FX Weekly Strategy: April 29th - May 3rd

Focus on FOMC and US employment report

Scope for USD strength on strong US labour market data

JPY weakness is extreme but hard to buck the current correlations

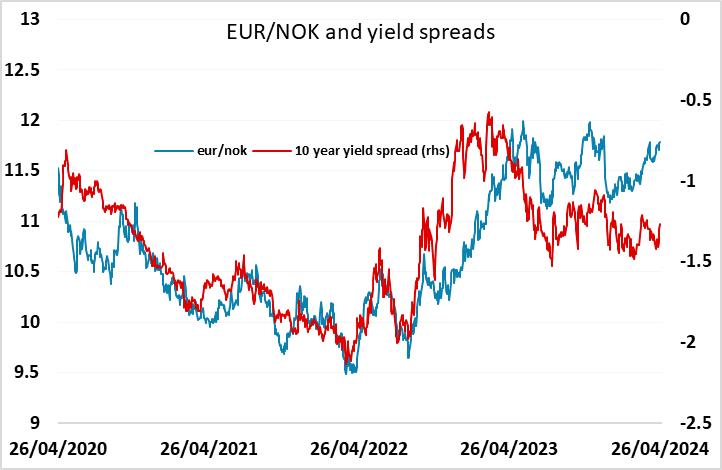

NOK also looks too weak

Strategy for the week ahead

The focus will of course be on the US FOMC meeting on Wednesday and the employment report on Friday. While there has been interest in the BoJ meeting and the PMIs in the last week, FX markets are currently being driven mainly by US yields and US equities, and the combination of the Fed and the employment report will be the most important drivers of these and consequently of FX.

However, it’s hard to see the FOMC changing the market’s view of Fed policy very much. The recent firmer inflation numbers have clearly made even the doves less keen to ease, so the current market pricing of just 37bps of easing this year with the first cut not fully priced until November is unlikely to change a great deal. However, it will be difficult to price in less easing than this, and if the statement indicates that he Fed still anticipates easing his year there may be some modest downside risks for US yields and the USD.

There may be more potential for the market to move on the employment report, and we see the risks to be to the strong side of market expectations, with upside risks to both average earnings and non-farm payrolls. Any USD losses on the Fed are therefore unlikely to last long.

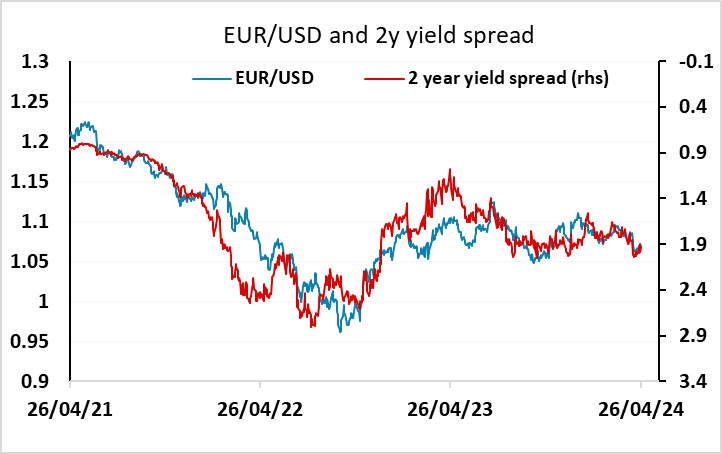

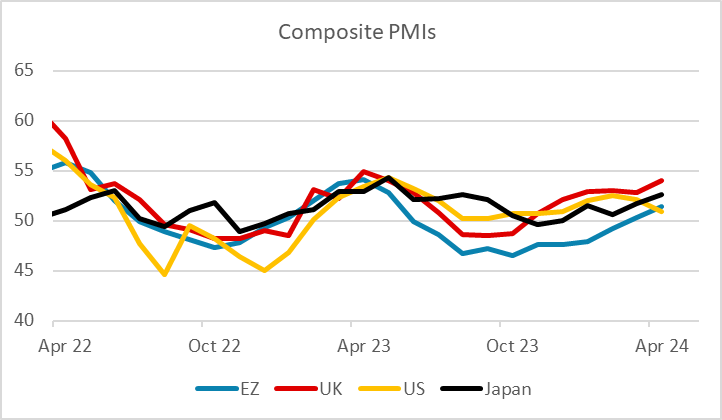

While the US will be the main focus there will also be interest in the GDP and HICP data from the Eurozone. The PMI data last week has created some positive sentiment for the EUR, particularly given the weaker PMIs in the US, but we see downside risks to the market expectation of a 0.2% Q1 GDP gain. This should maintain market expectations of ECB easing and help prevent any extension of EUR/USD gains above 1.07. However, there is more potential for market impact from the CPI data. Our forecast is in line with then market at 2.4% for the headline, suggesting net downside risks for the EUR. But in practice yield spreads against the US have not been moving much and movements are generally dominated by US developments, so we doubt there will be much deviation away from 1.07.

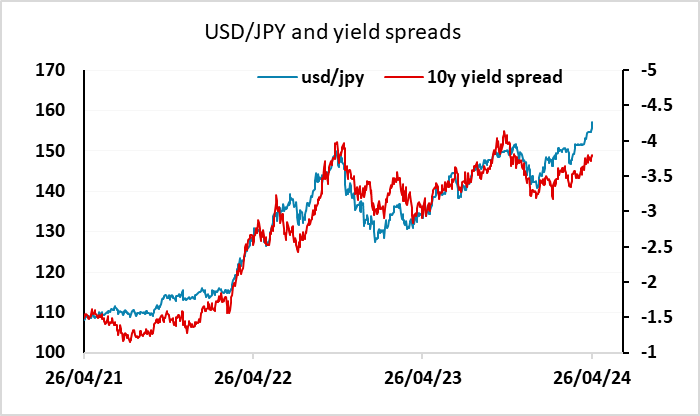

USD/JPY has shown a lot more volatility than EUR/USD in the last week (and this year), with the JPY the weakest of the major currencies, and there will continue to be a lot of focus on USD/JPY after the new 34 year high near 157 seen on Friday following the BoJ meeting. Despite a brief spike lower on Friday, there has been no confirmed BoJ action, but the danger of intervention remains. JPY weakness continues to be driven by wide yield spreads and the JPY’s negative correlation with equity risk premia, and this correlation doesn’t suggest we are about to see a significant turn in JPY weakness. So from this perspective Japanese intervention would only likely have a temporary (although possibly quite sharp) impact.

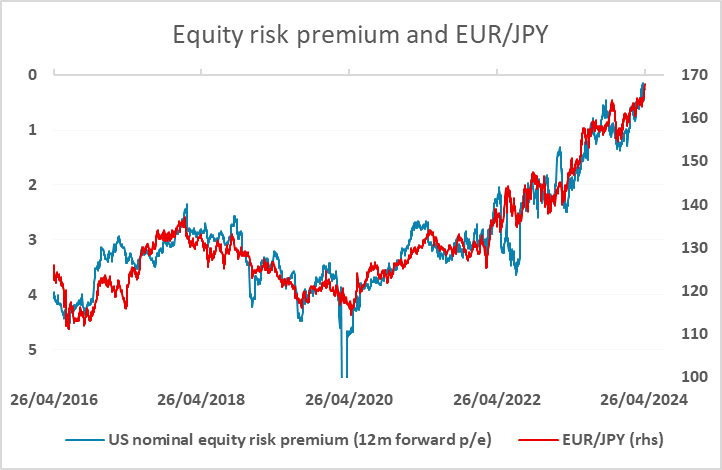

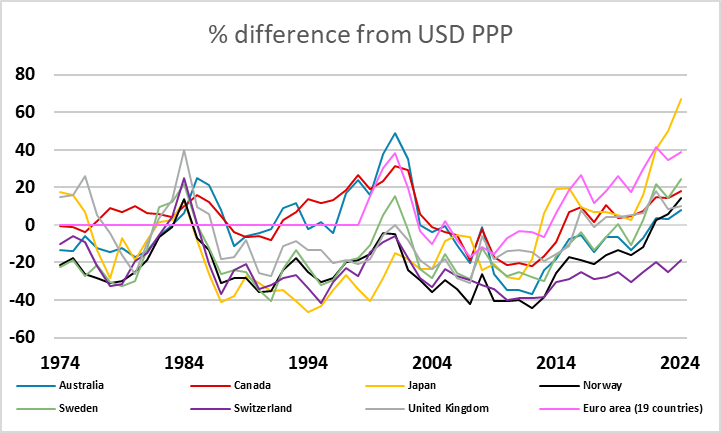

However, there is another perspective. While the correlation with risk premia is well established, it has little fundamental basis, and in particular ignores the relatively low Japanese inflation in recent years which has meant that the JPY’s decline has been much larger in real terms than it looks to have been in nominal terms. This makes it difficult to believe that the correlation with risk premia can persist in the long run, as it is real rather than nominal exchange rates that are economically significant. While the headlines refer to USD/JPY hitting 34 year highs, this is a largely meaningless nominal value, and in real terms the JPY is at all time floating era lows. Most do not appreciate the extent of the JPY’s weakness. Not only is it at all time lows in real terms, it is further below PPP than any major currency has been in the floating era. This makes the chances of a huge reversal of JPY weakness that much greater, and while the short term correlations with nominal yield spreads and risk premia are hard to oppose, it should be recognized that these correlations can’t be expected to persist forever. While there is currently little obvious damage being done to the Japanese economy by the weakness of the JPY, the extent of the weakness increases the chance that the Japanese authorities try to draw a line in the sand at some point quite soon.

There is a central bank meeting in Norway this week, but there is unlikely to be any change in policy or statement. However, the weakness of the NOK is almost as notable as the weakness of the JPY in recent years. The difference is that the NOK has come from a position where it was initially much more highly valued, but the NOK has been one of the few currencies that hasn’t exceeded its peak against the JPY set 2 years ago (in nominal terms). Given the likelihood that policy will continue to stay on hold for some time while rates elsewhere may decline, the NOK ought to have potential for recovery and may fare better than the JPY in a risk positive environment given its more attractive yields.

Data and events for the week ahead

USA

Highlights of a busy week in the US will be Wednesday’s FOMC meeting and Friday’s non-farm payroll. The FOMC statement is likely to see some adjustments to reflect recent disappointment on inflation while repeating that more confidence on inflation moving towards target is needed before easing. It is also likely that tapering of Quantitative Tightening will be outlined at this meeting, but this should not be seen as a dovish policy signal. Powell is likely to sound quite hawkish at the press conference.

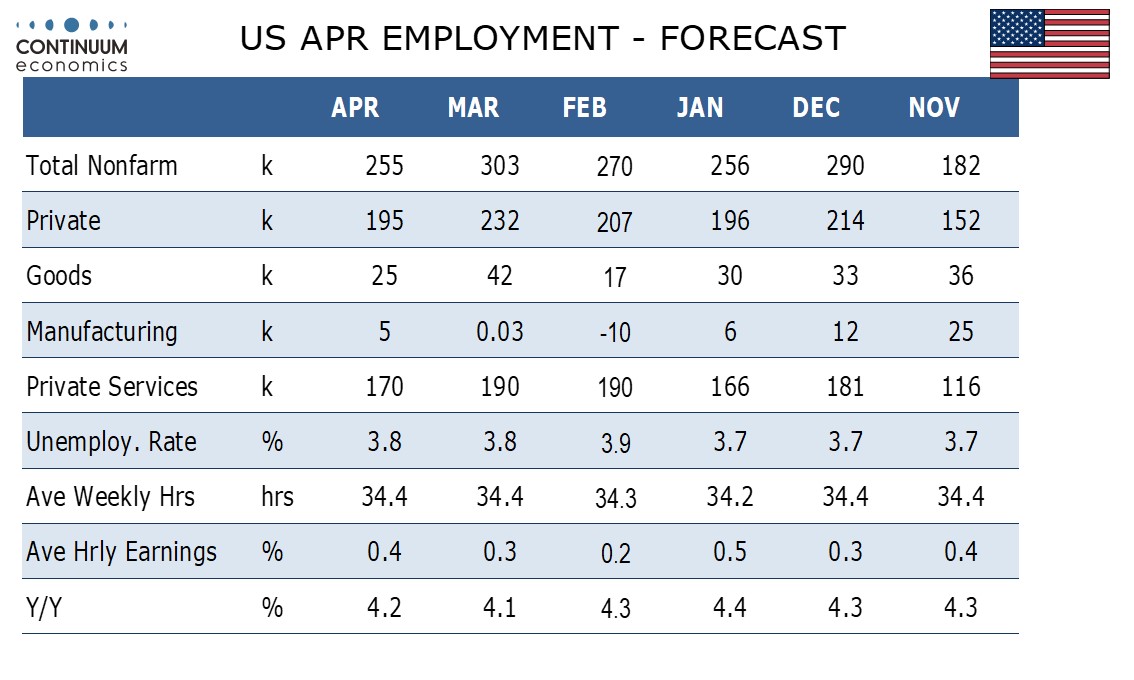

We expect a 255k increase in April’s non-farm payroll, still strong if the slowest since November, with a 195k increase in the private sector. We expect an unchanged unemployment rate of 3.8% and a slightly above trend 0.4% increase in average hourly earnings, lifted by a minimum wage hike in California. Ahead of the non-farm payroll (and the FOMC decision) we expect Wednesday’s ADP report to show a 150k increase in private sector employment. The FOMC will watch Tuesday’s Q1 Employment Cost Index closely. We expect a second straight rise of 0.9%. Other significant labor market signals will come from Wednesday’s JOLTS report on labor turnover, and on Thursday Q1’s productivity and costs report and weekly initial claims.

Monday’s calendar is quiet. Tuesday sees February House Price data from S and P Case-Shiller and FHFA, and April consumer confidence. April ISM surveys are due on Wednesday for manufacturing, where we expect a marginal increase to 50.5 from 50.3, and on Friday for services, which we expect to increase to 52.0 from 51.4. March construction spending is due on Wednesday. On Thursday we expect March’s trade deficit to increase to $69.2bn from $68.9bn. March factory orders are also due. Fed’s Goolsbee will speak on Friday.

Canada

Canada’s most significant release is February GDP on Tuesday, where we expect a 0.3% increase, slightly slower than the 0.4% preliminary estimate made with January’s report. April’s S and P PMIs are due for manufacturing on Wednesday and services on Friday. March’s trade balance is due on Thursday.

UK

A less busy week sees updated survey data with no major revisions expected in the final PMIs (Wed & Fri). More interest may be on Tuesday with fresh BoE-compiled money and credit data that may be of increasing importance. Firstly, they will show the extent to which cash-strapped households are still turning to borrowing to fund everyday spending. But secondly, they will highlight how BoE balance sheet reduction is having a wider impact, given the drop in bank deposits that has occurred if late, the question being to what extent is this adding to downward pressure on private sector credit.

Eurozone

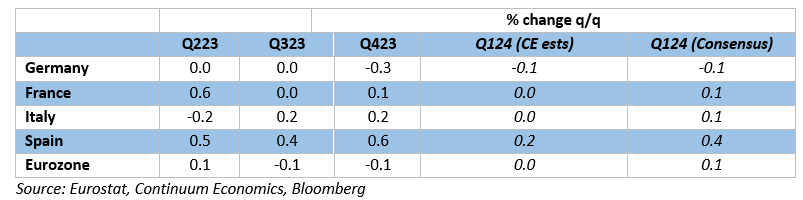

Datawise, it is a very busy week for high-profile numbers. Against a backdrop of marked, if not increasing, national growth divergences is likely to have continued into Q1 (data due Tuesday) where we see a flat overall EZ GDP q/q outcome masking moderate growth in Spain but a further slide in Germany. But there are upside risks. HICP data for the EZ arrives the same day. We see the headline staying at 2.4% in April but with the core down a further 0.2 ppt, as higher fuel prices are offset by some belated correction back in services inflation related to the early Easter distortion. German HICP is due Monday. We see both the headline and core easing a further 0.1 ppt in April data, the former to 2.2%, helped by an unwinding of early Easter distortions and in spite of higher fuel costs. EZ labor market data (Fri) may show belated rise in joblessness but also continued clear rise in the workforce.

Divergent Q1 EZ GDP Picture

There is also abundant survey data with PMI revisions likely to be modest (Wed and Fri), but where the European Commission survey data (Mon) may tell a more downbeat story.

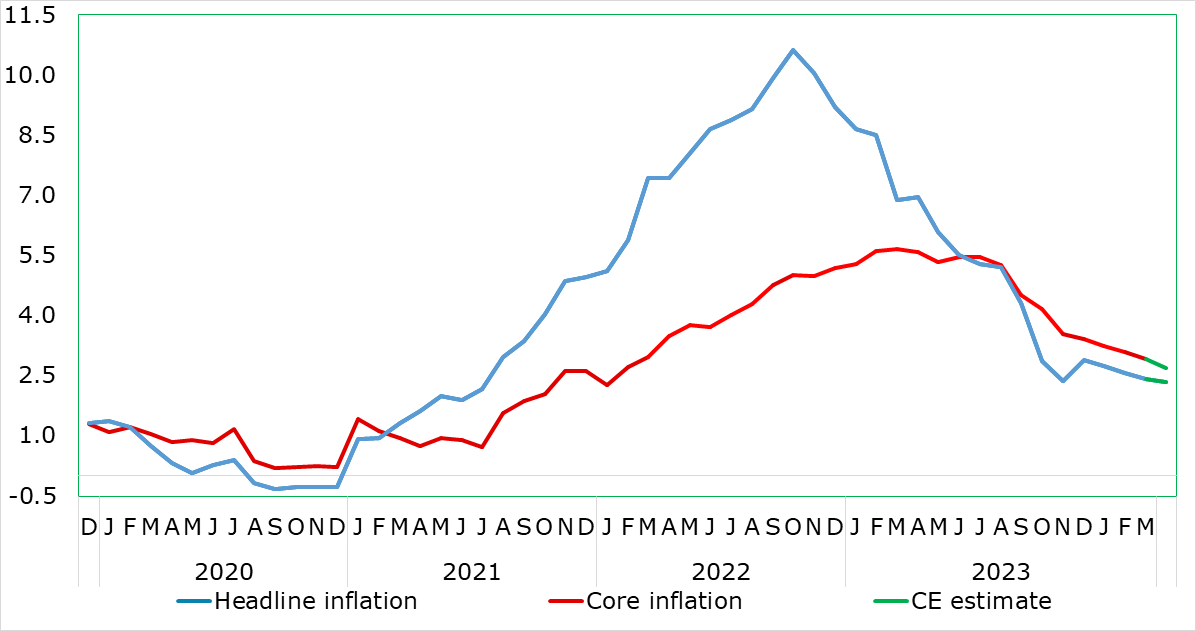

Stable Headline and Lower Core Inflation?

Source: Eurostat, CE

Rest of Western Europe

There are key events in Sweden, with m/m GDP indicator due on Monday, albeit the data plagued with volatility and revisions. Otherwise, Deputy Riksbank Governor Floden will discuss bond market matters. Switzerland sees CPI data (Thu) and where we some rise from the 1.0% March downside surprise may now occur due to base effects.

In Norway, the Norges Bank Board is very likely to leave its policy rate at 4.5% for a third successive meeting when it gives it next verdict on May 3. It is also likely to retain the thinking first aired at the December meeting, namely the ‘policy to stay on hold for some time ahead’ rhetoric.

Japan

The Japanese calendar next week starts on Tuesday, with unemployment rate, industrial production and retail trade. Of all, retail trade would be more important from our eyes as it gives us a glimpse in the coming domestic demand. It likely won’t be strong as real wage was still in negative territory and savings depleting. Else, we have the BoJ minutes on Thursday but very likely to be non-event as there was no major changes in this week’s BoJ meeting.

Australia

Australia also have retail sales on Tuesday but carries less weight as the Japanese counterpart for RBA’s focus remain on CPI because the Australian economic growth is healthier. Bunch of PMIs on Wednesday and Friday. Trade Balance on Thursday would be a good area to look into to assess the continuous strength of Australian export and the contracting domestic demand.

NZ

Business outlook and confidence on Tuesday is overshadowed by labor data on Wednesday. Within the labor report, labor cost index would be critical as thew RBNZ has been cueing for stronger CPI. However, the RBNZ has watered them down and stick to their OCR forecast for now. So unless there is a big beat, it will likely be not having a lasting impact in the market.