ECB Doves Coo Louder?

That high-profile ECB Council members are now talking both more clearly and openly about possible near-term rate cuts is of little surprise. It does fit in with both what was said and that was not said after last week’s Council press conference. Not least are week-end comments made by BoF Governor Villeroy de Galhau told a French newspaper that the ECB could cut interest rates at any moment this year and all options are open at upcoming meetings. His Portuguese colleague Mario Centeno was also open in calling for lower rates sooner rather than late, suggesting acting sooner would allow the ECB to ease more gradually. This is the start of a more active and open debate among ECB Council members about policy, prompted by the speedy manner in which inflation has fallen and the proximity of headline HICP inflation returning to target – in m/m adjusted terms it is already well below.

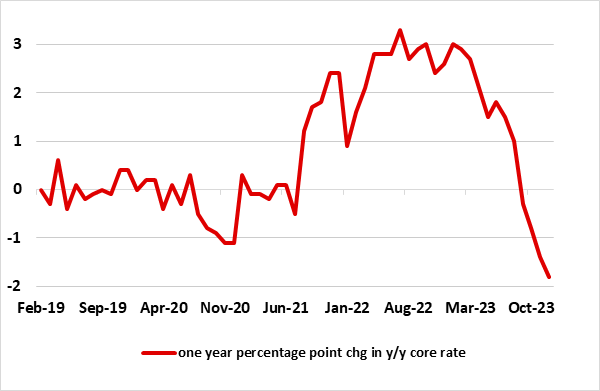

Figure 1: Inflation Fall is Faster than the Rise

Source: Eurostat, CE

While President Lagarde may have said last week that the Council regarded to be premature to discuss easing, this apparently was only by consensus, implying a minority wanted such a debate. In this regard the French and Portuguese Council members are very likely to have been in that minority and have enough confidence in the disinflation process to be vocal and open about their policy preferences. This is not surprising given the manner in which important data is both highlighting an ever clearer disinflation process. Indeed, disinflation (most notably for core rates, Figure 1) has actually been faster than the previous surge in inflation, questioning the empirical relevance of the “last mile” narrative that many central bankers have been highlighting.

Therefore this may be why last week’s ECB meeting made only a half-hearted attempt to redirect market speculation about official rate cuts. Thus, the ECB hierarchy still points to rates being at levels that maintained for a sufficiently long duration will return inflation to target and that policy rates being at sufficiently restrictive levels for as long as necessary. But ‘sufficiently long’ and ‘as long as necessary’ are vague, the question being whether this rhetoric is being adhered to because it does provide the ECB some policy flexibility to be as data dependent. Indeed, it does seem as if the ECB is already accepting the kind of ever clearer and broader disinflation process it needs in order to consider reversing policy.

President Lagarde has suggested rate cuts may occur in the summer, chiming with an interview from Chief Economist Lane who implied the June meeting will be critical. We still think that cuts may arrive sooner, ie starting in Q2, although we still pencil in no more than 100 bp cuts this year to be followed by a similar sized fall in 2025. It may very well be the case that the ECB starts to agree that early easing would allow it to proceed more gradually and therefore assess how durable the disinflation process is faring. And early easing would also have to be assessed against the backdrop and outlook of the ECB continuing to shrink its balance sheet, most notaby via bond sales.

Possible Policy Timetables

As for possible timetable, the ECB may have to paint a bleaker real economy picture and softer inflation outlook in its updated projections due at the next scheduled Council meeting on March 7. These could pave the way of a rate cuts at either of the scheduled policy meeting in Q2 (ie April 11 or June 6). But over and beyond calling an emergency meeting there are also a series of other hitherto scheduled non policy meetings at which a monetary policy decision could be made. Indeed, headline HICP inflation may already be at, or a touch below, target by that April meeting, a development that would almost cement an immediate response.