AI Boom and Bust?

• While some are becoming wary that AI bust could arrive in coming quarters, AI labs revenue growth has been explosive and this sustains the vertical chain of datacenter demand and commitments for the hyperscalers and also buoyant semiconductor demand. For 2027 and 2028 capital markets requires U.S. and global corporates to continue to adopt AI enterprise models at a quick growth pace to grow AI labs growth and trickle down the vertical AI chain.

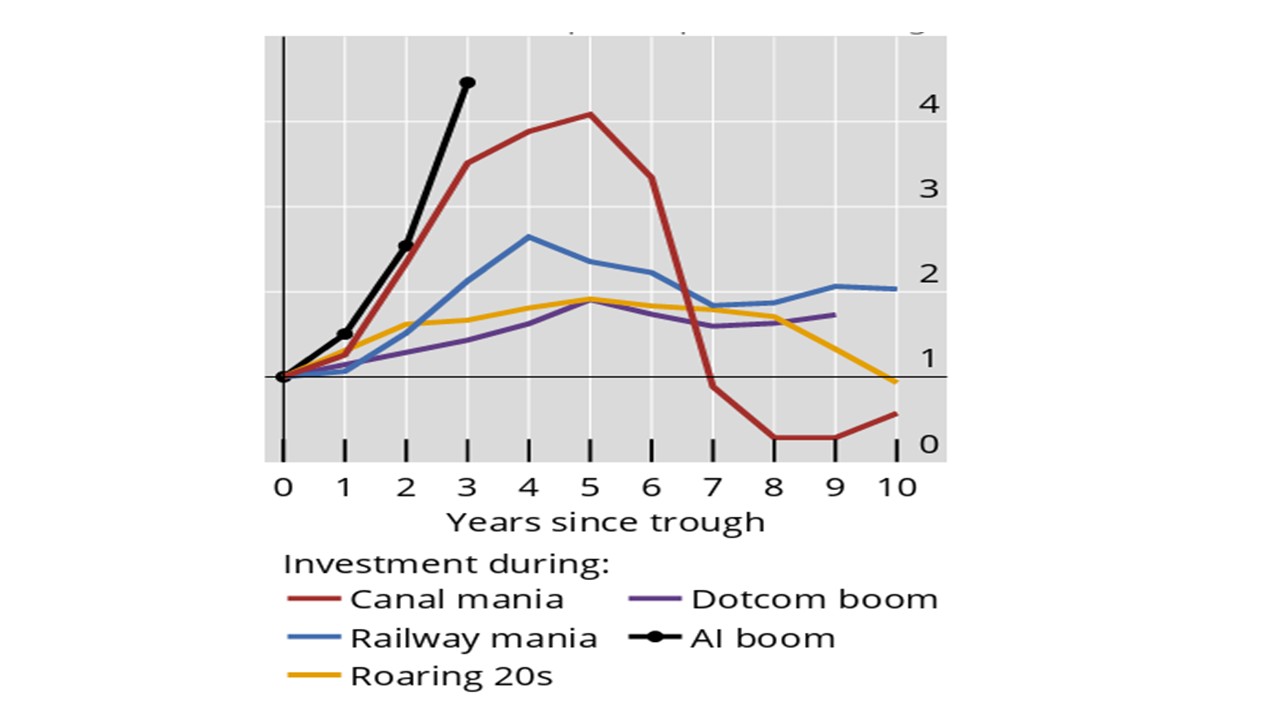

Figure 1: Investment Multiple of pre-boom trough

Source: BIS Annual Report

Question about whether the explosive growth trajectory of AI labs will be sustained at the recent rapid pace has arisen, after some U.S. large scale corporates have curtailed the scale of AI buildout on the basis of cost increases e.g. Walmart/Uber. This has seen hyperscalers equities soften versus semiconductors in June, with the view being that the AI infrastructure buildout could benefit semiconductors more than the hyperscalers or AI labs.

Much pivots on AI labs revenue growth which has been explosive for Anthropic in 2026 (reported to be up 500%), with Open AI also seeing rapid growth. With Space X having floated on AI hype, Anthropic and Open AI are keen to float into the autumn. Initially this could see renewed AI hopes, but then quarterly reporting from the three AI labs will likely see volatility in revenue growth and more clarity and worries on funding needs. This can make the AI trade more volatile than a focus on the quick cash flow benefits that have accrued to the AI infrastructure builders including semiconductor companies. In turn this could mean more corrections in the tech sector in the U.S. equity market and associated sectors in Taiwan/S Korea/Japan and China.

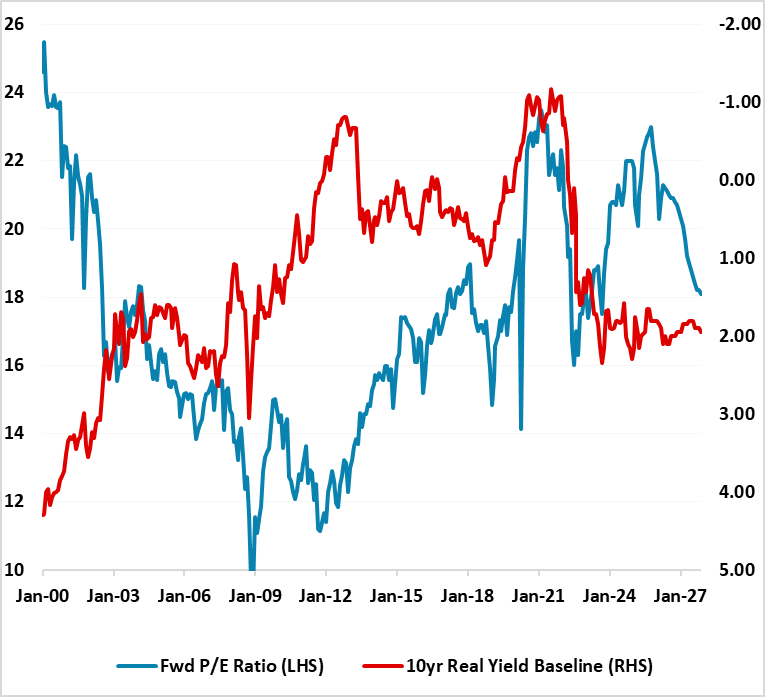

However, volatility in itself does not mean the end of the AI boom, which is dependent on the more fundamental metric of AI labs revenue growth. We remain wary of Space X, given it’s AI model has lagged. This places the focus on Anthropic and Open AI and their continued revenue growth in the coming quarters and years. While a hiccup in growth rates could cause an equity market correction, an AI bust would likely require AI labs revenue growth to slow dramatically from the current heady pace. No signs currently exist of a such a dramatic slowing. Even so, the bears worry that this could be an event risk in 2027, 2028 or beyond. The BIS annual report estimates that the AI boom as a bigger multiple of pre boom investment than other major technology boom (Figure 1). A sharp stalling of AI labs revenue growth would raise questions about their heavy losses/future funding and ability to meet datacentres commitments provided by the hyperscalers. In turn this would hit future demand expectations of the semiconductor sector. This could all prompt a deep correction/bear market. Figure 2 shows the sharp multiple derating after 2000, which deepened and extended the bear market. The fwd 12mth P/E ratio for the S&P500 is less overstretched than 2000, but an AI bust would like derate the market to 16-18 and also seriously dent tech earnings and revenue expectations.

Figure 2: 12mth Fwd S&P500 and Inverted 10yr U.S. Treasury Yield (%)  Source: Continuum Economics

Source: Continuum Economics

The AI optimists would argue that AI transformational capabilities could increase productivity and the share of profits in GDP substantively, which would transform the U.S. economy and sustain still higher P/E ratios. However, for capital markets this requires U.S. and global corporates to continue to adopt AI enterprise models through 2027 and 2028 at a quick growth pace to sustain the whole vertical AI chain. This is the key question for the next 2 years.