AI Optimism and Credit Markets?

· The AI trade in financial markets is also a question of credit markets, given the scale of financing needs is using up hyperscalers free cash flow at a rapid rate and the AI labs heavy financing requirements. Credit markets could become more sensitive, if the AI labs revenue growth slow or any of the hyperscalers freeze high CAPEX in the quarterly result season. Credit market reluctance to fund only short to intermediate bonds for certain issuers would be a bad sign and could cause spill over to produce profit-taking on risk in other sectors of the market.

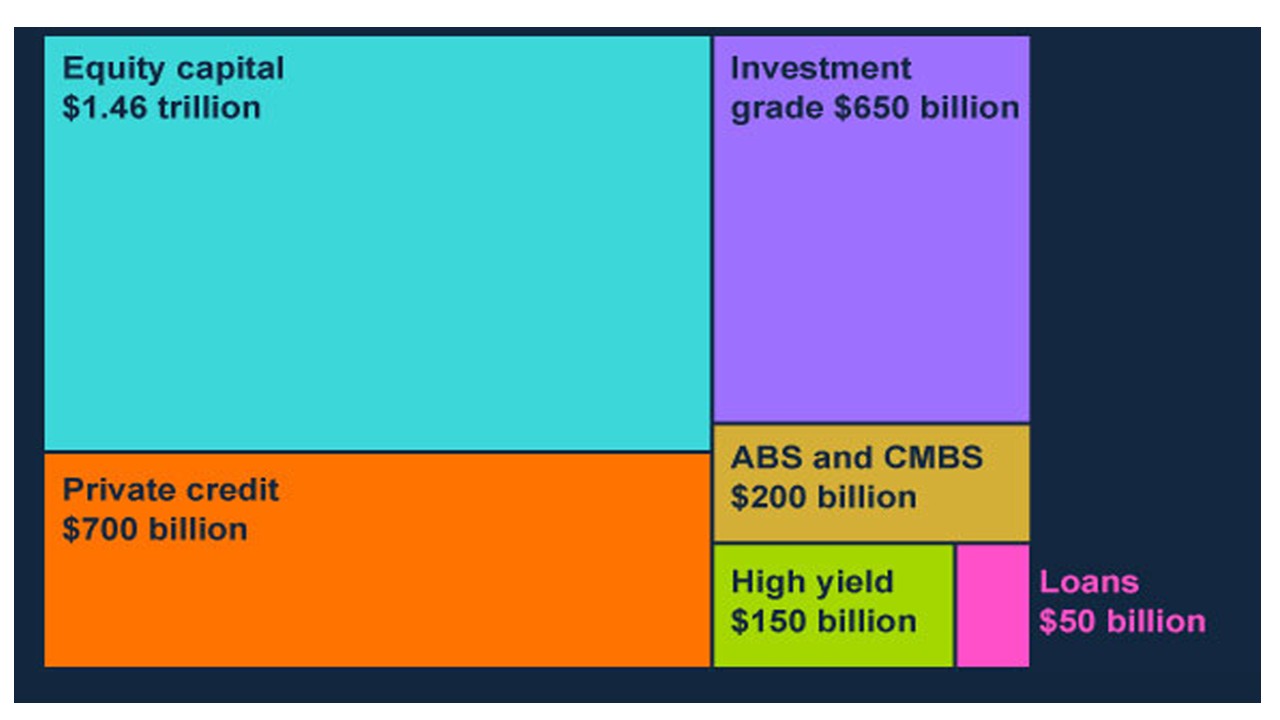

Figure 1: Estimates of funding sources for data centre capital expenditure (2026–28)

Source: BOE financial stability report/Morgan Stanley (here)

The AI trade in financial markets is running into intermittent profit-taking in equity markets, but this is largely profit-taking after a great run up since the Iran war lows. The base optimism remains in the U.S. equity market that AI will be transformational, with the key near-term metric being the AI labs enterprise revenue. This has been explosive in H1, but the equity market is watching closely in H2 with some corporate enterprise AI users reported to be looking to control surging AI token bills. If momentum in AI labs revenue remains strong, then equity market optimism will remain in place. Even so, we noted recently (here), the declining free cash flow of the hyperscalers and variability in AI labs revenue v financing requirements can cause more intermittent profit-taking phase in the equity market. For now, we maintain a forecast of 7800 for the S&P 500 for end 2026 (here).

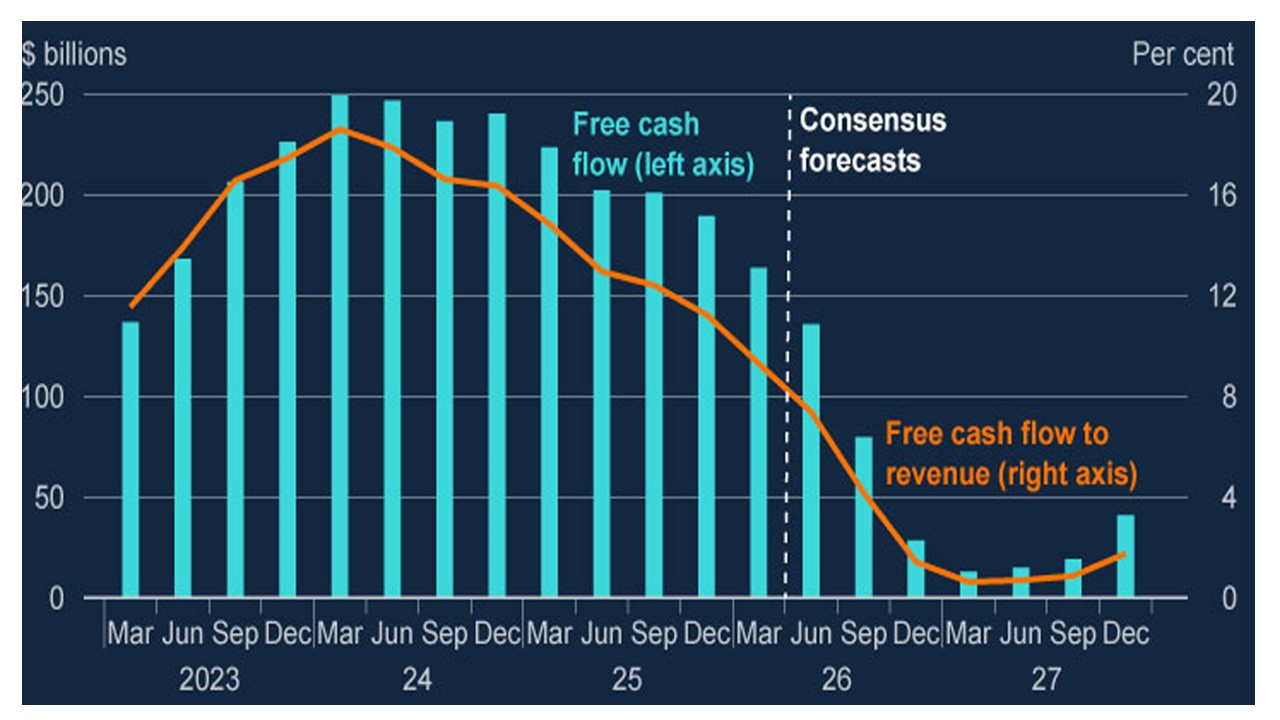

However, the AI trade in financial markets is also a question of credit markets, given the scale of financing needs is using up hyperscaler free cash flow at a rapid rate (Figure 1 and 2) and the AI labs heavy financing requirements. 30yr yield spreads versus U.S. Treasuries have already started to widen for some issuers given the credit market is more sceptical about long-term growth model estimates, while Space X bonds have increased in yield since placement. Credit markets could become more sensitive, if the AI labs revenue growth slow or any of the hyperscalers freeze high CAPEX in the quarterly result season. Generally hyperscalers have conservative balance sheets, but credit fund managers will be focused on 2nd tier AI labs (e.g. Space X) of hyperscalers with more debt (e.g. Oracle). Credit market reluctance to fund only short to intermediate bonds for certain issuers would be a bad sign and could cause spill over to produce profit-taking on risk in other sectors of the market.

Figure 2: Unlevered free cash flow (bars, left axis) and free cash flow to revenue (line, right axis) for the AI hyperscalers

Source: BOE financial stability report/Morgan Stanley (here)