DM Government Bond Markets in Limbo

· DM central bank meetings in June will be crucial, with a high risk of a 25bps ECB hike to warn against 2nd round effects from higher oil prices and a BOJ 25bps hike as part of the ongoing normalisation. However, the tone that the Fed’s Warsh will set will also be key. The biggest issue keeping government bond markets in limbo however remains the negotiations over reopening the Straits of Hormuz. Our baseline remains that the U.S. and Iran do not want to restart the war and have economic incentives to agree a reopening of the Straits of Hormuz by July. If this comes before the FOMC meeting, then it will calm FOMC members and also the U.S. Treasury market.

· Elsewhere, 10-2yr yield curve are flattening alongside the U.S., which is normal when expectations switch to tightening. The exception are JGB’s, where the 10-2yr curve is steepening, which is a worrying sign. Fiscal concerns are being amplified by super aggressive BOJ QT (6% of GDP in 2026), though BOJ QT will likely be slowed in June.

Some have become concerned about the yield rises in DM government bond markets. What next?

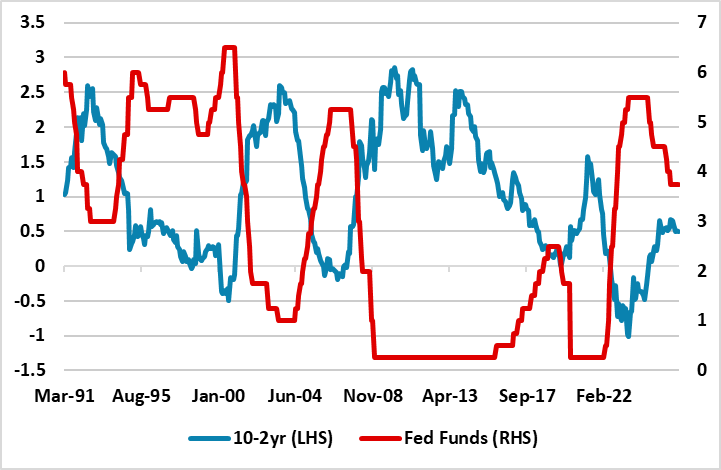

Figure 1: U.S. 10-2yr and Inverted Fed Funds (%)

Source: Datastream/Continuum Economics

Rising U.S. government bond yields since the outbreak of the Iran war have prompted apprehension of yet further yield rises. However, we would see it more reflecting a swing to discounting rate hikes and risk premium. If the market was really concerned about persistent inflation then the 10-2yr curve should steepen. Instead, a marginal flatten 10-2yr has been seen since the Feb 28 start of the U.S./Iran war and this is consistent with historical behaviour when the market swings to flatten when the market swings from easing to tightening expectations (Figure 1). Though money markets are now discounting a set of hikes from the Fed, incoming economic numbers will be crucial, both in terms of CPI inflation trends and the next NFP report. Interrelated to this is whether low to middle income consumers become more cautious in the face of the new CPI shock (here). Add in new Fed chair Warsh’s bias to ease on AI driving disinflation and it remains unlikely that the June 17 FOMC meeting will see the Fed actually hike. Even so, the FOMC meeting dots will be important alongside the statement (whether the easing bias is dropped) in setting expectations at the front-end and across the curve. It could be that the June FOMC itself does not bring relief to high U.S. Treasury yields.

The key swing factor are actually negotiations over reopening the Straits of Hormuz. Our baseline remains that the U.S. and Iran do not want to restart the war and have economic incentives to agree a reopening of the Straits of Hormuz by July (here). If this comes before the FOMC meeting, then it will calm FOMC members and also the U.S. Treasury market.

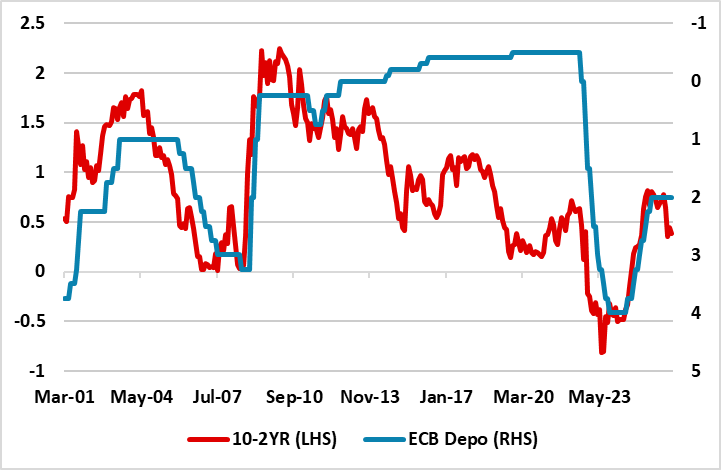

Other DM central banks should not be ignored. The key is the ECB on June 11, where it would be a surprise if the ECB does not hike given recent hawkish noises even from the doves/centrists. The reality of a 25bps ECB hike for the bond markets would cement expectations of a 2nd move and potentially more, which would lift EZ government bond yields across the curve. It would likely cause a spill over in other DM government bond markets. Though the RBA has hiked it is seen as an outlier, while the BOJ is seen to be in a normalisation phase from ultra-low interest rates. Even so, the 10-2yr German curve has become flatter since the start of the U.S./Iran war (Figure 2), which we would regard as normal when expectations switch to tightening. EZ yields are also in limbo from the outcome of the Straits of Hormuz negotiations, as a credible reopening would ease energy prices and pressure on the ECB.

Figure 2: Germany 10-2yr and Inverted ECB Depo Rate (%)

Source: Datastream/Continuum Economics

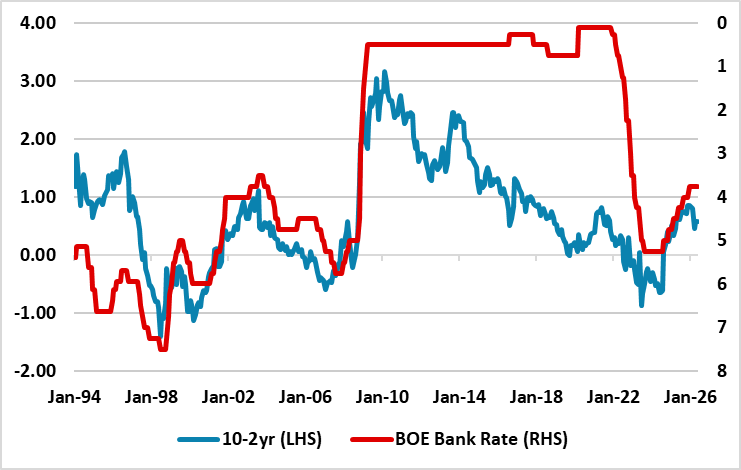

The BOE are also in the spotlight on June 18, but really the July meeting is key in line with the next monetary report and new inflation forecasts and given that the UK economy is soft in contrast to the U.S. Despite the political fears of a shift of Labour government policies to the left, the 10-2yr curve is flatter since the start of the U.S./Iran war (Figure 3), which reflects tightening fears.

Figure 3: UK 10-2yr and Inverted BOE Policy Rate (%)

Source: Datastream/Continuum Economics

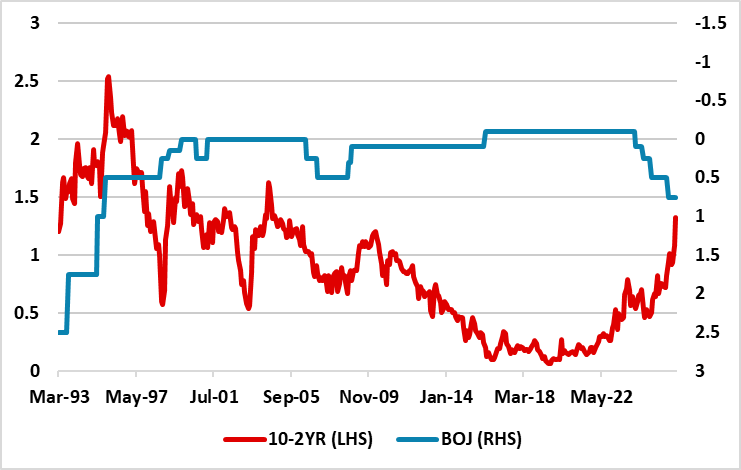

Japan is the odd one out for government bond markets, with a clear steepening of the 10-2yr JGB yield curve (Figure 4). This reflects concerns about fiscal easing, but is also a function of super aggressive BOJ QT. We estimate that the BOJ QT will be nearly 6% of GDP in 2026, which is much larger than the ECB or BOE and in sharp contrast to new Fed balance sheet expansion in line with nominal GDP. We remain of the view that JGB yield rises are now getting to the point where the BOJ could slow the increasing the pace of QT (more likely) or do a partial U turn. The annual review is due in June and would likely come alongside a 25bps BOJ rate hike on June. This could partially reverse the steepening in JGB’s.

Figure 4: Japan 10-2yr and Inverted BOJ Policy Rate (%)

Source: Datastream/Continuum Economics