FX Daily Strategy: N America, May 24th

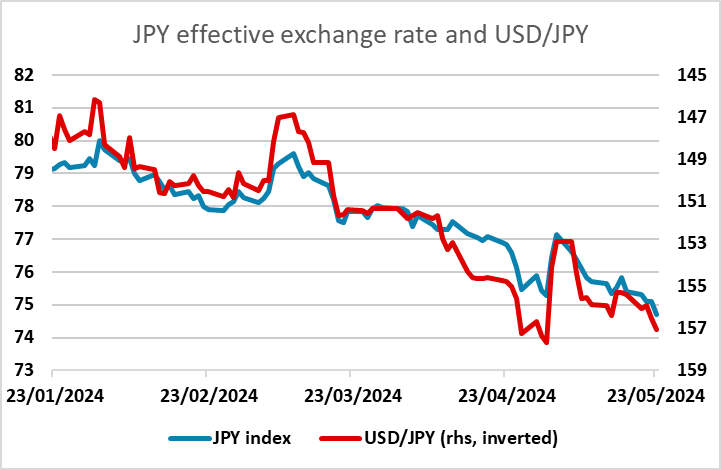

JPY to focus more on intervention threat than Japanese CPI

Levels suggests intervention likely but timing uncertain

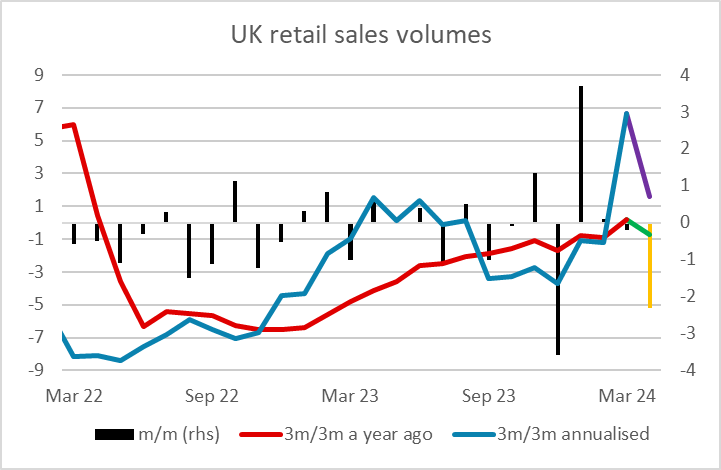

GBP to maintain firm tone despite softer PMIs

CHF looks a more attractive funding currency than the JPY

JPY to focus more on intervention threat than Japanese CPI

Levels suggests intervention likely but timing uncertain

GBP to maintain firm tone despite softer PMIs

CHF looks a more attractive funding currency than the JPY

The April Japan y/y CPI continued to moderate with headline falling to 2.5% from 2.7%, ex fresh food to 2.2% from 2.6% and ex fresh food & energy to 2,4% from 2.9%. While it remains above 2%, the further moderation nevertheless puts cap on BoJ's tightening magnitude. 10yr JGB yields gained a foothold above one percent.

More important for the JPY was Thursday’s stronger than expected PMI data, notably in the US where the services index hit its highest for a year. This triggered a rise in US yields and pushed USD/JPY above 157. There was a sharp drop of 50 pips after the move above 157, but the drop doesn’t seem to have been large enough or sustained enough to be the result of intervention, even though we are at levels where intervention looks increasingly likely. The Asian session will be focused on whether the Japanese authorities decide to intervene at these levels, with the trade-weighted JPY already below the levels seen at the last intervention. Action looks inevitable sooner or later, but the BoJ may prefer to maintain an element of surprise rather than get tied down to defending a particular level. While US yields rose in response to the data, it is notable that yield spreads don’t provide a strong case for USD gains as Japanese yields have been rising in the last week.

GBP was one of the less strong performers on Thursday as UK PMIs were less impressive than the Eurozone and the US numbers. UK April retail sales came in much weaker than expected, falling 2.3% m/m, but after a quick spike higher EUR/GBP has returned to opening levels just below 0.8520. The decline in retail sales was unexpectedly large, but retail sales have been choppy in recent months, and are often seasonally affected in the spring, so it would be wrong to read too much into today’s data. The underlying trends remain fairly steady, and we are likely to have a significant correction next month. If that is also weak, there will be more reason for concern, but for now the market will continue to see little to no chance of a rate cut in June and EUR/GBP is likely to hold close to 0.8520, with the bias still towards testing the 0.8492-0.8500 support area.

Neither US durable goods orders not Canadian retail sales numbers looks likely to have any significant market impact. For the USD, the risk of BoJ intervention may mean USD bulls look elsewhere. In a risk positive environment USD/CHF looks to be the obvious alternative given low Swiss rates, the SNB’s comfort with a weaker CHF and the strength of the CHF in recent years (particularly against the JPY). There may be scope to test the recent highs above 0.92 in USD/CHF.