DM and EM FX Outlook: Cross-Currents for H2 and 2027

· Our baseline for the coming quarters is that global FX is moving through a period of dollar bounce and cross-current positioning adjustment, rather than a clean return to the dollar downtrend. The near-term driver is the market's (over) hawkish reading of the June FOMC/Summary of Economic Projections (SEP), an upside breakout in the dollar and a renewed dalliance with US exceptionalism after a run of stronger US data and resilient risk markets. This can see the dollar flip to the other side of a reinvigorated ‘dollar smile’ short-term, moving from Iran haven support to outperformance support, with these episodes temporarily sidelining long-term valuation considerations.

· In the near term, that can keep the dollar breaking modestly higher even as the Iran haven bid unwinds. EUR/USD can therefore extend the downside break toward 1.12 in coming weeks, as the market catches up to relative US outperformance that had been partly obscured by the Iran shock and the wait for the new Fed chair. By year-end, however, we expect this phase to fade as the US consumer slows, Fed hikes do not arrive, and the market shifts back towards expecting the completion of the easing cycle. That leaves EUR/USD recovering later in the year and stretching into the low-1.20s by end-2027.

· The cleanest tactical unwind remains in the trades that became crowded during the Iran/oil shock. NOK/SEK was arguably the purest expression of that theme and might briefly correct further on the oil moderation and position-squaring continues. AUD also looks vulnerable near term after longs became stretched outright and against NZD, and with a moderate El Nino risk discount adding to what is already a dollar-bounce and positioning correction. JPY should, in theory, benefit from a reversal in the terms-of-trade shock, also easing fiscal support pressures, but market buy-in remains low and hard to time so long as carry, low volatility and momentum still dominate.

· In EM, our favourite EM currency remains the Brazilian Real (BRL). Post-election USDBRL will likely end 2026 at 4.95 if Lula wins, but 4.85 if Flavio Bolsonaro wins, as carry trades become the strong focus once again. End 2027 we now forecast 4.75. Elsewhere, China’s authorities will allow a gradual Yuan rise. We now see further Yuan appreciation to 6.65 by end 2026 and 6.50 by end 2027.

· Risks to our views: A more durable US exceptionalism revival would delay the dollar correction, especially if Fed hike expectations become reality. A severe El Nino impact would turn a modest AUD and NZD setback into a larger food-shock and output-shock trade, with the cleanest expression likely versus the dollar. A renewed Iran shock if Israel undermines the deal meanwhile would return markets to Q2 mode, though in this case markets may be less relaxed this time around. Even so, the most likely catalyst for a deeper U.S. equity correction would be a surprise hard landing for the U.S. economy.

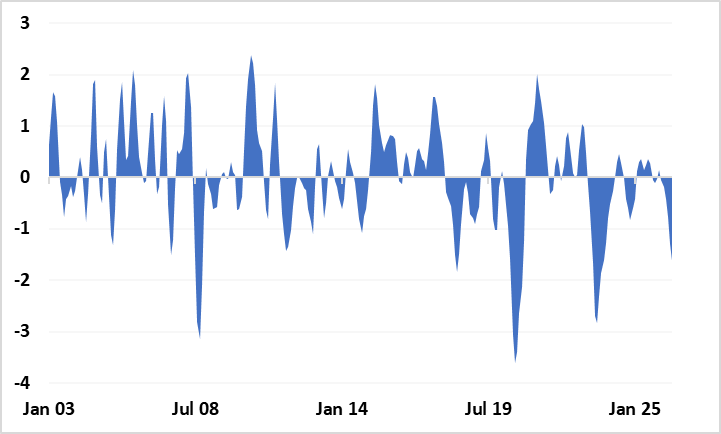

For major FX, the Iran shock interrupted rather than erased the underlying dollar trend. However, the more important question for the next one to two quarters is whether the dollar bounce can extend from haven support into a broader revitalised US exceptionalism trade, even as the Iran premium fades. Recent Fed repricing, wider US yield spreads, firmer US data and renewed AI optimism have allowed the US outperformance narrative to reassert just as the energy shock is starting to look less one-way.

Figure 1: Current dalliance with US exceptionalism: Eurozone economic surprise trend vs US (stdev)

Source: Datastream/Citi, CE

That rotation should still leave room for markets to unwind some of the thematic trades that worked during the oil spike. NOK strength versus SEK, AUD strength and broad commodity-linked outperformance all became crowded for good reasons, but the immediate catalyst is fading. For USD/Europe the effect is more equivocal, because the terms-of-trade hit, relative monetary policy channel and safe-haven channel pull in different directions. That helps explain why USD/Europe volatility has stayed compressed despite very elevated uncertainty.

This story of market bullishness on US resilience, inflation risks and hawkishness on the Fed, then giving way to more measured sentiment into next year, underscores much of the dollar-centric forecast trajectory. On valuation, it is worth noting that much of the dollar's still relatively rich real effective exchange-rate positioning is driven primarily through USD/JPY. It therefore needs a clearer market narrative shift and significant reversal in the latter to see a return to more meaningful mean-reversion dynamics.

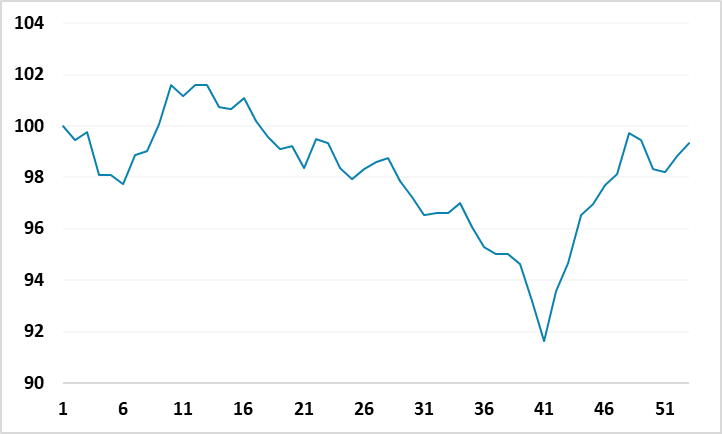

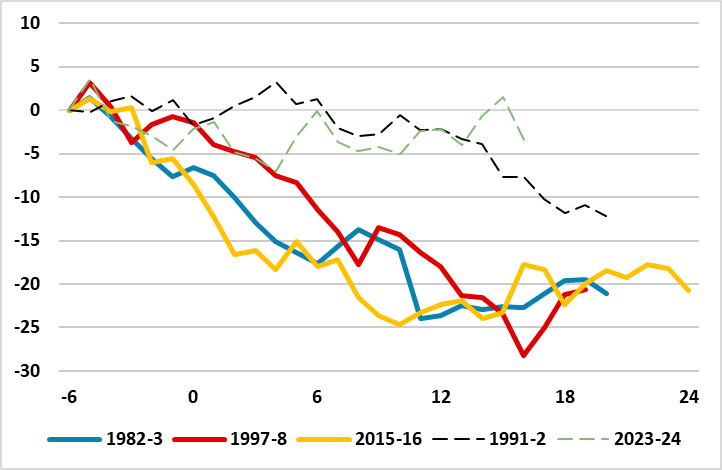

Figure 2: ‘Generic’ risk profile in mid-term years: Nasdaq average weekly trajectory (prior yr-end=100)

Source: Datastream, CE

Mid-term elections are a risk event in H2. Midterm years historically (shown here back to the 80s) can often see equity drawdowns before later recoveries, which could be temporarily risk-off dollar supportive. This particular election also carries some risk of interference or contested results, which could revive the dollar-negative institutional and currency trust issues seen earlier in Trump's second term. Our central view is that markets remain relatively calm, with the main lasting implication being some fiscal restraint from political deadlock after the mid-terms, which would go with the grain of slower US activity into 2027.

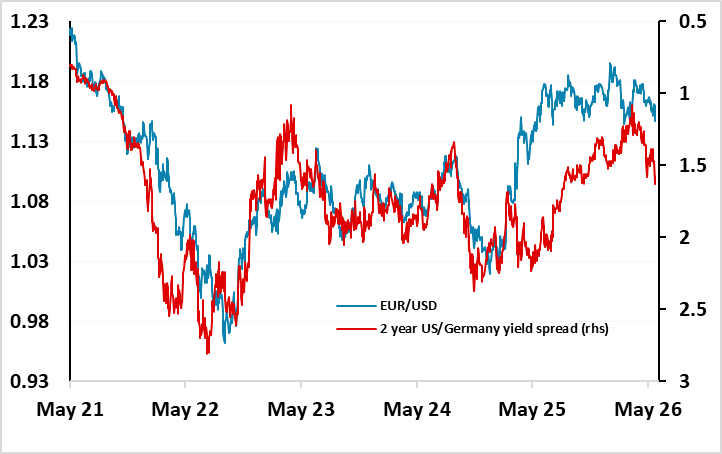

For EUR/USD, we see the market's read on the latest FOMC developments as overdone, with the SEP showing more an uncertain and split board rather than a hawkish one, still consistent with policy being kept on hold if data cools as we expect. Nonetheless, with dollar yield spreads pulled wider and EUR/USD breaking below its recent range, we allow for some follow-through to as low as 1.12 in coming weeks. This can be seen as a period of ‘catch-up’ to a strong spell of relative US outperformance and upside surprise that was sidelined by Iran and the wait for the new Fed chair.

By the end of the year, however, we look for the pair to have recouped ground as a constrained US consumer starts to impinge on the economy, Fed hikes do not arrive, and the market focus swings back to a modest resumption and completion of the easing cycle. We also feel that the AI optimism could become more volatile after the Open AI and Anthropic IPO’s are out of the way (here). While we also see the ECB eventually reversing course, that should help stem rather than prevent the euro rebound. By end-2027, we assume a shift back to global upswing and a resumption of the dollar's slow correction from rich levels allows EUR/USD to stretch out to 1.21.

Figure 3: EUR/USD and the 2year US/Germany yield spread

Source: Datastream, CE

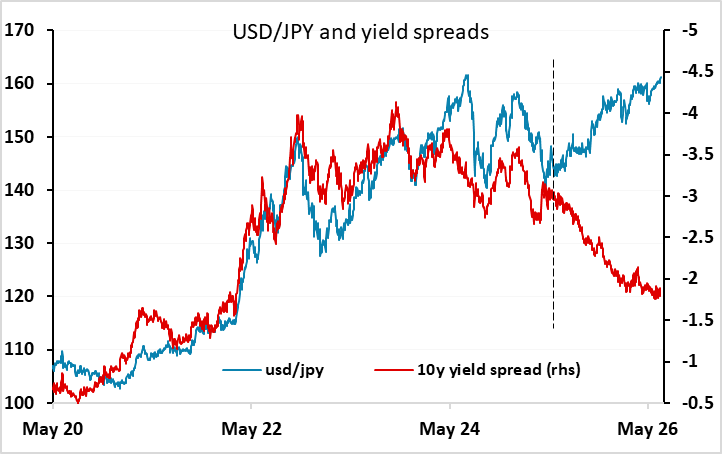

USD/JPY remains the most challenging market. Yen weakness has moved well beyond what yield spreads might imply as the relationship broke down, both because carry has dominated in a low-volatility environment and because the market has built a momentum narrative around Japan's policy bind. The counter-argument is still strong. The energy terms-of-trade shock should partially reverse under the benign Iran scenario, and BoJ tightening, when taking due account of extreme and BoJ-to-Fed-divergent quantitative tightening, is not being fully reflected in relative policy pricing.

If JGBs and yen weakness stabilise, arresting capital-loss concerns, local bonds can become more compelling again for Japanese buyers and for overseas buyers hedged or unhedged. MoF intervention is harder in episodes of broad USD strength, but it can reinforce a cap on the upside and cause periodic shakeouts of spec positioning. We still assume a correction though the horizon, with USD/JPY at 137 by end-2027. A sharper US equity correction, and a wider risk-premium shock, would be the cleanest catalyst for faster yen gains.

Figure 4: USD/JPY and 10-year yield spreads

Source: Datastream, CE

AUD remains favoured over the medium-term horizon, but the near-term balance has shifted. Longs had become overweight, both outright and versus NZD, and it has not taken much in terms of a dollar bounce, mixed domestic data and choppiness in metals and sector risk to pressure liquidation. While Fed repricing versus the RBA remains in place, and while equity markets are still rotating, AUD/USD can complete a corrective phase before stronger fundamentals reassert.

Those medium-term positives remain compelling: fiscal and demographic fundamentals, late-cycle commodity exposure, AI and energy build-out, yield pickup and relative effective exchange-rate cheapness.

The main caveat is El Nino. With a strong event now central rather than a tail risk, we allow for a conservative one-to-two quarter AUD setback within a broader period of dollar strength and position correction. The forecasted decline is modest relative to the potential output and agricultural impact, but the FX history is noisy and the shock overlaps with other macro forces. If the event remains strong rather than severe, this should be more of a temporary headwind than a reason to abandon the longer-term AUD recovery preemptively. This issue does represent a clear downside risk to the market however and is likewise a wildcard for more lasting dollar strength.

Figure 5: AUD/USD around super (bold) or strong (dashed) El Nino episodes, % from -6mth base

Source: NOAA, Datastream, CE

The historical FX pattern is not clean, because El Nino episodes often overlap with other large shocks (if sometimes not entirely coincidentally). But the direction of travel is still useful: severe episodes tend to be difficult for the antipodeans, especially against the dollar, while CAD is more nuanced (net positive locally but globally influenced) and JPY can benefit if the weather shock becomes a broader risk-off or carry-unwind event. This argues for treating El Nino as a baseline headwind to the AUD forecast, with a larger downside scenario if the weather impact becomes severe.

Macro estimates also point the same way, although they should be treated as scenario inputs rather than precise forecasts. A strong El Nino can subtract around half a percentage point from Australia GDP and slightly less from New Zealand, while the US and Canada can see a modest positive growth impulse. In severe or super episodes, the output hit can be twofold or more, and the currency reaction can scale more sharply still if the market narrative moves from the Iran shock to a food shock. That would favour short antipodeans versus the dollar on a one-to-two quarter horizon, with positioning and USMCA risk complicating CAD.

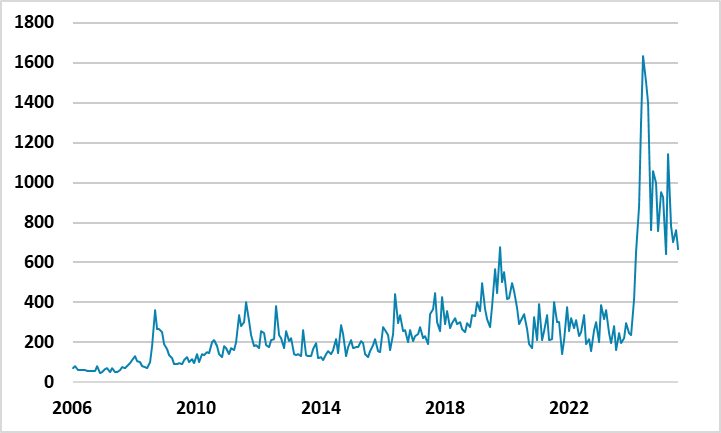

Figure 6: Canada could retain a near -term risk discount: Canada policy-uncertainty index

Source: Baker, Bloom, Davis, PolicyUncertainty.com

For Canada, the global dollar and risk channel can still dominate the currency even if Canada is a net macro beneficiary from El Nino. The more immediate local risk is USMCA. As things stand, and given Trump's approach to deal-making, it seems unlikely that renewal is signed by the US on 1 July, with USTR Greer signalling strongly that the U.S. wants an addendum separately with Canada and Mexico to the existing deal. That could also push the agreement into an annual or multi-year review process with scope for standoffs and headline risk. Even so, threats against Canada will escalate from the Trump administration in the next 6 months. CAD has partly discounted this risk, and an early resolution would be bullish, but the more likely path is a period of elevated risk. It should also be noted Alberta separatism is another risk factor into the autumn, although polling on the non-binding vote currently has ‘remain’ comfortably in the lead leaving it as a background topic to monitor rather than a central forecast driver.

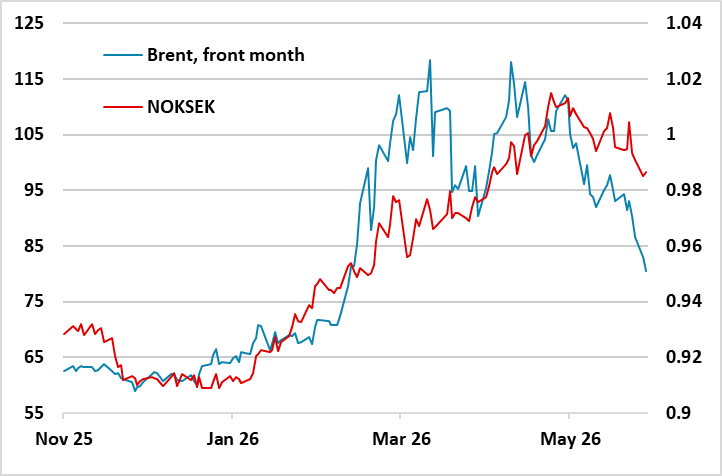

Figure 7: Recent NOK/SEK performance and oil prices

Source: Datastream, CE

Among the majors, NOK/SEK has been the cleanest Iran thematic trade to fade. It also went with the grain of divergent monetary policy, interest-rate spreads and relative NOK cheapness. In the immediate term it can have further room to pare as long as oil breaks lower and positions are squared – that is, if the Lebanon flashpoint does not derail progress. We also see Norges Bank policy as the most restrictive and overly-hawkish among the majors meaning that a lot is in the current price. Further dollar upside however would still tend to dominate both currencies, and could stymie SEK recovery especially if risk market prove noisier near-term. Over the medium term, we continue to see value in the Scandinavian currencies given robust fundamentals especially as fiscal strength becomes a more important base load factor over time. Both, especially Sweden, have some minor positive exposure to AI through tech startups, green energy and data centre build-out, though this should remain a footnote consideration rather than a driver.

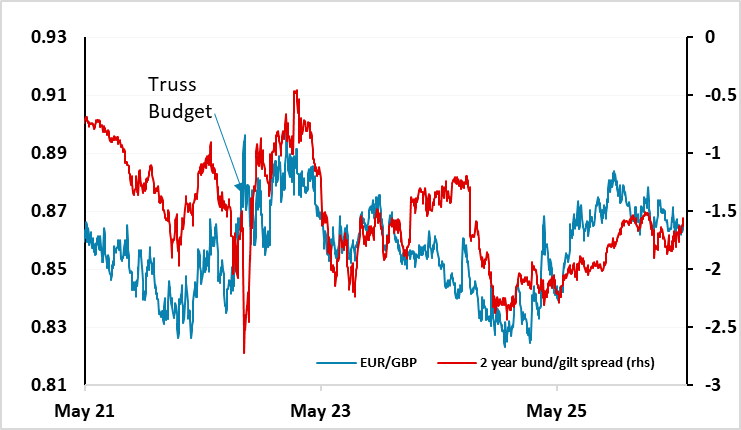

On sterling, we remain reasonably neutral and expect the medium-term broader EUR/GBP range to hold, which at current prices allows some upside drift for the cross. Politics remains live, and the market may at times be uneasy (issues such as re-nationalisation may perhaps create disquiet even if fiscal action is measured). Looking glass half full, an Andy Burnham victory that reinvigorates Labour and slows the populist parties such as Reform could be seen as a good outcome, given that Burnham would probably stretch rather than abandon the fiscal framework, while success from institutionally immature populist parties could bring more Truss-like chaos.

Episodes of UK fiscal stress are more likely to be seen in reaction to spikes in global sovereign yields, via debt-interest pressure on the budget, than through a dramatic domestic fiscal event. We remain more dovish than the market on the BoE, although the market has moved closer to our on-hold view for this year. While we are also more dovish than the market on the ECB, some short-end spread narrowing through mid-2027 should allow EUR/GBP a modest upside drift while broadly maintaining range action. Eurozone fiscal concerns, especially France, can still at times outweigh UK-specific risks and allow sterling to outperform intermittently. Renewed appetite and rotation support for financials can also play to periods of outperformance.

Figure 7: EUR/GBP and 2-year yield spread

Source: Datastream, CE

EM FX

China authorities are allowing a slow controlled appreciation of the Yuan. The Iran war has so far not hurt China economy, with coal/renewables playing a bigger part in electricity production. Additionally, monthly trade numbers also show that exports are still performing well, both due to Chinese companies’ keenness to export but also as the real value of the Yuan has fallen since 2021 with overseas inflation outstripping inflation in China. The current account surplus will likely be around 3.5% of GDP in 2026 and this will keep the Yuan firm. The May 2025 Xi-Trump summit has also reinforced the sense that tariffs threats are now under control and China/U.S. trade truce can hold. We feel that the authorities will pause appreciation at times via FX intervention, but then allow appreciation to restart. The reopening of the Straits of Hormuz would make the authorities more willing to accept appreciation. This willingness to allow slow appreciation also appears to be linked by official desire to increase long-term usage of the Yuan. President Xi Jinping's 2024 speech also noted that the yuan should be widely used in global trade, investment, FX markets, and more importantly, have the status of a global reserve currency. We now see further Yuan appreciation to 6.65 by end 2026, though the authorities will be reluctant to see much more. Additionally, the 2yr spread between the U.S. and China also argues for slow further appreciation.

Figure 8: USD/CNY Exchange Rate

Source: Datastream/Continuum Economics

For end 2027 we forecast USDCNY at 6.50. China authorities did allow Yuan appreciation in 2014, 18 and 22 (Figure 8), but became sensitive below 6.25. Stepwise this probably translate into a restraint around 6.50 in 2027. Additionally, China prospective returns for bonds and equities are unattractive for active global investors, even if global benchmarks require passive funds to increase weighting in China. FDI data also shows that inflows have slowed, as the private sector business environment is less positive than the go-go years from 1990-2019. FDI inflows will likely be narrowly focused on AI and Green energy. However, the current account surplus will remain large and this will keep the Yuan firm. We see 6.50 by end 2027.

Our favourite EM currency remains the Brazilian Real (BRL). We have been constructive on the BRL, but we feel that the BCB will now be slower in easing in 2026 and 2027 with the oil price shock from the Iran war (here). This makes us more bullish on the BRL over this 18-month period. However, pre-election fiscal easing remains a risk with close opinion polls for the presidential election and Q2 and Q3 will likely see a BRL consolidation/mild correction as the political race intensifies. Domestic players are also biased against too much BRL strength due to fiscal fears, which has restrained the BRL unless the USD is in a downtrend. Post-election USDBRL will likely end 2026 at 4.95 if Lula wins, but 4.85 if Flavio Bolsonaro wins, as carry trades become the strong focus once again and the gradual USD downtrend continues. We also see a slower pace of BCB easing before the election with one 25bps cut in September and then two 25bps cut in Q4 to 13.50% end 2026.

2027 will likely see more BCB cuts to 11.50%, but then lower short and long-term yields help reduce government debt servicing and we would also see some fiscal consolidation. Though we see a prolonged reopening of the Straits of Hormuz, the Iran war has reinforced the desire to buy more Brazilian commodities multi-year. This can all keep the BRL underpinned and we now forecast 4.75 for end 2027. BCB has already tried some FX intervention, but this is unlikely to be effective unless accompanied by aggressive rate cuts (unlikely given BCB policy rate caution).