic standards, and yield spreads having scope to narrow, we see most of the risks on the upside. But even though the labour market data may in reality be more important for policy than the CPI data, the market may be reluctant to react too much ahead of Wednesday’s September CPI data.

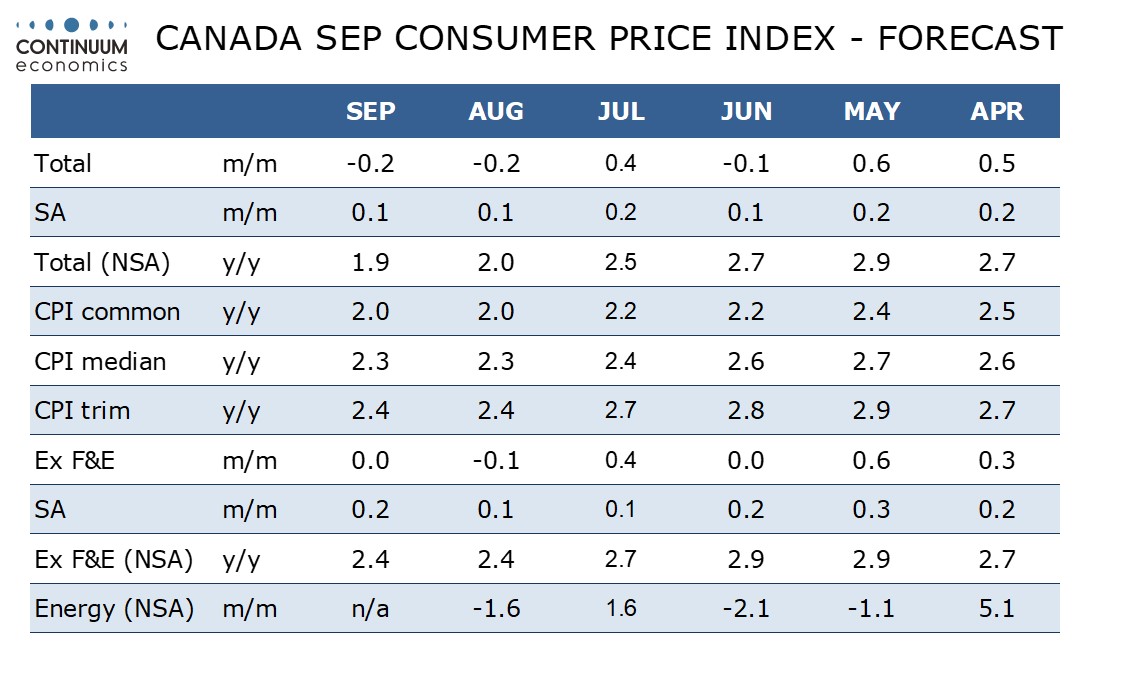

We expect September Canadian CPI to slip to 1.9% yr/yr from 2.0% on weaker gasoline prices, reaching its slowest since February 2021. However we expect the downtrend in the Bank of Canada’s core rates to see a temporary pause as weak data a year ago drops out. Seasonally adjusted we expect a second straight 0.1% increase on the month overall with a 0.2% increase ex food and energy, the latter slightly stronger than 0.1% gains seen in July and August but still acceptably subdued. Before seasonal adjustment we expect CPI to fall by 0.2% overall with an unchanged outcome ex food and energy.

Our forecasts are broadly in line with the market consensus, and are unlikely to significantly change market expectations of BoC policy. As it stands, yield spreads have moved in the USD’s favour as market expectations of a 50bp Fed easing in November have been priced out of the market, but the market still sees next week’s BoC meeting as a 50-50 call between a 25bp and a 50bp cut. After the strong employment report last week, the risks have likely shifted towards a 25bp move, and if inflation surprises on the upside there is now probably more risk of consensus shifting to 25bps than it shifting to a 50bp move on a softer number. Even so, with spreads currently suggesting upside risks for USD/CAD it might take stronger data to prevent a move above 1.38, even though these levels do look like good long term buying levels for the CAD.