FX Weekly Strategy: Asia, May 13th-17th

Scope for EUR/USD to break higher

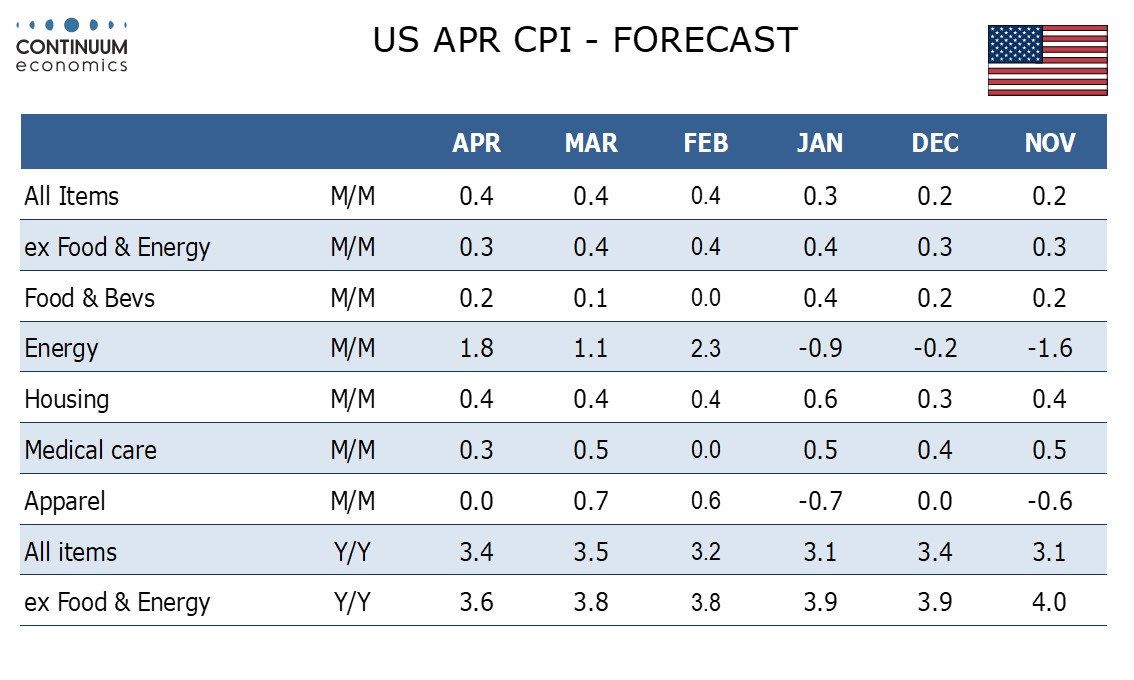

Focus on US CPI data

GBP/USD may return to previous correlation

JPY still has most potential for recovery

Strategy for the week ahead

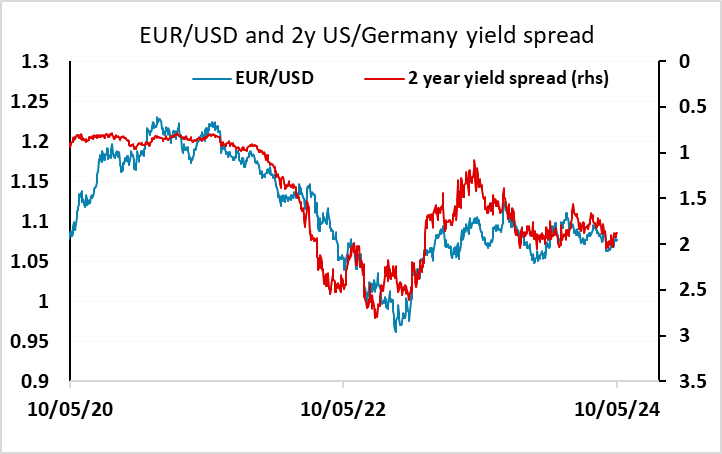

EUR/USD has been quite steady in the 1.07-1.08 range for much of the last week, having moved up from below following the US employment report. It continues to broadly follow short term yield spreads, but we do sense that an upside break may be about to occur. There are essentially three reasons for this. First, the US data has softened up a little, with weaker PMI, ISM and confidence and higher claims data in the latest week. Second, European data has started to show some improvement, notably the UK GDP data for Q1 rising 0.6% with the Eurozone GDP Q1 data also showing a stronger than expected 0.3% rise. The European economies appear to have emerged from the shallow recession of H2 2023. Third, USD valuation remains at very high levels, and looks out of line with a variety of metrics. While this has been justified by the outperformance if the US economy in recent years, the case for USD strength will fade if economic performance starts to equalize.

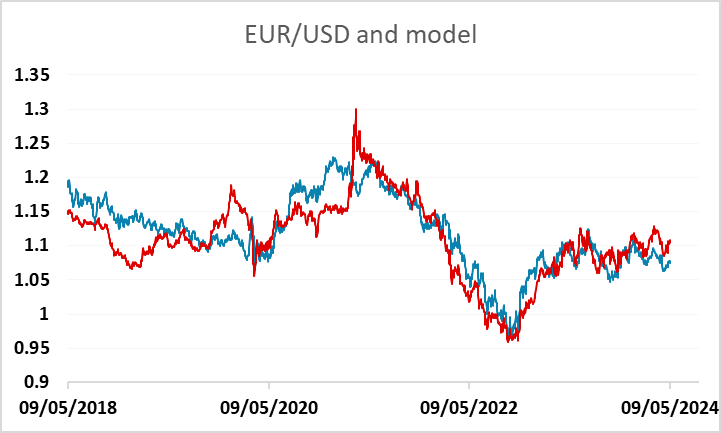

But it’s early days, and EUR/USD has in the short run stuck fairly close to correlation with the 2 year US/Germany yield spread. This week the market will be focused on US CPI and retail sales data to see if this changes the chances of US rate cuts in the coming moths. Our forecast for core CPI is in line with consensus at 0.3%, but a bit above consensus for the headline at 0.4%. This would be unlikely to encourage any expectations of Fed easing and may provide the USD with some support. But European currencies also show some correlation with equities and with the relative performance of US and European equities. Our model based on these relationships suggests there is some upside scope for EUR/USD here, which will be greater if we see any European equity outperformance due to improving growth numbers.

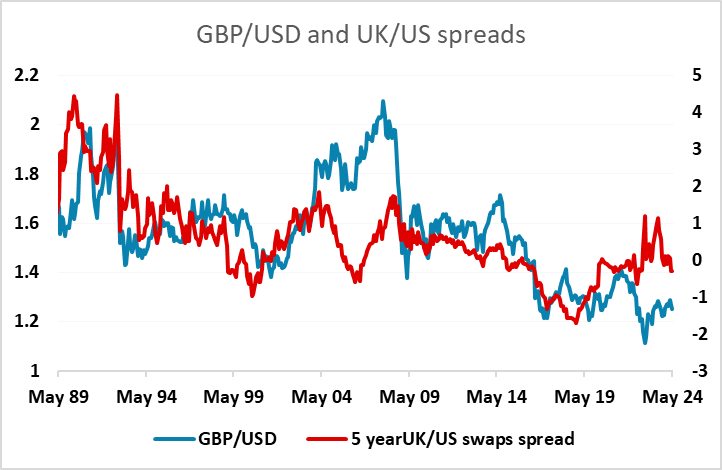

The UK Q1 GDP rise of 0.6% was significantly better than expected, but we are a little wary of the data as the strength was largely due to weak imports, and came after a 0.3% decline in Q4. Even so, the underperformance of GBP/USD relative to yield spreads has been quite striking in the last couple of years, and this may be partially related to the relative weakness of UK growth. There may also be some political risk premium, as GBP weakness was most pronounced in the short-lived UK Truss administration. The political risk story may change as we come up to US and UK elections at the end of the year (the UK election may be anytime between now and January, but most likely in the autumn). There is uncertainty in the US, while in the UK a Labour government is a near certainty, and at this stage is a favoured outcome for the markets. Of course, in the short term the market is likely to be more concerned with interest rate expectations, and these could be affected by this week’s labour market data. The BoE tone at last week’s MPC meeting was more dovish, and we may see GBP weaken if wage data provides support for a dovish view. But GBP/USD may start to look attractive on dips from a longer term perspective.

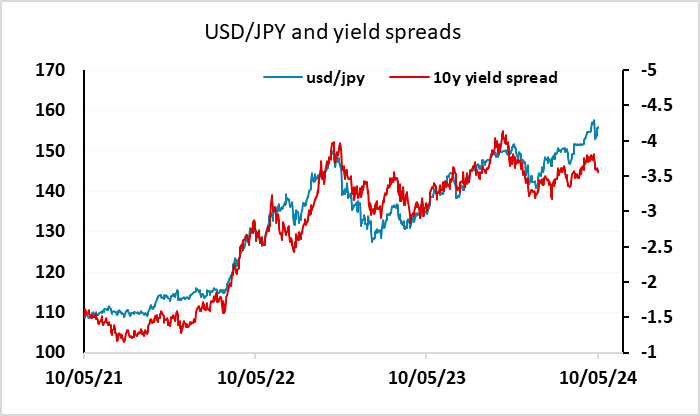

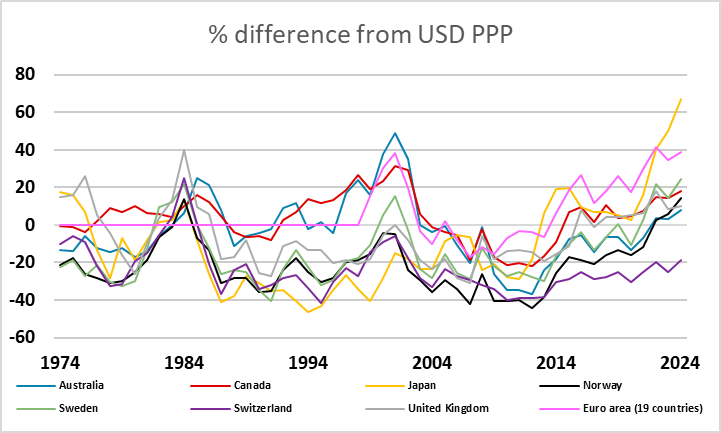

The USD is clearly highly valued across the board, not just against European currencies. The JPY is, of course, the most notably weak currency, and we continue to see risks of a sharp JPY recovery, which will grow if the market starts to sense a slowdown in the US and a general weakening of USD sentiment. Yield spreads suggest downside risks for USD/JPY in any case, but low US equity risk premia tend to correlate with a weak JPY on the crosses, and at current levels suggest EUR/JPY could hold in the high 160s. We still expect the JPY to show a general recovery, but gains against the USD are likely to be easier than gains on the crosses as long as equities look resilient.

Data and events fro the week ahead

USA

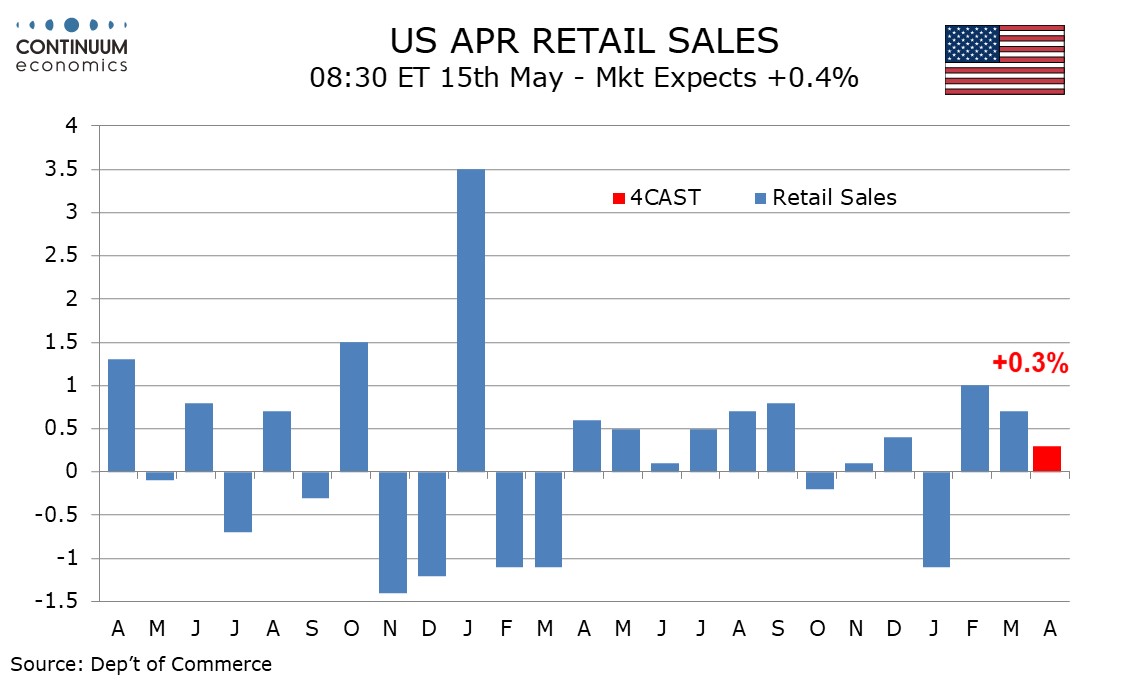

The key day of a busy week in the US will be Wednesday, when April CPI and retail sales data will be released together. For CPI we expect a third straight increase of 0.4% overall, but with the ex food and energy pace slowing to 0.3% after three straight gains of 0.4%. While a slowing will be welcome, 0.3% is still higher than the Fed would like. While CPI is the most important release, retail sales will give important insight on the strength of the consumer. We expect a modest rise of 0.3% overall, 0.2% ex autos, with sales unchanged ex auto and gasoline, pausing after strong March gains of 0.7%, 1.1% and 1.0% respectively. With CPI and retail sales May’s Empire date manufacturing survey will also be released. March business inventories, where existing data suggests a 0.1% decline, and April’s NAHB homebuilders’ index, follow. Fed’s Kashkari is due to speak on Wednesday.

Monday sees no significant data but Fed’s Mester and Jefferson will speak. On Tuesday we expect April PPI to rise by 0.3%, with a modest 0.2% gain ex food and energy. Fed’s Powell’s due to speak with ECB’s Knot on Tuesday. Thursday’s initial claims will be interesting after a preceding sharp spike. At the same time we expect April housing starts to rise by 4.5% to 1380k after a 14.7% March decline while permits fall by 1.2% to 1350k after a 3.7% March decline. April import prices and May’s Philly Fed manufacturing survey are also due. Soon after we expect a 0.3% rise in April industrial production with manufacturing output rising by 0.2%. Fed’s Harker, Mester and Bostic are due to speak on Thursday. Friday has a limited calendar, with April’s leading indicator the only data release.

Canada

In Canada March building permits are due on Monday, and March wholesales sales on Thursday, for which the preliminary estimate was a 1.3% decline. Wednesday sees April housing starts and April existing home sales, as well as March manufacturing shipments for which the preliminary estimate was a 2.8% decline.

UK

Major data awaits with the first of what the BoE view as critical in determining when rates may be cut. Indeed, Tuesday sees the labour market update still presented amid continuing concerns over the accuracy of figures and this time around will offer Q1 productivity insights. The numbers may show a further rise in the jobless rate and higher inactivity, but there will be as much weight on HMRC numbers regarding job dynamics which have suggested clearer slowing in private sector employment, if not an actual contraction. However, the average earnings figures will be the most closely watched and where we see only a modest slowing in both regular pay growth (3 mth mov avg) at just below 6% and the headline rate down to below 5.5%.

Regardless, with even the BoE (belatedly) casting doubt on the validity of these numbers, more attention may be paid to the PAYE pay data where a clear(er) slowing has already been seen. Tuesday also sees comments from BoE Chief Economist Pill and rate cut advocate Dhingra but later in the week two of the MPC hawks offer opinion, most notably Megan Greene (Thu).

Eurozone

Datawise, the main event will be updated Q1 GDP numbers where no material revisions are seen. But an underlying continued still weak undertone will be evident in what may be a clear fall in March EZ industrial production data released alongside on Wednesday. Media-wise there will be interest in the ECB Financial Stability Review (Thu) which will provide an overview of potential risks to financial stability, this time possibly looking at private sector credit. Final HICP data (Fri) may see no revision. (Probably), there are also the European Commission economic forecast updates where GDP projections may be curbed with the question being whether the just-above target rate for HICP inflation for next year is belatedly trimmed.

Rest of Western Europe

There are key events in Sweden, with the minutes to last Riksbank meeting due (Wed), albeit with little likely to be gleaned regarding the rate cut and/or the possible policy oath ahead. Norway sees monthly and quarterly GDP (Thu) and where a 0.1% q/q rise is anticipated, but with some loss of momentum at end Q1. Switzerland sees consumer confidence data (Mon) and industrial production (Fri), both likely to be soft.

Japan

We will have the preliminary Japan GDP for the first quarter of 2024 on Thursday, May 16. It is very likely we will have another weak number as household consumption albeit rebounded to positive territory for the past two months, is still depressed by negative real wage and high inflation. Whether it will dip into negative territories and the actual private consumption number will be critical to watch and very affect JPY sentiment. Else, we have PPI on Tuesday and Industrial Production on Thursday.

Australia

The labor and Wage price index will be the highlight of Australia next week on Wednesday , May 15 and Thursday, May 16. The last jobs report disappointed and continue to point towards a choppy downtrend for the Australian labor market which we forecast to persist. The impact towards the market will unlikely to last for the limbo between RBA and CPI remains key. Thus, wage price index will capture more eyeballs.

NZ

We have RBNZ Inflation Expectations on Monday, May 13 and PPI on Friday, May 17.