ECB Review: Half Hearted Defence of Policy?

Unsurprisingly this latest ECB meeting was not notable for what the Council did but rather what is said. This third successive stable policy decision was unambiguously expected as was the more formal attempt to redirect market thinking that still prices 50 bp rate cutting by mid-year. Thus, it still points to rates being at levels that maintained for a sufficiently long duration will return inflation to target and that policy rates being at sufficiently restrictive levels for as long as necessary. But ‘sufficiently long’ and ‘as long as necessary’ are vague, the question being whether this rhetoric is being adhered to because it does provide the ECB some policy flexibility to be as data dependent as it boasts it is. Indeed the attempt to rein in market thinking was half-hearted, not least as the Q&A was almost explicit in suggested that all the ECB needs it see is an already ever clearer and broader disinflation process continuing before it considers reversing policy.

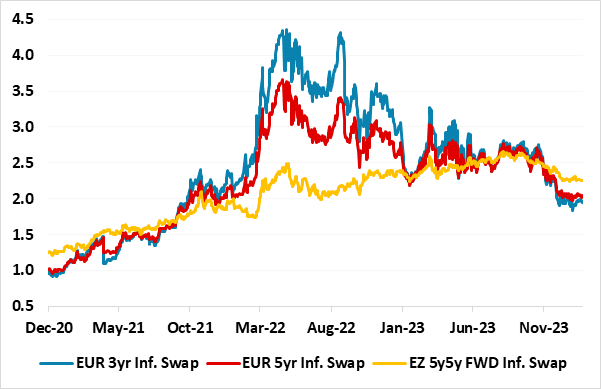

Figure 1: Inflation Expectations Falling

Source: Bloomberg

President Lagarde has suggested rate cuts may occur in the summer, chiming with an interview from Chief Economist Lane who implied the June meeting will be critical. We still think that cuts may arrive sooner, ie starting in Q2, although we still pencil in no more than 100 bp cuts this year to be followed by a similar sized fall in 2025.

Possible Policy Timetables

As for possible timetable, the ECB may have to paint a bleaker real economy picture and softer inflation outlook in its updated projections due at the next scheduled Council meeting on March 7. These could pave the way of a rate cuts at either of the scheduled policy meeting in Q2 (i.e. April 11 or June 6). But over and beyond calling an emergency meeting there are also a series of other hitherto scheduled non policy meetings at which a monetary policy decision could be made. Indeed, headline HICP inflation may already be at, or a touch below, target by that April meeting, a development that would almost cement an immediate response.

Markets Winning in the Battle?

It does seem as if the ECB is finding difficult to battle against market expectations that factor in almost 150 bp of easing in the coming year. Indeed, rate cut discussions have taken place given the manner in which a summer timetable has already surfaced. While President Lagarde may have said today that the Council regarded to it premature to discuss easing, this was only by consensus, implying a minority wanted such a debate. This not surprising given the manner in which important data is both highlighting an ever clearer disinflation process and underscoring the manner in which policy tightening is still biting.

As for the former, the ECB noted the clear fall in inflation expectations (Figure 1), actually no longer citing such expectations as an upside risk to the inflation outlook. It also accepted that its own wage tracking pointed to a stabilization, if not an easing, in such costs pressures, this accentuated by more signs that such pressures were also being absorbed more by companies cutting profit margins. All of which came alongside clear acknowledgement that underlying inflation was falling.

The Last Mile Issue

As for policy tightening, it was again noted that past interest rate increases keep being transmitted forcefully into financing conditions, this evident in the manner in which the bank lending survey was still seeing credit standards being lifted. It was also noted that tight financing conditions are dampening demand, and this is helping to push down inflation, this possibly an implicit admission that supply factors are also contributing. And as the ECB meeting in December then noted that when looking at the annual inflation data for the last few years, it appeared that disinflation to date had actually been faster than the previous surge in inflation, questioning the empirical relevance of the “last mile” narrative that many central bankers have been highlighting.

Overall, despite what it regards are less downbeat real economy signs, it still sees growth risks being (justifiably) tilted to the downside. But it is deliberately vague as to where the balance of inflation risks lie. We think they have surprised to the downside and will continue to do, not least as we would regard a good portion of disinflation as supply driven and that with policy hikes still biting the impact of weak demand will only accentuated this.

Inflation Dynamics Ever Friendlier

But the inflation numbers are already making us more confident that the headline rate may fall to below the 2% target in Q2, thereby corroborating a disinflation trend already evident in seasonally adjusted m/m core and headline numbers, data we have been flagging for some time. And it does seem as if the ECB is starting to use such numbers as the Dec account mentions, albeit using a 3 month on 3 month annualized measure that very much lags the more coincident 3 month moving average we prefer. In this regard, it is notable that the ECB acknowledged that these were often better predictors of future inflation than annual growth rates and had already pointed to below target inflation.