Tone of FOMC Minutes From March 20 is Not Hawkish

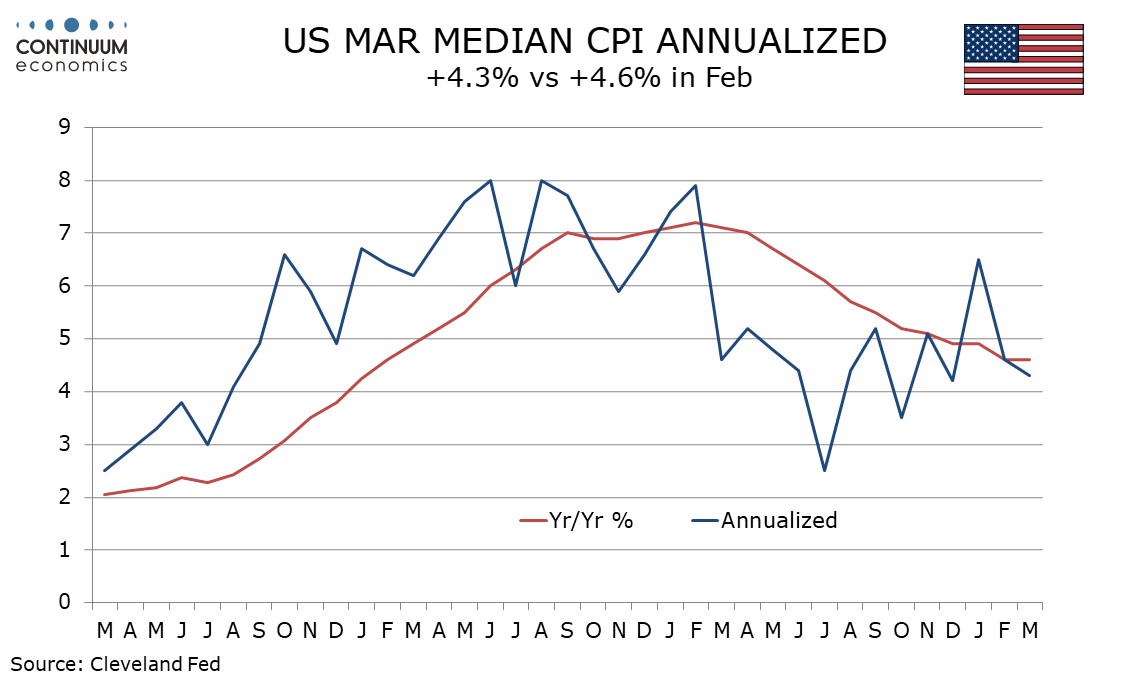

FOMC minutes from March show little sign of disagreement and the tone is not hawkish, with participants expecting both inflation and the economy to slow, and there being a clear majority view that the pace of balance sheet reduction should soon be trimmed. Optimism on inflation is however cautious which the strong CPI outcome for March is likely to have dented.

Participants noted that they continued to expect that inflation would return to 2% over the medium term. They observed that significant progress had been made over the past year even though January and February data had been firmer than expected. Some noted that those gains had been relatively broad based and should not be seen as aberrations. However a few noted that residual seasonality could have impacted the readings. Some unevenness was anticipated as inflation returned to target though it was noted that recent data had not increased their confidence of a return to target, and March data will have caused further doubts. Participants also expected economic growth to slow from 2023’s strong pace and assessed that labor demand and supply were coming into better balance.

All agreed it was appropriate to leave policy unchanged at the meeting and almost all agreed it would be appropriate to ease at some point this year if the economy evolved as expected, though they wanted greater confidence on inflation returning to target before easing. They noted the risks of easing too late and too soon, with incoming data seen as important for assessing the latter risk. On policy the message is of a consensus looking towards easing despite recent disappointing data but the consensus having some vulnerability to further strong data, which has materialized in March’s CPI release.

Before discussing the economy and when to ease, the minutes address the pace of balance sheet reduction, which suggests that the conclusions here are unlikely to be vulnerable to the CPI disappointment. After reviewing lessons from 2017-2019, participants broadly assessed a cautious approach to further runoff was appropriate with the vast majority favoring slowing the pace of runoff fairly soon. This did not mean that the balance sheet would ultimately shrink by less than it would otherwise. Participants generally favored reducing the monthly pace of runoff by roughly half from that seen currently. Participants generally preferred to maintain the existing cap on agency MBS and adjust that on USTs.