FX Daily Strategy: Europe, April 16th

GBP in focus on labour market and CPI data

Scope for a more dovish tone to emerge if earnings data soften further

EUR/USD downside looks more restricted from here

JPY likely to have bottomed out on the crosses

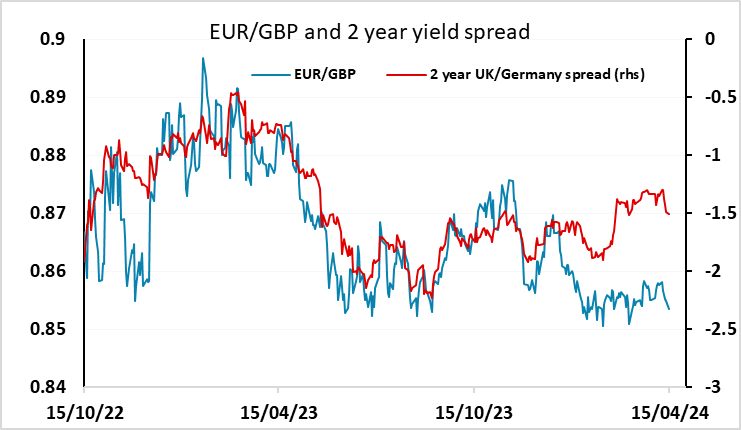

UK labour market data may bring rate cut expectations forward

Recent GBP strength may consequently see some retracement

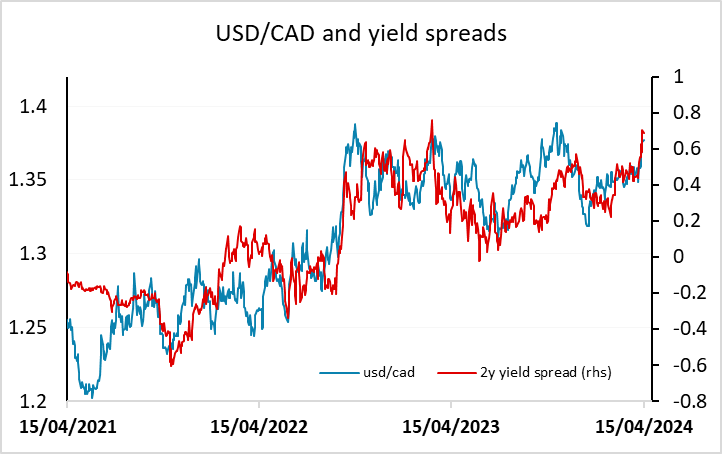

Canadian inflation should help USD/CAD to stabilise below 1.38

JPY intervention risk high

Tuesday sees UK labour market data and Canadian CPI numbers, both of which could potentially be market moving. The Bank of England MPC is very focused on the situation in the labour market, and particularly the growth in earnings. Unfortunately, the data is perceived to be quite unreliable, and there is probably more credibility in the HMRC payrolled employment data than the ONS’s own average earnings and employment series. The HMRC data is also more up to date, so is increasingly becoming the more important for the market. This data has showed a clear slowing in payrolled earnings growth in recent months, with earnings very little changed since November and the y/y of 5/5% the lowest since November 2021. While this is still too high to be consistent with the inflation target, a continuation of the flat trend of the last four months would strengthen the case for an early rate cut.

As it stands, the market is pricing almost no chance of a rate cut in May, in part because of the comments from MPC member Greene last week saying rate cuts should be “a way off”, in part because of the rise in US yields since the CPI data last week. But the UK is not the US, and although the latest UK activity numbers have shown a slight improvement, the trends in wages and inflation do suggest greater scope for an earlier rate cut. We believe the GBP curve should show a more similar rate cut trajectory to the EUR curve than the USD curve given the relative performances of the economies, and this suggests there is scope for UK yields to move lower if this week’s data continues to show an easing in wage and price pressure. GBP has been firm in recent days, with EUR/GBP testing the 0.8530 support level, but another flattish earnings number ought to see some retracement of recent GBP strength as the market moves UK rate expectations more towards the Eurozone.

We expect March Canadian CPI to move higher to 3.0% yr/yr from 2.8% in February and 2.9% in January, with the monthly data likely to look quite firm after two soft months. However we do expect some modest progress lower in two of the three BoC’s core rates. We expect the monthly data to show overall CPI up by 0.7%, with a 0.6% increase ex food and energy, before seasonal adjustments, though some of the increase will be seasonal. We expect seasonally adjusted data to show a 0.4% rise overall, lifted by gasoline, with a 0.3% increase ex food and energy. At the last meeting, the Bank of Canada made no policy changes with rates left at 5.0% and Quantitative Tightening continuing as expected. However the tone of the statement was significantly more optimistic on inflation, focusing more on this than recent signs of stronger activity. The BoC still needs to see progress on inflation sustained before easing, but looks likely to move sooner than the FOMC. Our forecasts for CPI are essentially in line with the market consensus, but the slightly edging up in y/y inflation data might lead to a modest rise in Canadian yields and help stabilise USD/CAD below 1.38.

Other than the UK and Canadian data, there is likely to be a lot of focus on USD/JPY, with potential for BoJ intervention rising as the JPY falls. The Japanese authorities were no doubt reluctant to oppose the rise in USD/JPY last week as it was a USD move, with the JPY actually strengthening on the crosses. However, Monday has seen the JPY weaken across the board, and this looks much more likely to be opposed. We continue to see the 165 area ain EUR/JPY as likely to be a hard level to hold above.