Brazil: Slowing Pace of Cuts and BRL Strength

· Brazil cut the SELIC by 25bps to 14.25%, but received critiques from the market by raising end 2027 CPI inflation from 3.5% to 3.7% and talking about Q1 2028 in the relevant policy horizon. We feel that BCB still wants to leave the door open to further cuts in 2026, given how restrictive policy is. We see a slower pace before the election with one 25bps cut in September and then two 25bps cut in Q4 to 13.50% end 2026. The BRL can thus be well underpinned by high rates and we forecast USDBRL at 4.90% by end 2026.

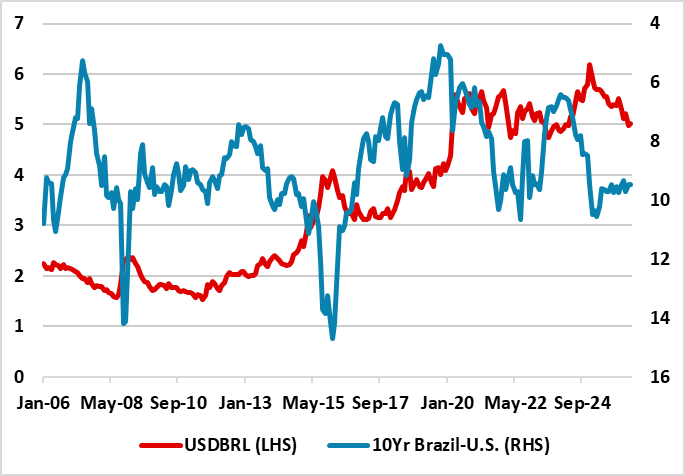

Figure 1: USDBRL and Inverted 10yr Brazil-U.S. Government Bond Spread (%)

Source: Datastream and Continuum Economics

Sentiment towards the BRL remains constructive. Brazil is a commodity safe haven for oil importers with disrupted supplies from the Middle East and grain buyers fearful of higher prices (Gulf fertilizer export freeze and a strong El Nino). Still high policy rates and bond yields provide ample real returns with inflation broadly controlled. The goldilocks macro story is finished with reasonable growth, which provides some scope to weather external storms. Although, these drivers are quite well appreciated, the real effective exchange rate has only just got to the 10yr average and most estimates of fair value on USDBRL are around 4.50. It is also worth remembering that the BRL can have large countertrend against the USD, which in 2006-08 was 30% (Figure 1) during the last major USD downtrend. Current 10yr Brazil-U.S. bond yield spreads are currently higher than this period.

We have been constructive on the BRL, but we feel that the BCB will now be slower in easing in 2026 and 2027 with the oil price shock from the Iran war. This makes us more bullish on the BRL over this 18 month period. However, pre-election fiscal easing remains a risk with close opinion polls for the presidential election and Q2 and Q3 will likely see a BRL consolidation/mild correction as the political race intensifies. Domestic players are also biased against too much BRL strength due to fiscal fears, which has restrained the BRL unless the USD is in a downtrend. Post-election USDBRL will likely end 2026 at 4.95 if Lula wins, but 4.85 if Flavio Bolsonaro wins, as carry trades become the strong focus once again and the gradual USD downtrend continues. We also see a slower pace of BCB easing before the election with one 25bps cut in September and then two 25bps cut in Q4 to 13.50% end 2026.

2027 will likely see more BCB cuts to 11.50%, but then lower short and long-term yields help reduce government debt servicing and we would also see some fiscal consolidation. Though we see a prolonged reopening of the Straits of Hormuz, the Iran war has reinforced the desire to buy more Brazilian commodities multi-year. This can all keep the BRL underpinned and we now forecast 4.75 for end 2027. BCB has already tried some FX intervention, but this is unlikely to be effective unless accompanied by aggressive rate cuts (unlikely given BCB policy rate caution).