Eurozone Outlook: Has Inflation Peaked Already?

· Under our only slightly updated view of no further fighting in the Middle East, we see oil and gas prices largely consolidating recent falls before falling afresh from mid-2027.The current situation is very different from that of 2022 and the Ukraine War in which the EZ lost access to Russian gas as that ‘shock’ was super-imposed on an EZ economy where demand was recovering from the pandemic amid clear shortages.

· Even so, we now see 2026 HICP inflation some 0.3 ppt higher than envisaged three months ago, averaging 2.5% but where it may already have peaked. A dip back below 2% is on the cards by mid-2027, with the HICP outlook on average for 2027 little changed at 1.8%. There is also a weaker real economy, hit not just by what will be a lingering impact of the Middle East conflict but also from financial conditions remaining tighter.

· While the ECB has now underscored that a least one further rate hikes is certainly possible, we still regard the next move in rates to be a further cut (probably a 25 -50 bp move) but now sometime next year, something that the real and monetary economy may very well be demanding.

Our Forecasts

| GDP Growth | HICP Inflation | Discount Rate (%) | |||||||

| 2025 | 2026e | 2027e | 2025 | 2026e | 2027e | 2025 | 2026e | 2027e | |

| Eurozone | 1.5% | 0.4% | 1.1% | 2.1% | 2.5% | 1.8% | 2.0 | 2.25 | 1.75 |

| France | 0.9% | 0.4% | 0.8% | 0.9% | 2.4% | 1.9% | - | - | - |

| Germany | 0.3% | 0.6% | 1.5% | 2.2% | 2.6% | 1.9% | - | - | - |

| Italy | 0.6% | 0.5% | 0.6% | 1.7% | 2.9% | 1.9% | - | - | - |

| Spain | 2.8% | 2.0% | 1.4% | 2.7% | 3.1% | 2.2% | - | - | - |

Source: Continuum Economics

Eurozone: Inflation Rise Over?

We still think the ECB and the consensus are, and will remain, too pessimistic about inflation and too optimistic about growth. Despite what have been clearly weak business survey data and weak growth numbers, the cumulative downgrade to the GDP outlook just made by the ECB over three years is a bare 0.1 ppt. Given the recent Q1 GDP downgrades unearthed earlier this month the ECB is effectively assuming 2% ann. rate growth per quarter for the rest of the year. Admittedly, this downgrade is a reflection of anomalies in Irish national accounts without which EZ GDP would have growth nearer 0.4 q/q of late. But when the ex-Ireland GDP numbers were labouring over a year ago, the ECB was happy to take the headline numbers at face value and even as a sign of better supply conditions. Indeed, it is notable how little the GDP outlook varies among the (now) four scenarios the ECB is offering, with the ECB suggesting all are consistent with the need for at least this hike.

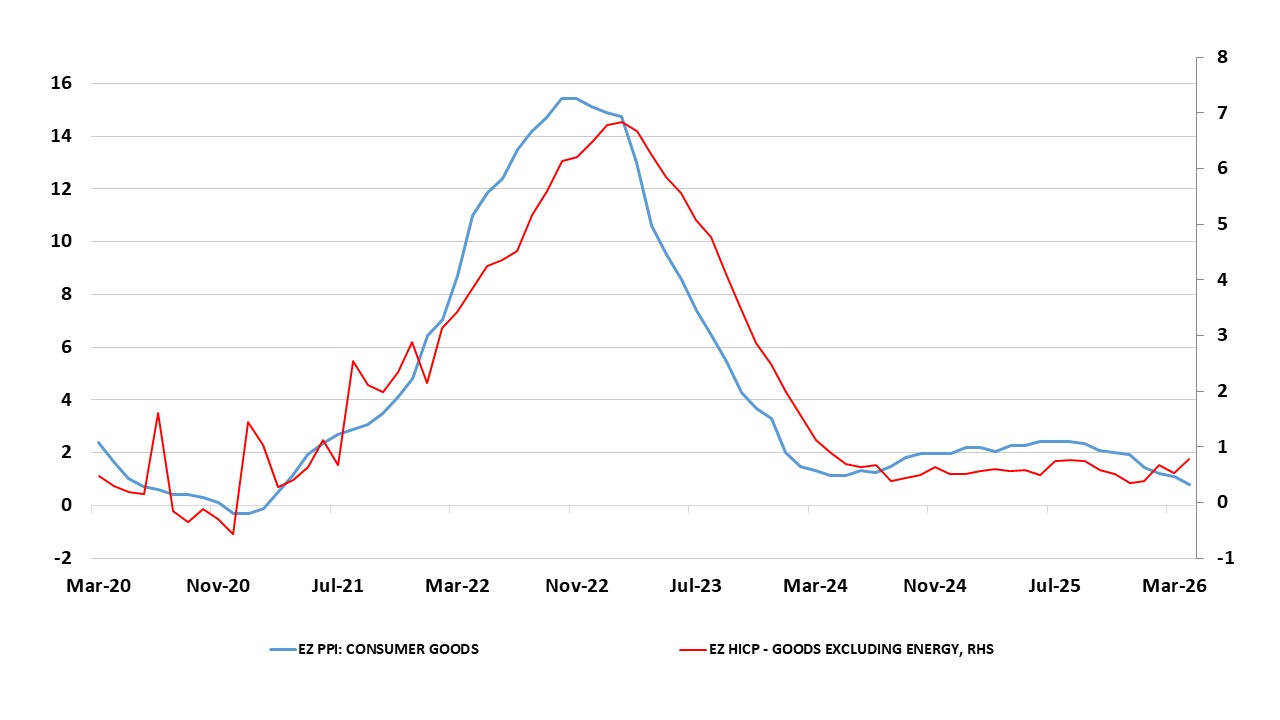

But the HICP outlook and backdrop are not all pointing to the upside. As Figure 1 shows, this is far from the case as consumer goods PPI inflation data (up to April) has reached new lows at under 1% y/y, and suggests little sign that HICP core goods has started to show genuine upward momentum. Furthermore, noting higher services inflation last month ignores the strong likelihood that this is mainly a calendar effect due to the timing of Easter. Moreover, rather than continuing to rise thorough the summer as the ECB and consensus hints at, already falling fuel prices may start to pare back overall HICP numbers from this month on – fuel prices could knock some 0.2 ppt of the figure for June, thereby taking it back below 3% and suggesting last month was the peak headline rate. And of course, this also sits alongside continued signs of softer wage growth, something that sits uneasily with services inflation moving in the opposite direction – at 3.2% out to 2028 the ECB projection for employee compensation sits well with the 2% HICP target

Indeed, and arguing against any clear wage spiral emergence, an ever-wider array of survey data suggest also that job losses are also starting to become worryingly widespread as business confidence spirals down. Notably, the service sector is being hit especially hard by the cost surges created by the war. Moreover, what is even more notable is that supply shortages not only pose upside risks to prices but can and seem to be constraining real activity already and probably more so in the coming months. With this in mind, how little the ECB revised its real economy outlook this month is as important as how inflation was altered, the former very much helping determine both the size and persistence of any price shock – one that does seem to be increasingly supply related. Indeed, the case can be made that 2026 GDP growth could be as low as 0.2%, although we have factored a more conservative 0.4%, this down 0.2 ppt from what was envisaged three months ago but which may forgo any near GDP drop in q/q terms. We have also pared back the 2027 and 2028 outlooks each by a notch. These factors highlight our below-consensus GDP outlook, one that comes very much with downside risks that reflect obvious adverse global factors and real income damage from higher fuel prices, but also ECB policy. Several factors explain this outlook

Instead, ECB policy is biting adversely (either directly or indirectly) through three channels. Firstly, financial conditions have tightened even further, underscoring that the discount rate was and is a poor guide to the policy stance. Secondly, the ECB is still drawing down its balance sheet with excess liquidity (at EUR 2.4 trillion) having halved from its peak and set to fall toward EUR 1.5 trillion by end-2027. Since the ECB’s bond portfolios very well might continue to shrink even then, the idea is that regular liquidity operations would become more used by banks to offset that effect. Then, at some point, the ECB would introduce structural liquidity operations. Thirdly, as lending surveys have repeatedly shown, banks are not just more reluctant to lend but are actually rejecting an increasing amount of possible loans, especially those that have less collateral attached (Figure 2). Furthermore, even with the recent U.S. Supreme Court ruling suggesting otherwise, the EZ seems locked into 15% tariffs given its trade deal. Regardless, overall rifts with the U.S., and especially still over trade, maybe growing. The US is throwing a huge invite-only party for more than 5,000 diplomats, politicians and officials in Brussels on 28 June to mark the 250th anniversary of US independence. But very Few of the EU hierarchy are going.

Policy also assumes that changes in ECB rates have been fully passed on by banks to borrowers, something that does not seem to have been the case during the most recent easing cycle. Indeed, while the ECB discount rate (now back up to 2.25%) is some 2 ppt below the peak last seen in mid-2024, the effective cost of borrowing for firms has fallen by only 1.5 ppt while that for household by a puny 40 bp! All of which will take its toll on HICP inflation, not least given some disinflationary moment evident before the Middle East conflict. But while we largely echo an upgrade to the 2026 HICP pictures to an average of 3.0%, we see an earlier and faster slide such that y/y HICP rate may be back below 2% by mid-2027.The core rate is largely seen shadowing, albeit recognising the upside risks that fresh supply problems that Middle East conflict has already precipitated and may do further yet.

But there are so some other upside growth risks as both the German fiscal stimulus and EU-wide defense build-ups take effect, this actually pointing to a gradual an underlying q/q pick-up in GDP from late 2026. This outlook reflects a host of uncertainties, some to do with the timing of likely fiscal and defense initiatives, divisions within the German coalition and some to do with to what degree they may boost EZ growth only modestly due to the likely large import content. As for impact on the current account balance, the anticipated cyclical, and possibly structural, recovery in imports seen ahead, as well as what may be a weak global economy weighing on exports, will also mean that the improvement in the current account surplus last year (at around 2% of GDP) may reverse into 2026 and possibly even more so in 2027. This though is a headwind to GDP growth.

Figure 1: Despite ECB Thinking, Not Everything Suggests Price Pressures Broadening Out

Source: Eurostat, CE, % chg y/y

Fiscally, to suggest the backdrop and outlook is mixed would be an understatement, now clouded further by higher borrowing costs and from actual government interventions to reduce the spike in oil and gas prices for consumers and, to a lesser extent, firms. The overall EZ budget situation is likely to see small increases to above 3.5% of GDP into 2027, with the primary deficit slightly higher at -1.5% and the structural gap similar to the headline numbers. But this masks marked differences among EZ members, not least the Big 4 we assess in the Outlook. Regardless, the fall in the EZ government debt ratio to 87.5% of GDP last year will likely soon be followed by a rise toward 91% in 2027. These fiscal divergences raise policy question and make the job of the ECB harder; it is thought the central bank may wish to be more vocal in its fiscal criticism through 2026. But this may make it harder to use its TPI tool on any credible basis if what are current fiscal problems turn into genuine crisis (most notably in France).

ECB: How Was the Hike Not Insurance? Not Such a Good Place

The 25 bp official rate hike unveiled this month was so well-flagged it is hard to suggest that it is consistent with a decision process on a meeting-by-meeting basis. Similarly, the clearer shift by the Council toward a pre-dominance of inflation upside risk thinking, alongside another dose of optimistic real economy projections, is hardly proper data-dependency. All of which shows where the ECB focus lies albeit where a more sustained Middle East ceasefire should put a restraint on ECB hawks, not least if headline inflation has peaked. Thus while the latest ECB projections show HICP inflation back in line with target by Q4 next year, a view based around the then market view of around three 25 bp hikes, such speculation has backed off since and may continue to do so - the question then being if and when easing thinking returns. But as suggested above, the projections show hardly any further damage to the GDP picture. Even with some relatively rapid energy prove resolution, we think the ECB is underplaying the combination of tight(er) financial conditions, banking sector reservations and weak sentiment that should combine to pull HICP inflation back to, if not below, 2% by mid-2027 and thus create both rationale and room for fresh policy easing. While a further hike cannot be ruled out given the ECB’s biased reaction function, we think that this 25 bp hike is more than enough and that this misplaced move will be more than reversed into 2027 (i.e. thinking largely siding with the OECD). However, it is the case that the ECB is still reverberating from the 2022 energy shock and criticism it faced of hiking both too late and too slowly. If so, the ECB is getting confused. What is notable is that this energy shock and the ECB’s positioning is very much different to that of 2022, occurring at a point when the EZ economy is operating with a margin of spare capacity as opposed to one reviving from a pandemic induced demand shock. This is accepted clearly by the ECB! All which to us suggests that the ECB has repeated the kind of policy mistake it presided over in both 2008 and 2011. It may be the case that the ECB is once bitten, twice shy but will be thrice wrong!

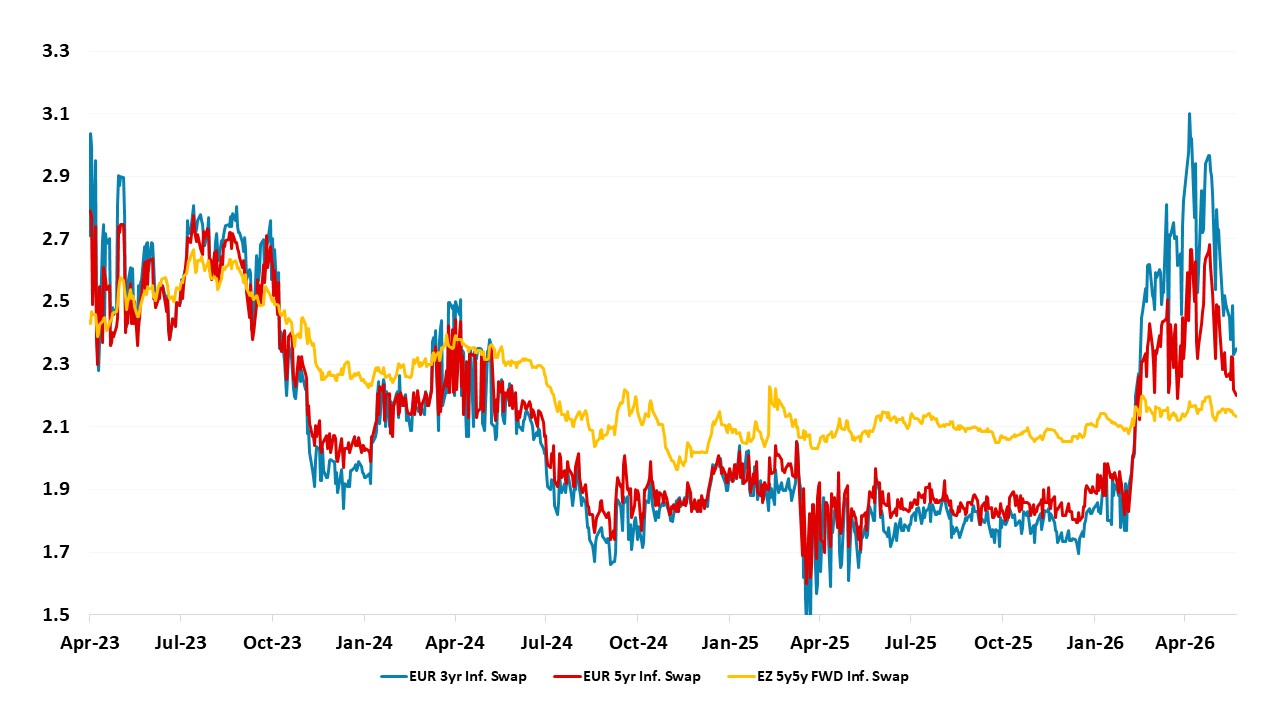

Figure 2: Inflation Expectations – What Goes Up…….

Source: DataStream