DM ex U.S. EZ Outlook (Japan and Western Europe): Navigating the Post Iran War Period?

· We have revised 2026 Japan GDP only slightly lower to 0.8% as wage growth is solidly above 3%, which will support consumption for the rest of 2026/27. The extension of energy stimulus will cap headline inflation for Q2/Q3 2026. For the BOJ, despite hawkish forward guidance, the 1% rate will be steady until spring wage negotiation in 2027, when we see another 25bps hike in Q2 2027. More importantly, bond purchase tapering will pause from April 2027 and keeping monthly bond purchase at ¥2 trillion. Even so, the substantial JGB redemption is still pointing towards an aggressive reduction in BoJ's balance sheet that will push long-dated JGB yields higher (here).

· For the UK, an upward revision to 2026 but downward to 2027, as the underlying softness of the economy and labor market acts as a drag. Changes in the government also raise fears of more tax hikes and act as a headwind. This can stop the BOE hiking and we still see 50-75bps of cuts in 2027.

· For Switzerland, 2026 GDP growth will be soft for a World cup year and combined with domestic disinflation should be enough to sustain zero SNB policy rates until mid 2027 – then the SNB will likely start thinking about slow normalisation.

· In Sweden, we see no Riskbank hike, despite a mild tightening bias. Underlying inflation remains well controlled, while the U.S./Iran interim deal should bring energy prices lower into 2027. For Noway, the Norges bank are signalling a risk of hike by November, but we feel this will not be delivered. Indeed, underlying inflation should help to deliver easing into 2027 (Our Forecasts below).

Our Forecasts

| GDP Growth | Inflation | Policy Rates (%) | |||||||

| 2025e | 2026e | 2027e | 2025e | 2026e | 2027e | 2025e | 2026e | 2027e | |

| Japan | 1.1% | 0.8% | 1.0% | 3.1% | 1.7% | 2.2% | 0.75% | 1.00% | 1.25% |

| United Kingdom | 1.3% | 1.0% | 1.0% | 3.4% | 3.2% | 2.3% | 3.75% | 3.75% | 3.00% |

| Sweden | 1.8% | 1.4% | 1.7% | 0.7% | 0.9% | 1.4% | 1.75% | 1.75% | 1.75% |

| Switzerland | 1.3% | 1.0% | 1.2% | 0.2% | 0.6% | 1.1% | 0.00% | 0.00% | 0.25% |

| Norway, mainland | 1.8% | 0.9% | 1.6% | 3.0% | 3.2% | 2.1% | 4.00% | 4.25% | 3.50% |

Source: Continuum Economics

Japan

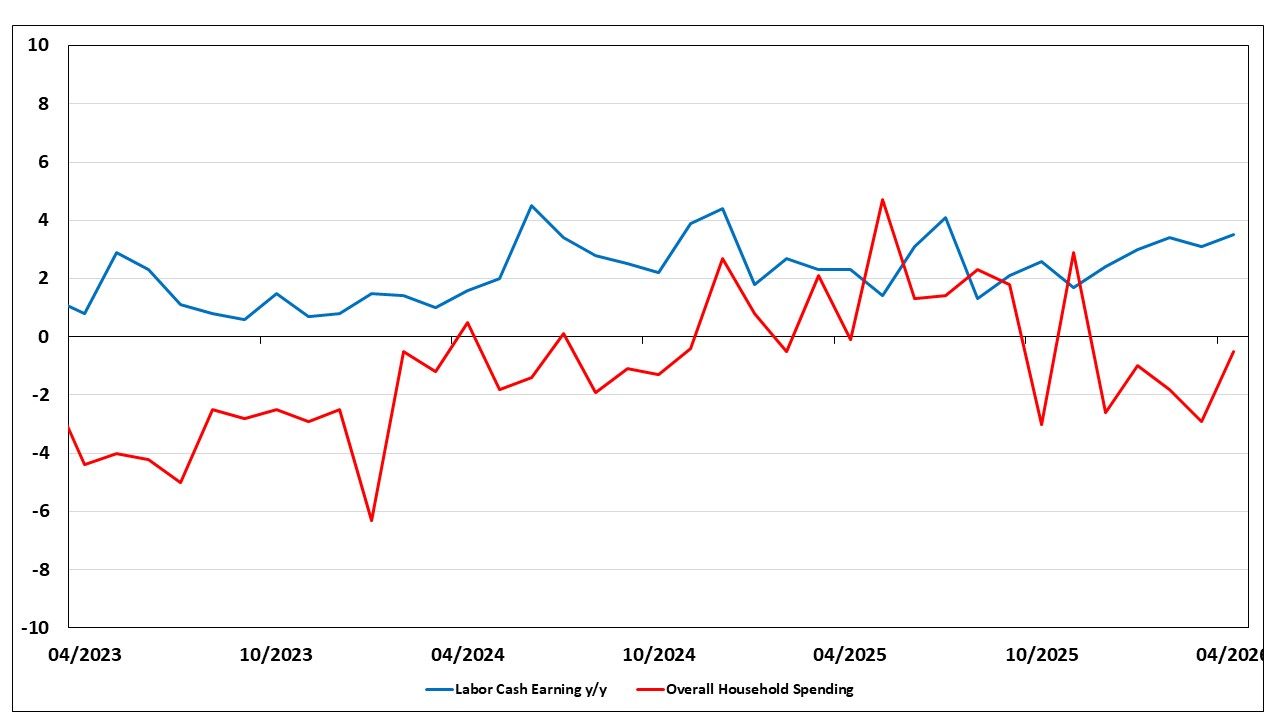

Figure 1: Overall Household Spending and Labor Cash Earning (y/y)

Source: Continuum Economics

Real wages have risen for a fourth consecutive month, expanding by 2.1% y/y in April 2026. This momentum was fueled by the historic 2026 spring wage negotiations, which closed with a 5.3% average headline increase and a 4.1% boost to total compensation, the strongest wage growth since the early 1990s. Household spending remained slightly sluggish due to rising utility and food costs.

PM Takaichi’s stimulus remains fully in motion. The one-time cost-of-living measures, including the ¥7,000/household energy subsidies and rice coupons, were extended through Q2 to offset the pressure from imported inflation. In early June, the Lower House swiftly passed a ¥3.11 trillion supplementary budget to cushion households and businesses from the energy shock. While the package will be financed by debt, the issuance will be partially offset by ¥3 trillion in unissued deficit-covering bonds from the previous fiscal year.

The trade balance remains under pressure from U.S. tariffs, but the diversification strategy toward Asian and EU markets continues to cushion the manufacturing sector. While the weak JPY keeps Japanese exports attractive, we expect net exports to moderate through late 2026 and 2027 as strengthening domestic demand and elevated global energy costs drive import values higher.

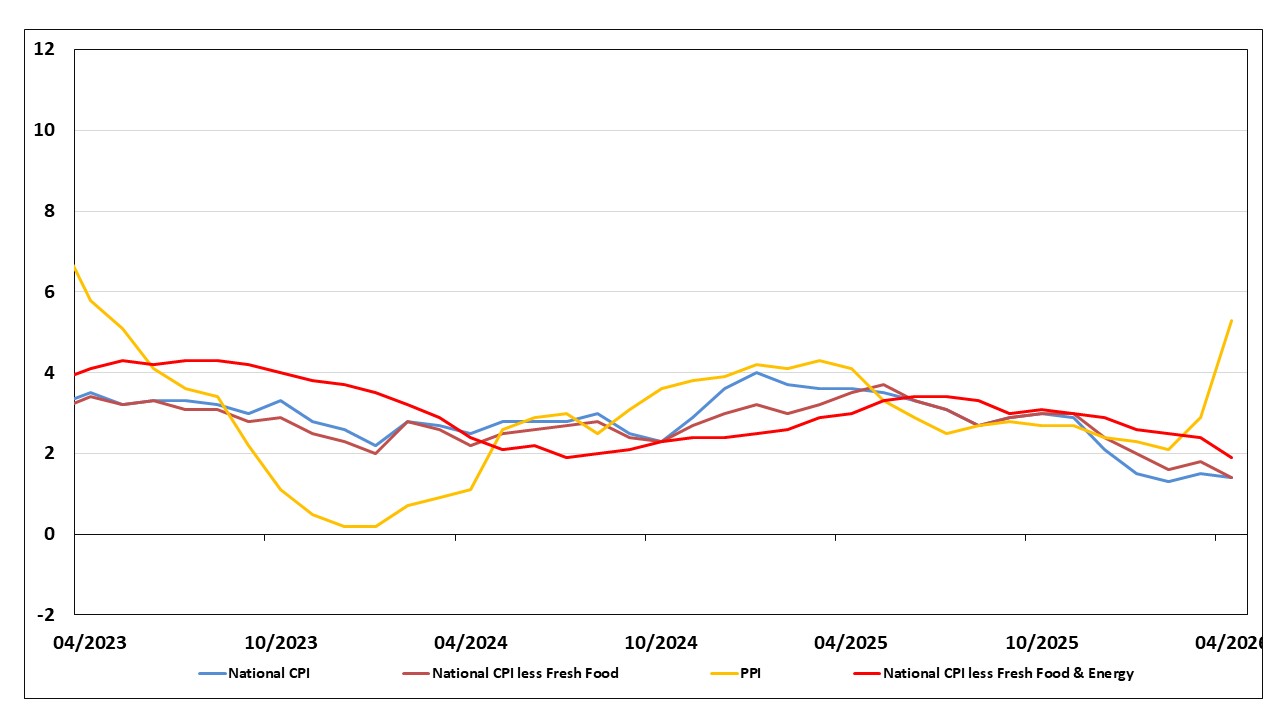

Figure 2: Japan National Headline CPI, less fresh food and less Fresh Food & Energy CPI and PPI (y/y)

Source: Continuum Economics

Our forecast for 2026 GDP is revised to +0.8% as private consumption is growing slightly below our estimate during the Middle East uncertainty. While the "Takaichi stimulus" was a crucial buffer, its net impact on growth has been partially neutralized by the persistent high energy prices, meaning the package will contribute less to overall expansion than initially anticipated. Nevertheless, we project moderate consumption growth through the remainder of 2026 as real wages accelerate, providing a solid floor for domestic demand.

We have revised our 2026 CPI lower to +1.7%, factoring in the artificial suppression of inflation by strong government stimulus. While the Japanese government’s subsidies have successfully cushioned the headline impact for households, the risk of underlying inflation deviating upward due to high B2B energy costs filtering through to a wider range of items cannot be ruled out. For 2027, our central forecast is revised higher to 2.2%. We anticipate the gradual moderation of cost-push effect from global energy markets to fade while demand-pull inflation to take over as the primary driver, supported by the virtuous cycle of rising wages and consumer spending. It should bring the Japanese economy toward a more stable, sustainable equilibrium consistent with the BOJ’s long-term targets.

Following the June 16 decision to raise the policy rate to 1%, the highest level since 1995, the central bank has signaled its intent to continue normalizing monetary policy if the 2% sustainable inflation outlook holds. While the conflict in the Middle East initially created uncertainty, the BoJ concluded that the risk of a significant economic slowdown has decreased, justifying the hike as a necessary step to curb inflation and support the yen.

BoJ's commitment to a steady decline in its monthly JGB purchases holds. The quarterly reduction of ¥200 billion will continue until March 2027 and keeping its monthly bond purchase at ¥2 trillion from April 2027. The move suggests the central bank is allowing market forces to play a larger role in determining long-term yields as they are forecasting ¥45 trillion from April 2027-March 28 with huge JGB redemptions, which is essential for the transition to a normal interest rate environment. However, if yields spike (sharp move above 3% for 10yr JGB yields), we expect the BoJ to deploy emergency bond-buying operations or adjust its tapering trajectory to try to stabilize market sentiment.

Moving onward, we maintain our forecast for a prolonged "hawkish hold." Now that the 1% threshold has been reached, the BoJ will likely prioritize allowing the economy to digest this higher interest rate environment. This approach balances the need for domestic demand support with the ongoing reduction of its balance sheet, ensuring that monetary policy remains enough to anchor inflation without prematurely stifling the post-deflation recovery. If we see another strong spring wage negotiation in 2027 (above 3%), the BoJ could bring rates to 1.25% in Q2 2027.

UK

The June MPC minutes show that 6 MPC members take the view that recent data outturns provided some further evidence that underlying disinflation had been on track pre-conflict. Secondly, that upside risks to energy prices had receded, although they remained higher than pre-war. Finally, that the higher interest rates facing households and businesses were already acting to reduce inflation over time and therefore a hold in Bank Rate at this meeting was appropriate. This all suggests that the gang of 6 are not for hiking in the coming meetings (Catherine Mann was between the two camps, but did not join Greene/Pill in calling for a rate hike). Additionally, BOE governor Bailey showed only a mild tightening bias, though could fade by the time of the new forecasts scenarios in the July monetary policy report. We expect the July report to be less hawkish and turning dovish by the November 5 monetary policy report.

It is also notable that Governor Bailey has recently referenced the approach of the BoE in 2011, which kept rates on hold even as UK energy inflation soared to 20%, citing its mandate to tolerate deviations from target in a bid to avoid unnecessary harm to the economy and jobs. A BoE survey of senior executives released of late offered tentative support for Bailey’s implicit wait-and-see approach (or what he prefers is an ‘active hold’), with evidence that companies will resist inflation-fuelling pressure from workers for higher wages in response to the current crisis. The expected price growth reading in the regular BoE-compiled Decision Makers Survey is among the weakest since 2022 and we would also point to pay growth already broadly consistent with the BoE’s inflation target. The survey also showed expectations for employment growth remaining in clear negative territory. All of which adds to a picture of a UK economic backdrop vastly and increasingly different to four years ago.

On fiscal policy, the change of Prime minister could mean a change in Chancellor and raise concern that the shift left could trigger fiscal easing. Even so, this is unlikely to deliver substantial new net fiscal easing in 2026-27 and fiscal worries should be lower after the autumn budget. The focus will be on improving the feel good communications and execution of existing plans, with some modest additions. Fiscal policy will thus continue to have mixed effects on the outlook over different years (given multi year tax hikes), but the wider economic for the BOE.

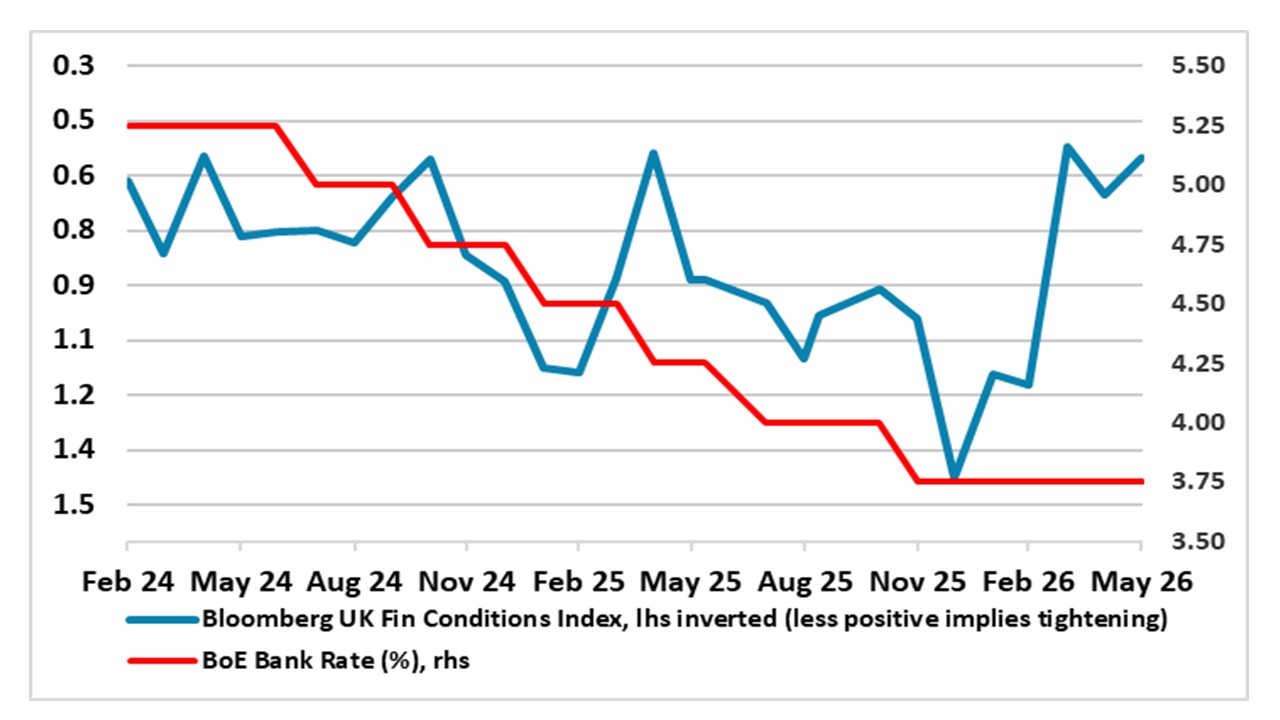

Figure 3: Official Rate Level Far From the Whole Story

Source: BoE, Bloomberg, CE

Given ever tighter financial conditions, we still see at least two and probably three more 25 bp rate cuts ahead but now deferred to starting no sooner than Q1 2027 and then extending through 2027 (a moderate probability exists that the 1st cut could be Q4 2026). As for the three scenarios (A seeing energy prices follow market thinking while C sees not only higher energy costs but more persistently too) we are puzzled that the combination of the energy shock and more restrictive policy not only fails to deliver any kind of recession even in the most severe scenario but that all three outcomes see little variation in the growth outlook – i.e. just 0.1 ppt per year between each outlook. We await the new July 30 forecasts.

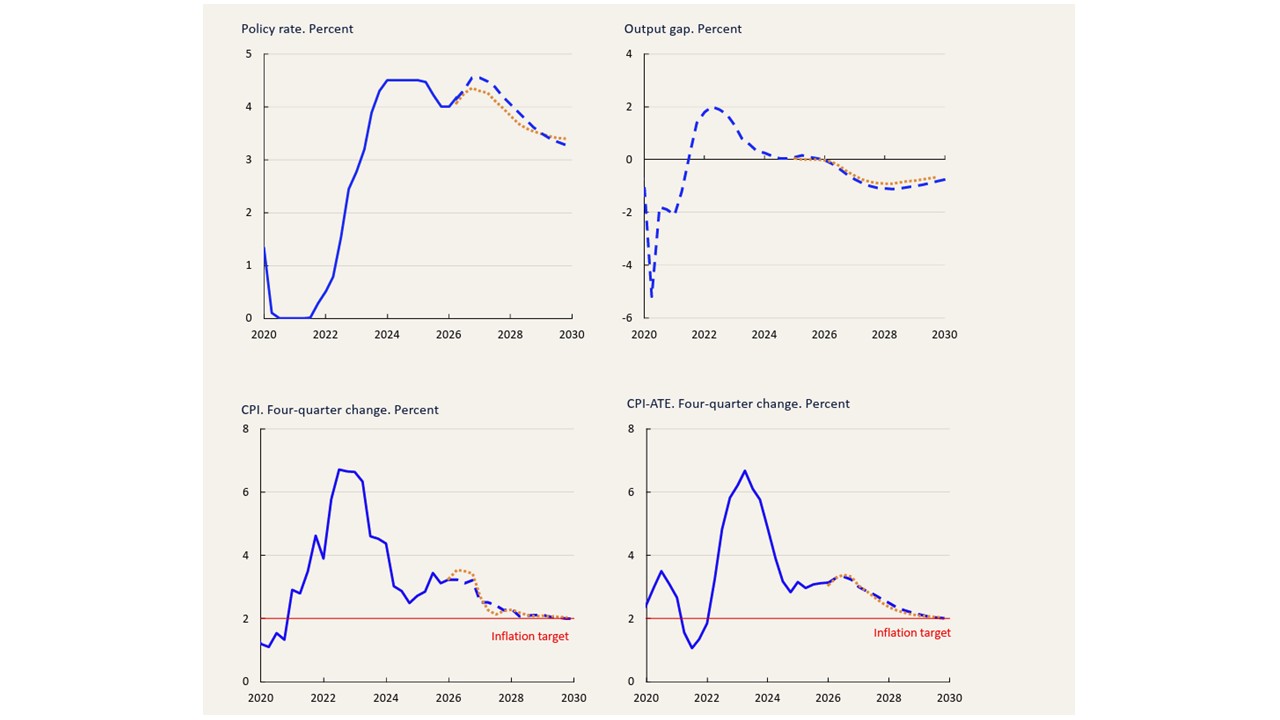

Sweden

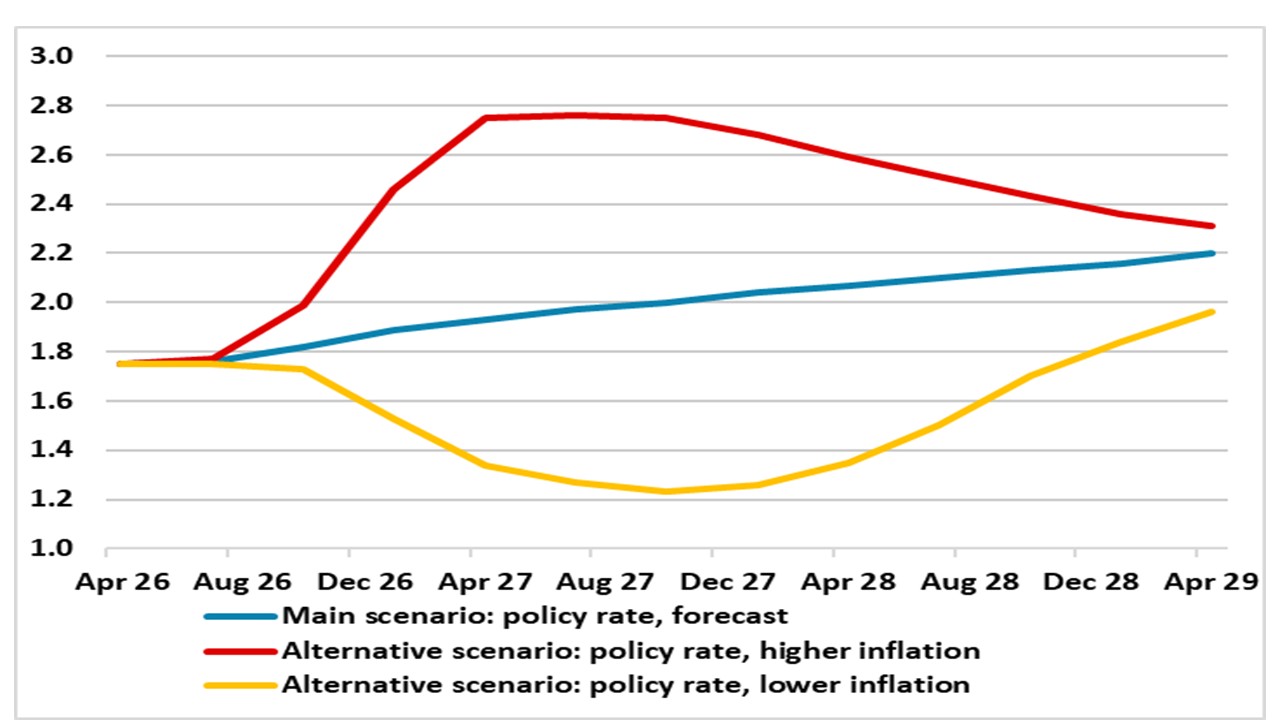

We still see stable policy though to end-2027 for the Riksbank rather than the small hikes markets and the Board are now pricing for late 2026. A similar profile has been offered by the Riksbank since last autumn (Figure 4) and it did bring forward its first hike hint a touch when it presented its updated June Monetary policy report. Somewhat better data in the last quarter on both the GDP and CPI fronts may even harden this guidance.

Figure 4: Riksbank Policy Rate Outlook Scenarios

Source; June 2026 Riksbank Monetary Policy Report

Regardless, the June Board analysis is partially out if date, not encompassing the recent Iran ceasefire deal and the marked drop in energy prices. Even so, the update suggests that CPI inflation in Sweden is still low, largely due to the dampening effects of fiscal policy measures. Economic activity is somewhat weaker than normal and growth was lower than expected in the first quarter. Moreover, the recovery in the labour market is tentative.

The Executive Board therefore decided to leave the policy rate unchanged at 1.75 per cent. Underlying inflation is low and economic activity is somewhat weaker than normal, but at the same time the supply disruptions have led to a rise in inflationary pressures and increased the risks of inflation being too high. Against this backdrop, the Executive Board has raised the policy-rate forecast somewhat, but assesses that it is well-balanced to leave the policy rate unchanged at present. The forecast means that the probability of the rate being raised later this year has increased compared to the assessment in March.

But there is considerable uncertainty and the developments call for vigilance. In addition to the war in the Middle East, there are also other risks that could affect the outlook for inflation and economic activity. There is also a possibility that the effects of the war will interact with other more underlying vulnerabilities in the global economy, such as high equity valuations and unsustainably high public indebtedness. The range of potential outcomes for what can happen going forward is wide and the Riksbank is highly prepared to adjust monetary policy, presumably this implies a move in either direction ultimately. But a clear but modest hiking bias remains even on a more benign inflation, albeit as for the later any such hikes would follow clear further easing.

Norway

The June Norges bank statement had a hawkish bias with a higher policy rate profile than in March MPR (Figure 5) and concerns voiced again over persistent domestic inflation pressures. The Norges bank appear ready to move in September or November. However, the Iran/U.S. deal impact on energy prices could mean a downward inflation revision in September and mean no hike in 2026.

Figure 5: Norges Bank Policy Outlook Suggests Short-Lived Hikes

Source: June Norges Bank Monetary Policy Report

The Norges bank remain ready to undertake one final 25bps hike in September or November over concern on domestic inflation persistence. This was a hardening of the statement compared to previous meetings, which leaves the impression that the Norges currently want to hike. Even so, we think that the inflation persistence arguments, that actually prevented faster easing before the Middle East conflict broke out, are overdone and that even with no hike at all, the current Norges Bank policy stance is very restrictive. Even on its own assessment with the current policy rate is 1.5 ppt-plus above neutral despite (at worse) a mixed inflation backdrop.

Given the lags in such policy moves taking effect, this questions the need for such a temporary hike to 4.50% other than to underscore hawkish reputation. As a result, we feel the Board is being excessively hawkish.

Moreover, as suggested above, we question the extent to which the inflation forecast made by the Bank in the June report are realistic with the Board CPI-ATE now seen averaging 3.2% end 2026 and 2.6% end 2027, Some of the forecast this year is due to the apparent fact that CPI data have been higher than expected, but is this an indictment of the Board’s forecasting as despite its assertions to the contrary underlying inflation has been reasonably well behaved. Indeed, underlying inflation short-term dynamics are far from unfriendly especially if food is excluded from the targeted CPI-ATE measure so as make a more familiar core measure.

Given Norges Bank hawkishness, we remain far less confident about the extent of any eventual easing, and our forecast is deferred into 2027. A 2026 hike is possible to 4.50%, but a rethink could stop this. Additionally, we envisage some 100 bp of cuts through next year. At 3.25%-3.5%, that would still leave the policy rate still at the end if next year well above its own estimated nominal neutral rate of just over 2%.

Switzerland

The June quarterly assessment saw little shift in the forecasts for either growth or in target inflation (Figure 6), with the tone of the economic outlook remained guarded due to concerns over the Iran war on the global economy (forecasts though look to have been completed before the U.S. Iran deal). This will be enough to justify stable policy now and for some time. We still see policy remaining on hold until at least mid-2027, with only a slight possibility of a return to sub-zero rates given the high(er) bar seen by the SNB for this to occur.

Figure 6: SNB Inflation Outlook Little Changed

Source: SNB

The SNB noted that CPI has rotated higher with the increase in energy prices and this has marginally pushed the CPI projections higher. Even so, the forecasts appear to have been completed before last week’s U.S./Iran war interim agreement and the near-term multi quarter inflation outlook could be revised down in September. As we have previously noted though the Swiss Franc strength has played a part in keeping inflation under control, weak domestic price pressures is also a disinflation force. Additionally, with a still soft 2026 GDP growth of around 1%, the sports adjusted GDP growth this year may be below 1% and thus some 0.5% below potential. This helps restrains domestic prices.

For policy the guidance is for stable policy rates, with inflation projections consistent with target and domestic disinflation counterbalancing risks noted in the statement of a renewed surge in energy prices (probability of the latter is lower after the U.S./Iran deal).

The strong Franc, more recently against the USD, did not have major policy impact. While still pointing to possible FX intervention and a continued willingness to adjust policy accordingly, the SNB was keen to suggest its currency aspirations and actions are not designed to boost Swiss competitiveness. But this seems more talk than action as any overt attempt to weaken the current via intervention or lower/negative rates may be shunned by the SNB for fear it would court U.S criticism and possibly fresh tariff retaliation. A high bar also exists for any return to negative borrowing costs the SNB has been clear this is because of the adverse impact on savers and pension funds (SNB President Schlegel stressed this in a recent interview).