This week's five highlights

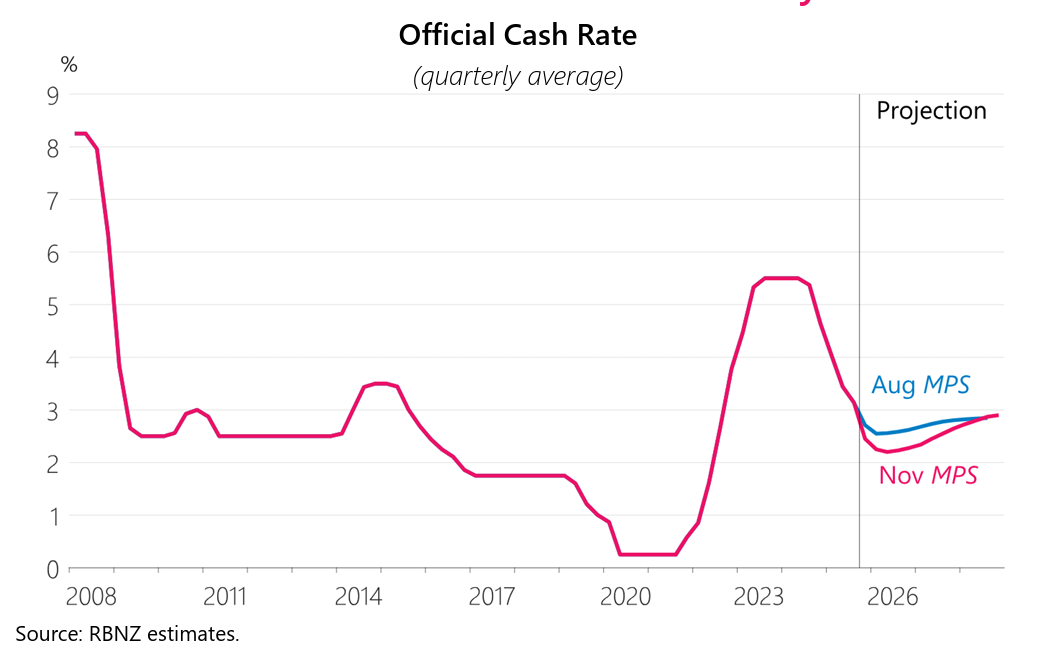

No More Cut Signaled by RBNZ

More Detail on Japan Stimulus

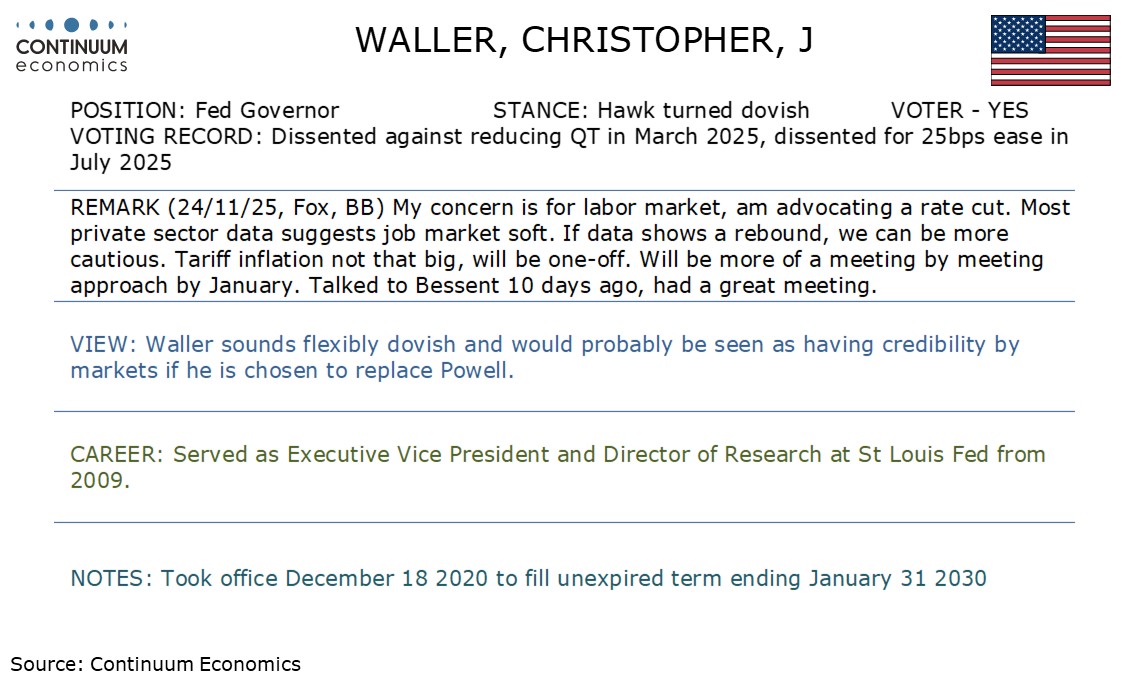

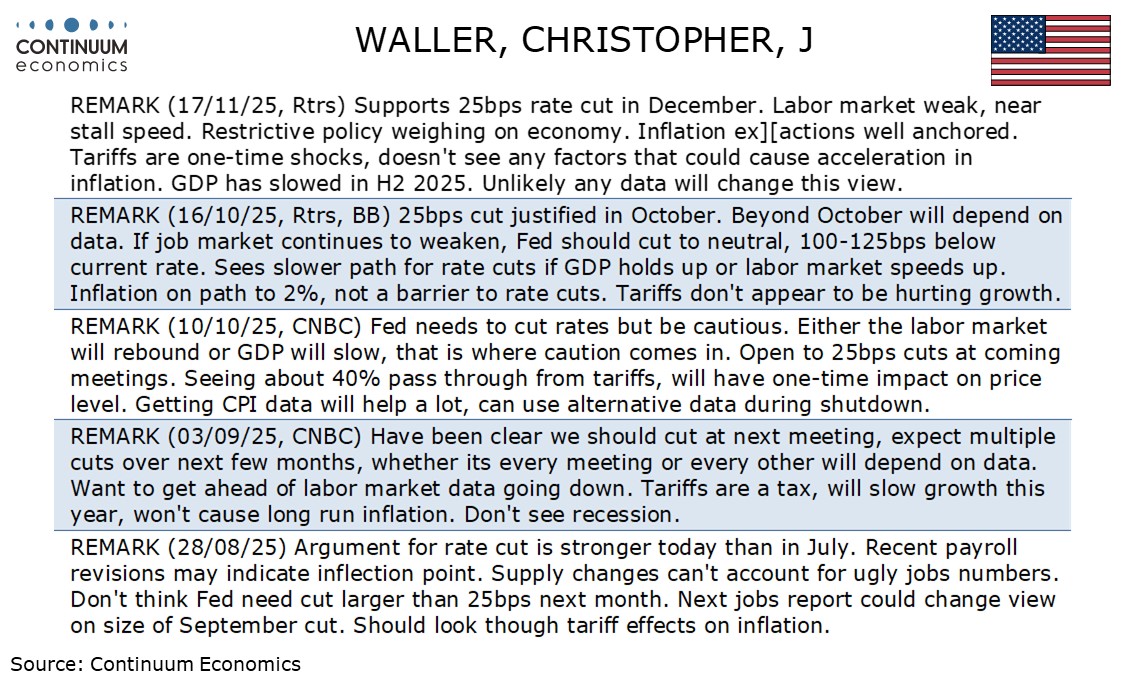

U.S. Fed's Waller Advocating ease on labor market concerns

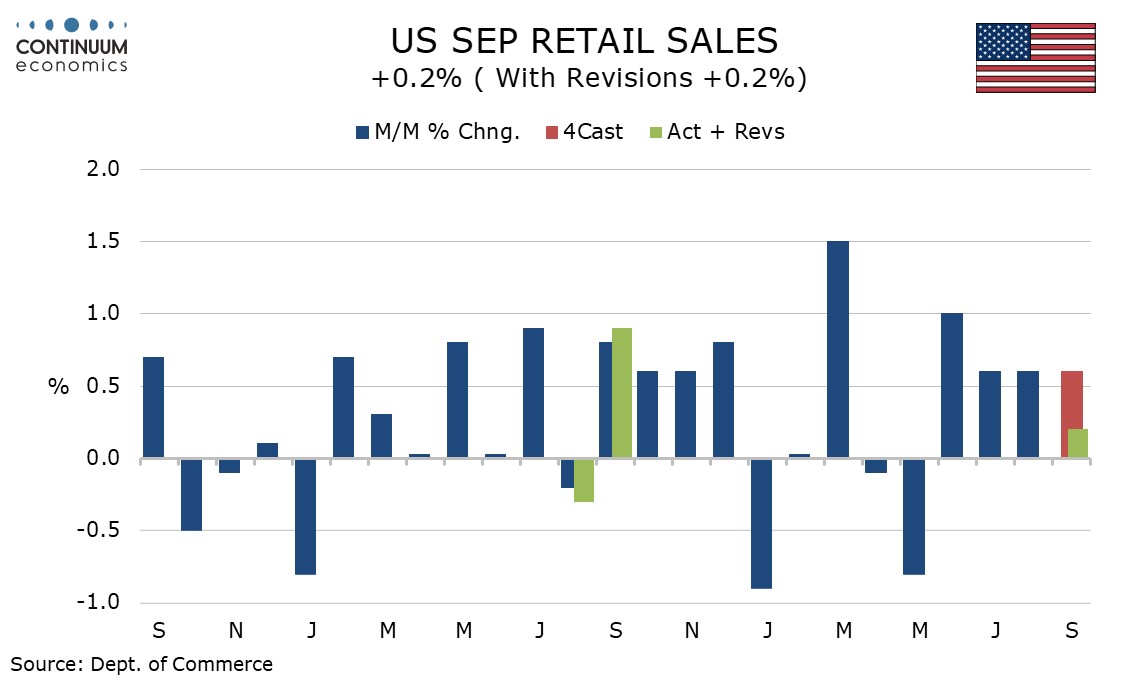

U.S. September Retail Sales lose momentum, PPI strong in goods but weak in services

UK Budget Shows Deferring the Fiscal Pain

The RBNZ cut its cash rate by 25bp to 2.25% in the November meeting and signal there will be no more rate cut. The RBNZ downplayed the spike of Q3 CPI by transitory factors and expect inflationary pressure to ease back towards mid point of target range in 2026. The OCR forecast is seeing no more rate cut from the current 2.25% and first rate hike in late 2026, a pace slightly sharper than August OCR forecast. The reason for RBNZ's 25bps cut seems to be slow economic recovery from U.S. tariffs and geopolitical uncertainty.

Some key takeaways:

Inflation Expectation: As previewed in the October meeting, Q3 CPI is at the top band of target range but is not bothering the RBNZ. They attributed the spike in inflation to "higher tradables inflation along with high inflation in household energy costs and local council rates", factors that are deemed to ease in 2026. Their forecast see inflation to moderate towards the mid point of target range in 2026.

Spare Capacity & Economic Recovery: The RBNZ highlight "spare capacity" in their statement again. They continue to see economic activity in New Zealand being weak. While tariffs and broad geopolitical uncertainty curbed economic recovery, the RBNZ believes the weakness has been overstated from seasonal adjustment.

Slowing Outlook: The RBNZ believe the global economic outlook will slow in 2026 after the AI boom in 2025. Thus, the risk to outlook has tilted towards balance.

Japan PM Takaichi announced the largest stimulus package since COVID at ¥21.3 trillion, an even higher number than first proposed. As we have previewed, the stimulus package is going to include energy subsidies (¥7,000 per household and no tax for gasoline), parental cash handout (¥20,000 per child) and rice coupons (¥3,000 per person). Such cost relief measures are targeting the dissent of LDP from rising living cost, especially for rice coupons. However, what has not been covered, is the promise to drive wage growth from SMEs. To drive inflation target to be reached sustainably, the input from SMEs are critical and they seem to be hanging onto the wind for now. The Japanese government is also establishing a 10yr fund for shipbuilding and other critical areas like A.I. & chips.

PM Takaichi is expected to propose a supplementary budget of ¥17.7 trillion. While there will be partial funds coming from the special account, it is likely trillions will need to be raised through debt issuance. We will see how it plays out as Takaichi is calming market by suggesting new debt issuance will not exceed the one in last year. Even if Takaichi get it through the scrutiny, it will still need to face parliamentary vote where we could see more political compromise from the LDP to its coalition partner.

September retail sales with a rise of 0.2% are weaker than expected and likely to be negative in real terms, given September gains in CPI goods prices, suggesting momentum in consumer spending is starting to fade with employment growth. September’s PPI with a rise of 0.3% overall met expectations but the core rate ex food and energy was subdued at 0.1%.

September’s CPI showed commodity prices up by 0.5% for the second straight month, so August’s 0.6% rise in retail sales was marginally ahead of prices, but September’s 0.2% rise fell short. Sales increased by 0.3% ex auto but only 0.1% ex auto and gasoline, with the control group which contributes to GDP falling by 0.1%.

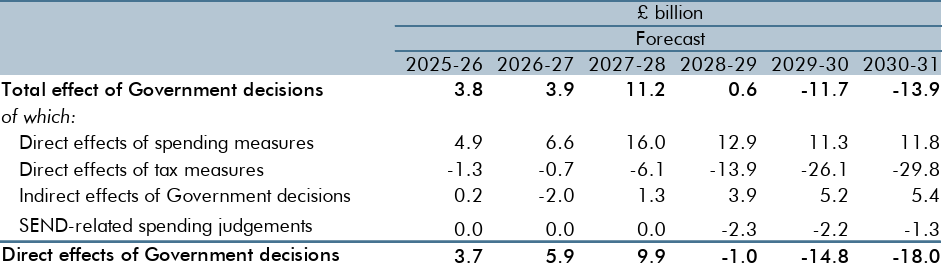

Figure: New Fiscal Measures see Tightening only from 2028!

The Budget looks something of a fudge, with no fiscal tightening until 2028 suggesting policy changes very much back-loaded (Figure) and puzzlingly timed to take effect in what may be the lead-up to the next general election. The immediate the result is actually a modest boost to GDP growth in the near-term. This provides no added pressure on the BoE to ease over and beyond the alleged damage to sentiment that the protracted and still uncertain fiscal picture allied to an already seemingly weaker demand outlook. Markets may take some solace from the fact that, despite the lack of front-loading, the eventual fiscal tightening still creates added fiscal headroom of over twice that previously in place. But, while welcome, this is still historically small and partly dependent on assumed additional tax rises. Moreover, with what still seem optimistic OBR economic forecasts, the government debt ratio may continue to rise, as the OBR estimates it still does on the more familiar measure excluding the impact of the BoE.