This week's five highlights

2-Week Ceasefire, Then?

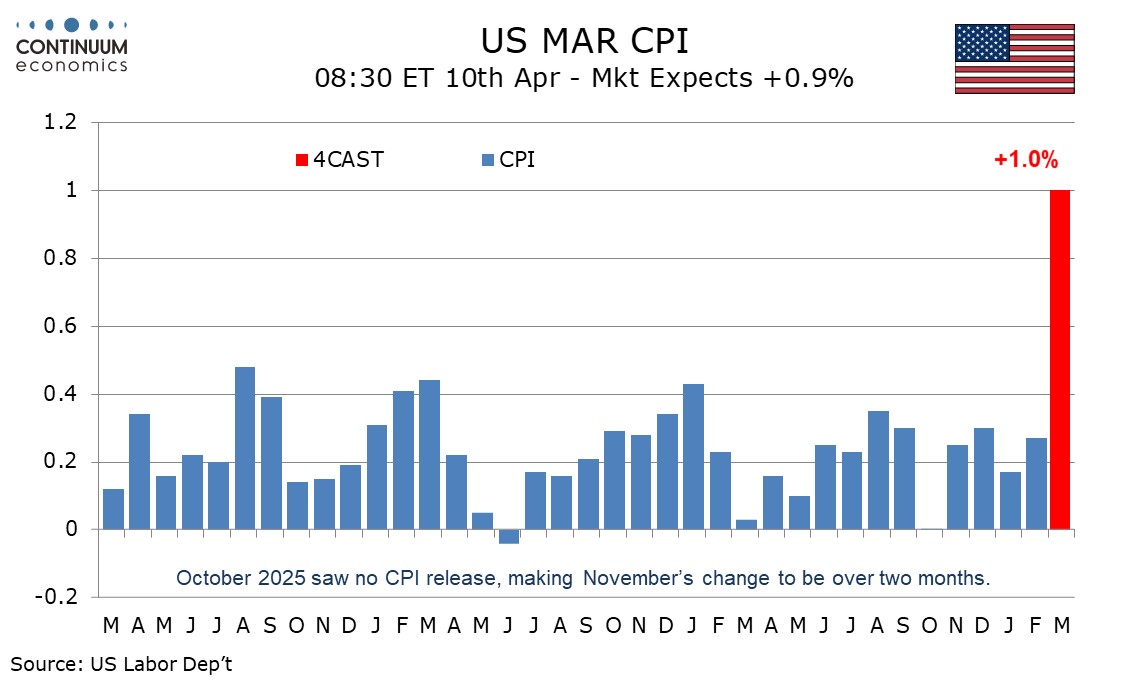

U.S. March Energy to surge in CPI

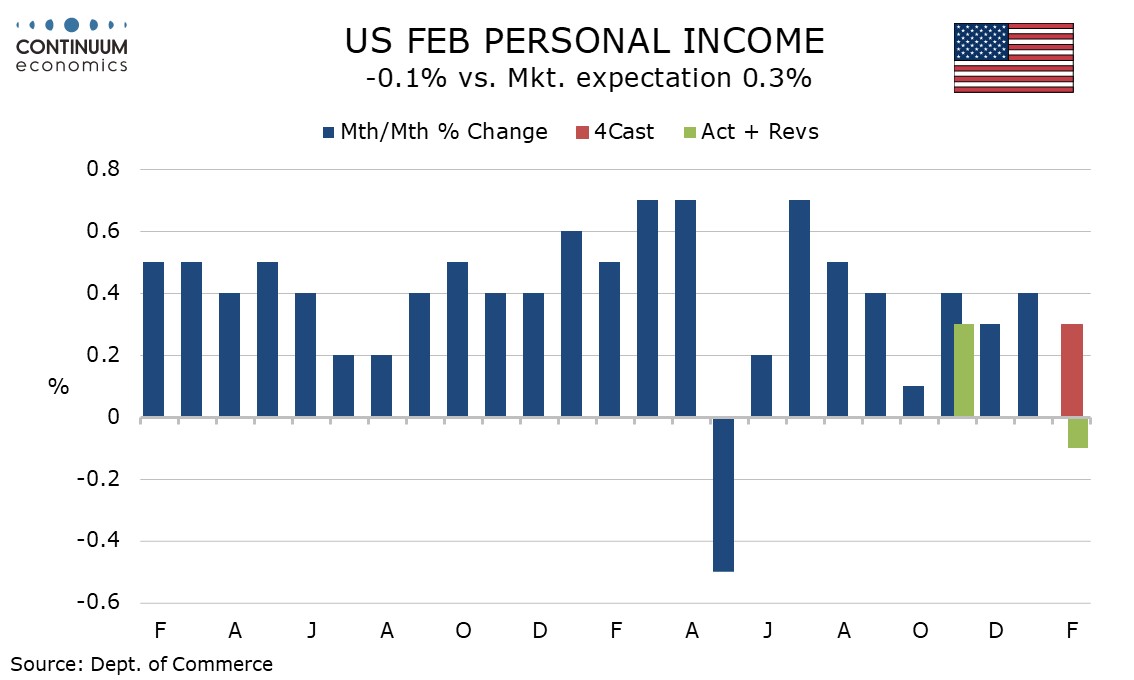

U.S. Personal Income slips, Core PCE Prices remain firm

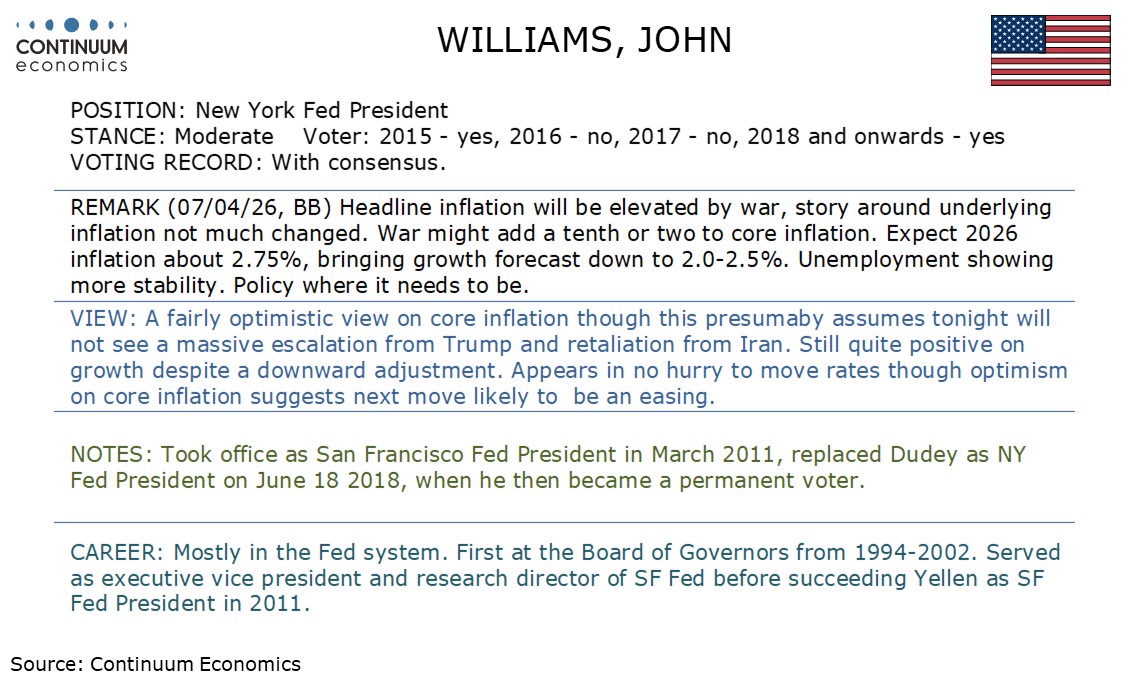

This Week's Fed Speakers

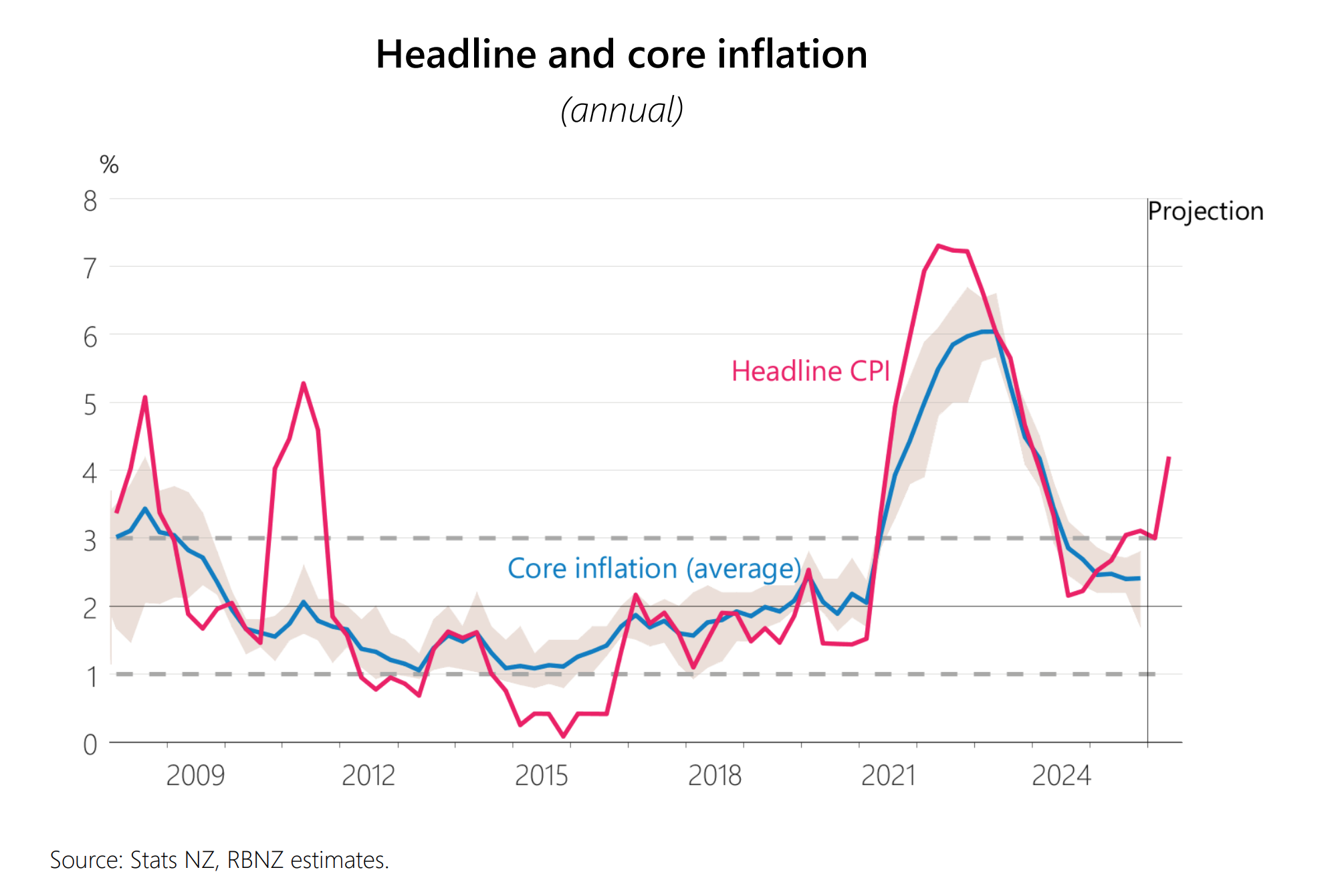

RBNZ Inflation Forecast Revised Higher

Figure : Iran Key Issues

| Issue |

| The lifting of all primary and secondary sanctions on Iran. |

| Continued Iranian control over the strait of Hormuz. |

| U.S. military withdrawal from the Middle East. |

| An end to attacks on Iran and its allies. |

| The release of frozen Iranian assets. |

| A UN security council resolution making any deal binding. |

Source: Media sources from Iran, US, Pakistan

The ceasefire will likely involve a new normal of shipping companies paying Iran a toll. While this is adding a cost to Gulf crude oil/products and LNG, the premium will be a lot lower than the cost of an ongoing war. The U.S. and Iran will now likely be reluctant to restart the war, which suggests that the ceasefire will likely be extended. However, it is difficult to see a comprehensive peace deal, given that the sides remain so far apart on some key issues. Iran will also use the threat that a future attack from the U.S. or Israel in the future will trigger closure of the Strait of Hormuz to get the U.S. to stop Israel at least for the next 6-12 months. This could all mean a further gradual reduction in the risk premium for global oil/oil products/LNG and Urea fertilizers in the coming weeks. This also reduces the risk of 2nd round inflation effects and central banks having to hike.

While both sides are claiming victory in the PR war, the ability to agree a 2-week ceasefire is important. We have argued that president Trump has been looking for an off ramp, given the war impact on gasoline prices and his falling popularity rating before the key November midterm elections. However, Iran’s decision to accept Pakistan’s proposal for a 2-week ceasefire is their first major compromise and suggested Iran now sees merit in negotiating and stopping the hostilities. Though Iran has been hurt severely from a military viewpoint, it has demonstrated leverage in the Straits of Hormuz and via asymmetric attack on Gulf countries.

We expect March CPI to surge by 1.0% overall, which would be the strongest rise since June 2022, seen in the aftermath of the Russian invasion of Ukraine. However we expect only a moderate increase ex food and energy, of 0.22% before rounding, which would match that seen in February. Even with some restraint from seasonal adjustments, gasoline prices look sure to see a sharp surge, which will explain nearly all of a 12.5% increase in energy, with most other components of the energy breakdown likely to seen only modest changes. We expect a moderate 0.3% increase in food, but there are upside risks going forward with the closure of the Strait of Hormuz disrupting fertilizer supplies.

Ex food and energy data has been showing a loss of momentum in recent months, with trend now looking close to 0.2% per month and even January at 0.3% not showing as strong a new year bounce as did most recent years. However PPI, some of which impacts core PCE prices, has been showing some acceleration even before the energy shock.

The latest US data is mostly on the weak side of expectations, most notably a 0.1% decline in personal income for February that significantly underperformed a 0.5% rise in spending (itself slightly below expectations) which saw the savings rate slip back after a tax cut-assisted bounce in January. 0.4% gains in overall and core PCE prices are as expected but too high. Initial claims corrected higher but continued claims are down, while Q4 GDP was revised even lower, to 0.5% from 0.7%.

The personal income detail shows a 0.2% rise in wages and salaries, below trend as was February’s non-fark payroll. Causing overall personal income to fall were significant declines in dividend income and benefits from Affordable Health Care enrollments. Disposable income was supported in January by lower taxes. The flip side of lower taxes is lower benefits. Real disposable income fell by 0.5% after a 0.6% increase in January. Personal spending was supported by strength in February retail sales already released, led by autos which rebounded from a weak January, but service spending rose by only 0.3%, weaker than expected and up only 0.1% in real terms. The savings ratio at 4.0% is back near Q4 levels after a bounce to 4.5% in January.

The RBNZ kept rates unchanged at 2.25% in the April meeting and has revised their inflation forecast. They see crude oil price below 100 USD/b by the end of June, which led to their inflation forecast for March to be just 3% y/y and 4.2% y/y in June. It is interesting we are not seeing a hawkish tilt from the RBNZ with 4.2% y/y CPI expected. They are downplaying such with weak demand and spare productive capacity.