ECB: Bark No Bite

· The vigilance mantra means that the ECB will still have a broad caution against 2nd round effects and the risks that energy prices could push higher. We feel that the June inflation data, plus the prospect that Iran/U.S. could call a new truce (here) will be enough to make most on the council reluctant to give strong guidance on the September meeting. Most ECB officials will also want to see more data and the new September staff forecasts. Lagarde will thus likely try to balance broad guidance, with a reluctance to provide a clear hint on the September meeting.

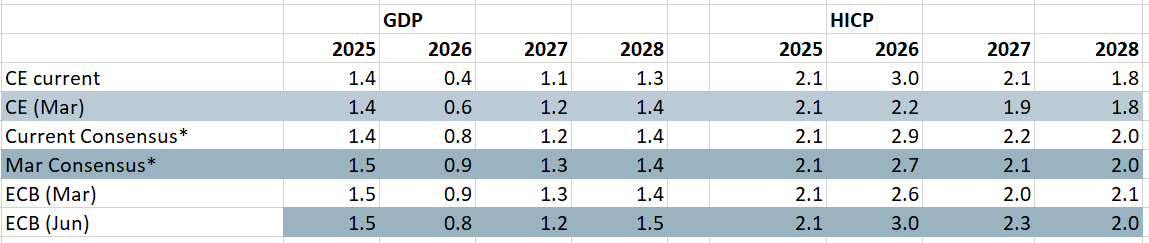

Figure 1: Economic Outlook from Various Perspectives

Source: CE, ECB, Consensus Economics

The July 23 ECB meeting is not expected to see a change in policy rates, with the key focus being on the forward guidance.

· Unchanged Policy Rates. The messaging around the June 25bps rate hike had already left the market feeling that back to back hikes would not be forthcoming. The U.S./Iran MOU and associated decline in energy prices has only reinforced the view that July will see a hold. Though the last 4 days of Iran and U.S. counterstrikes have strained the MOU to breaking point, ECB officials will not want to assume that energy prices will be on a higher path for the remainder of 2026. Additionally, though oil prices have picked since last week, it is noticeable that TTF gas prices have only risen from EUR42 to EUR41.5. The demand/supply balance in the global gas market are less stretched, but gas and any associated boost to electricity prices is really important to the EZ inflation picture. The June HICP data also shows no 2nd round effects and underlying control in the inflation picture (here), which would argue against a further rate hike.

· Broad forward guidance, not September. Even so, the vigilance mantra means that the ECB will still have a broad caution against 2nd round effects and the risks that energy prices could push higher. With the U.S./Iran MOU fragile, this is a stance that the hawks and the doves can agree upon. However, this is a general bark rather than guidance on another bite in terms of a September rate hike. Some of the hawks (e.g. Nagel on Wednesday) sound like they are not pushing for a September hike in contrast to the money market that is fully discounting a 25bps hike at the September 10 meeting. We feel that the June inflation data, plus the prospect that Iran/U.S. could call a new truce (here) will be enough to make most on the council reluctant to give strong guidance on the September meeting. Most ECB officials will also want to see more data and the new September staff forecasts. Lagarde will thus likely try to balance broad guidance, with a reluctance to provide a clear hint on the September meeting.

· 2027 rate cuts. We remain of the view outlined in the June Outlook (here) that the ECB will not hike further, both as the economy turns out softer than ECB forecasts and controlled wage inflation helps to drag down service inflation and core CPI. Indeed, by 2027 we feel that slowing Next Gen EU infrastructure spending will be a new headwind and that this will see some further disappointment on the economy and disinflation pressures will remain (financing conditions are tighter than the level of the ECB depo rate). Overall, we still see two 25bps cuts in 2027.