This week's five highlights

Jackson Hole Review

Fed Independence Challenged By Trump

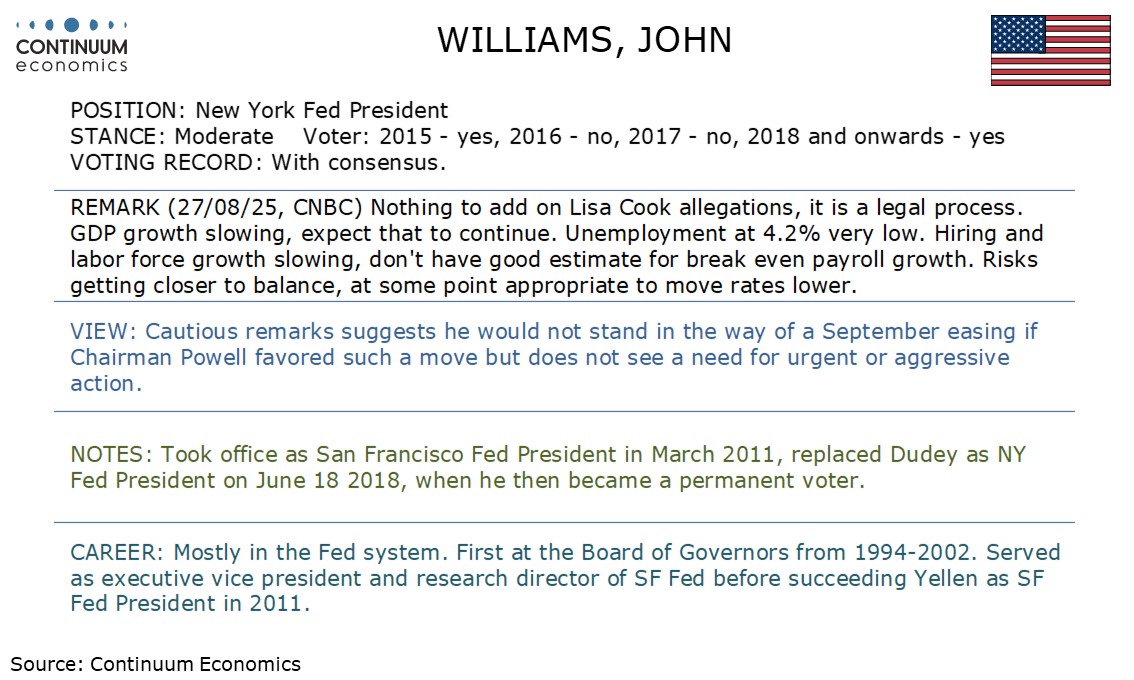

This Week's Fed Speakers

All Lead to USD Chopping Lower

India–US Trade Talks Stalled

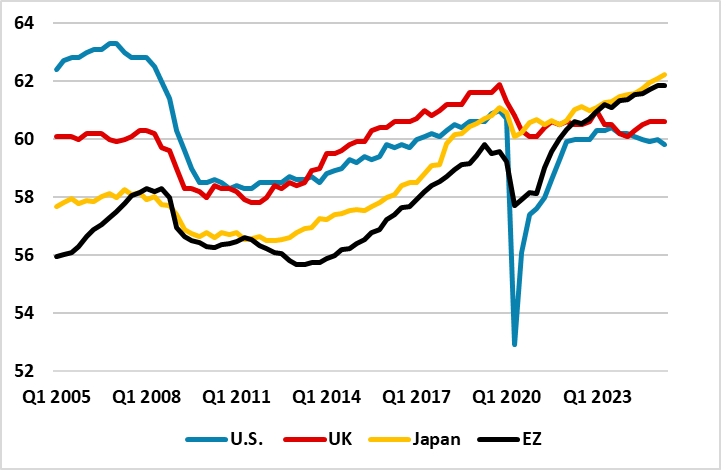

Figure: Employment Rate Major DM Economies (%)

Fed Powell focused on the cyclical softening of employment to back a more dovish undertone. In contrast other central bank heads focused on structural labor market issues. While ECB Lagarde was pleased with the post COVID EZ picture, current economic softness still leaves us forecasting two further 25bps cuts. BOE Bailey worried over a structurally tight labor market, but the contraction in employment is the worst in the G4 and we see this triggering more BOE rate cuts. Finally, BOJ Ueda made suggestion to reduce the tight Japanese labor market, but these are unlikely to be delivered in the next few years and meaning that the BOJ will likely hike in the autumn.

The Jackson Hole conference saw the head of the Fed, ECB, BOJ and BOE talking about labor markets. Fed Powell focus was on the cyclical situation in the context of monetary policy, which we feel signals a 25bps cut at the September FOMC meeting is now likely (here). However, the U.S. also suffers from structural problems in the shape of poor health for the over 60’s; large ex criminal population with lower employment rate and now the crackdown on illegal immigration. We discussed some of these in a recent article (here) and without measures to rectify they mean that the labor market ends up being tighter than normal and causing a medium to long-term dilemma for the Fed. The Trump administration however are not worried about labor supply.

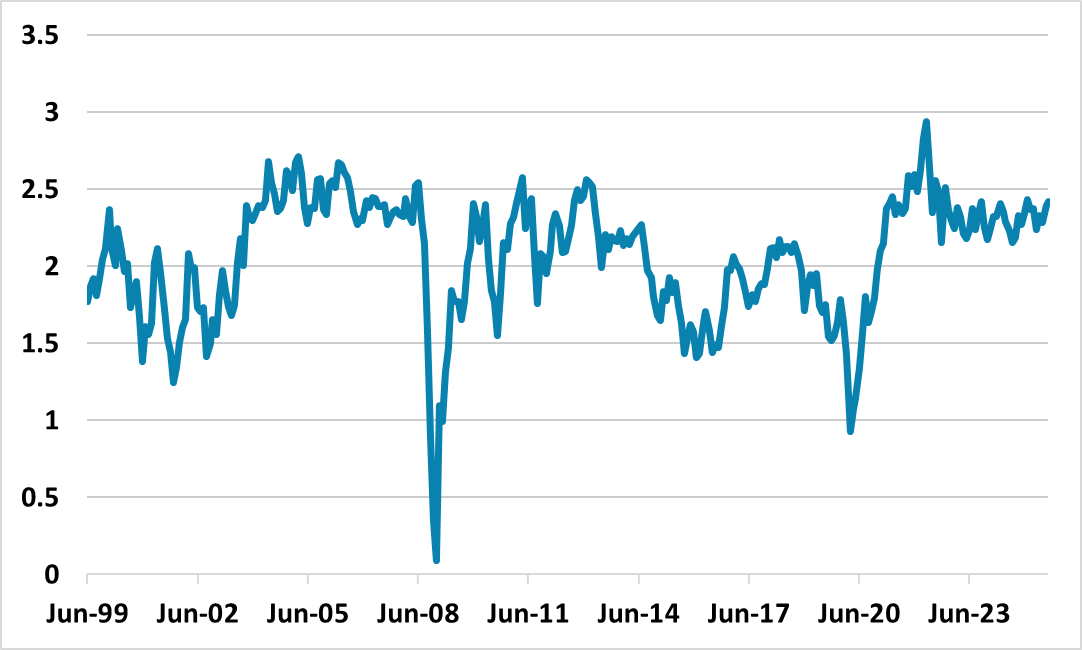

Figure: 10yr Breakeven Inflation (%)

The Fed independence question is getting more news media attention with President Trump announcing he will fire Fed Governor Lisa Cook over alleged mortgage fraud. Cook so far is disputing the legality of the firing and this may not be resolved quickly. It also remains unclear whether Stephan Miran will be in place for the September 16-17 FOMC meeting. Overall, Trump not only wants to blame the Fed, but also try to achieve significantly lower policy rates. So far the U.S. Treasury reaction has been muted to all this drama.

One reason is that the U.S. Treasury market is not clear that new Fed governors will radically shift Fed policy. FOMC votes and shifts in policy tend to be by consensus. If Trump gets a replacement for Cook, alongside with Miran they could vote for radical action at each policy meeting e.g. 100bps of rate cuts. However, the majority of the FOMC would still likely follow the same policy formulation, which from Powell at Jackson Hole appear to be for a 25bps cut at the September FOMC (here) and some FOMC members last week were not even convinced of this stance. The September FOMC voting will be interesting to see whether Bowman and Waller push for a 50bps cut rather than 25bps, especially if the August payrolls are in line with consensus. This would further fuel concerns over Fed independence. A two way split would be unusual, but other central banks have had three way splits (e.g. BOE August decision).

The challenge of Fed's independence has seen DXY chopped lower. With U.S. Treasury yields also treading lower, USD legs are cut. The broader upbeat risk sentiment also reduce the bids for haven USD. Market participants are anticipating a September rate cut. If Trump is successful in installing governors into the Fed, there is expectation those will be dovish and be USD bearish in a mid term.

On the chart, the anticipated break above 98.50 has been pushed back from 98.70~, as overbought intraday studies unwind, with prices currently balanced in consolidation above congestion support at 98.00. Daily readings have turned mixed/negative, suggesting room for a test beneath here. But mixed weekly charts should limit initial scope in renewed consolidation above further congestion around 97.50. Meanwhile, resistance remains at congestion around 98.50 and extends to 99.00. This range should cap any immediate tests higher.

India–US relations have entered a tense phase after Washington doubled tariffs on Indian exports to 50%, the steepest duties applied to any US trading partner. The move, tied to India’s record Russian oil imports, has derailed trade talks scheduled for late August. With USD 87bn in exports at risk and strategic cooperation under strain, both sides face a delicate balancing act between economic pragmatism and geopolitical rivalry.

Relations between New Delhi and Washington have entered one of their most testing phases in recent memory. The sixth round of trade negotiations, scheduled for August 25–28, has been stalled indefinitely, underscoring how the tariff standoff has spilled over into broader economic diplomacy. On August 6, 2025, President Donald Trump announced an additional 25% tariff on Indian exports, doubling the effective duty to 50% on most goods just days after an earlier 25% levy took effect. The move—explicitly linked to India’s continued purchase of Russian crude—makes Indian exports the most heavily penalised by the US, surpassing rates applied to China or the EU, and puts at risk roughly USD 87 billion worth of trade flows.