BOJ: QT still 5-6% of GDP until 2030 at least!

· Though the BOJ will maintain bond buying at Yen2trn pm from April 2027, huge redemptions means that net QT will be Yen45trn April 27-March 28 i.e. around 6.5% of GDP after QT at 6% of GDP in 2026. Then JGB net reduction of Yen40trn (6% of GDP) FY 29 and Yen35trn (5.5% of GDP). With a modest budget deficit, this is a huge amount of debt for the rest of the market to absorb. This will require higher real yields and a still larger term premium. It is difficult to see 10yr yields below 2.5% and we feel a spike through 3.0% is a real prospect in the next 3-12 months.

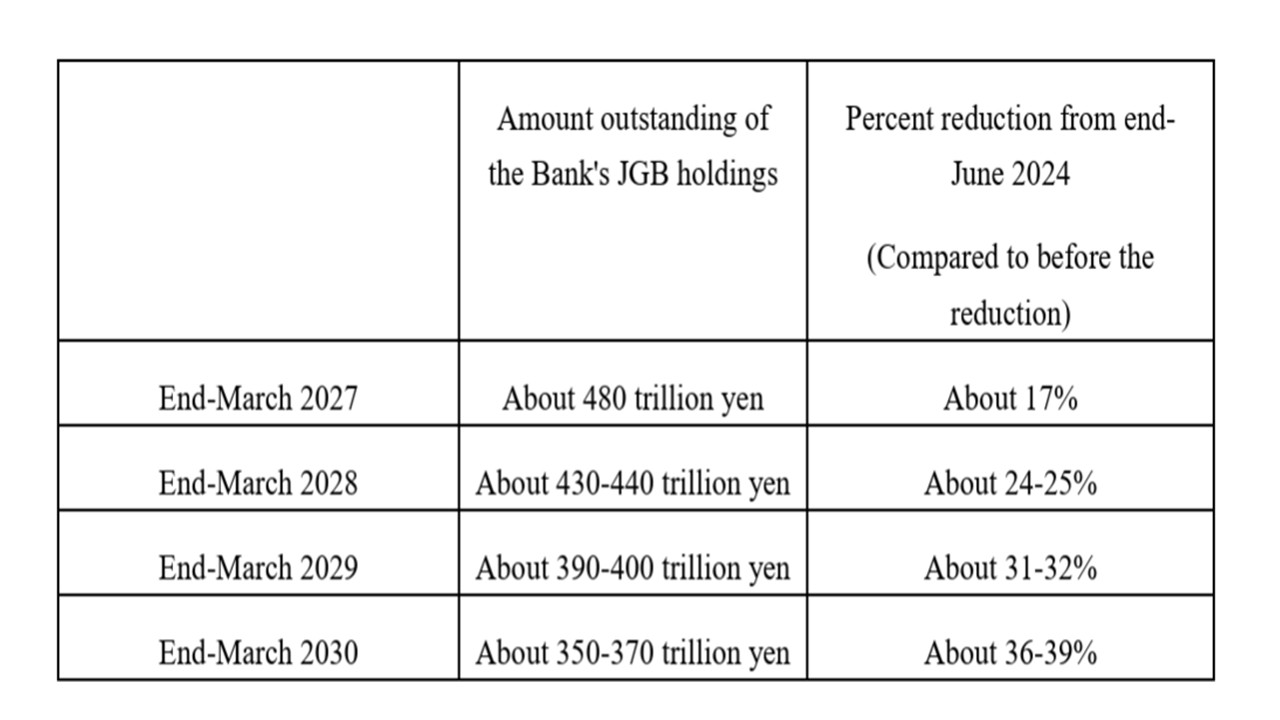

Figure 1: Projected Amounts of BOJ JGB Holdings (%)

Source: BOJ (here)

For 10yr yields, BOJ QT is more important than gradual BOJ policy rate normalization. Though the BOJ are keeping Y2trn pm gross bond buying, huge redemptions means that the BOJ is projecting its balance sheet to reduce materially by March 2030. The BOJ statement on QT (here) means that net QT is projected at 6.5% of GDP between April 2027-March 2028 (Figure 1), then 6% in the 12 months to March 2029! With a modest budget deficit, this is a huge amount of debt for the rest of the market to absorb. This will require higher real yields and a still larger term premium. It is difficult to see 10yr yields below 2.5% and we feel a spike through 3.0% is a real prospect in the next 3-12 months. This could bring a small U turn from the BOJ via an increase in gross bond purchases, but we suspect it will not be aggressive. Net QT should be down to 2-3% per annum to avoid QT produce a steepening yield curve in a tightening cycle.

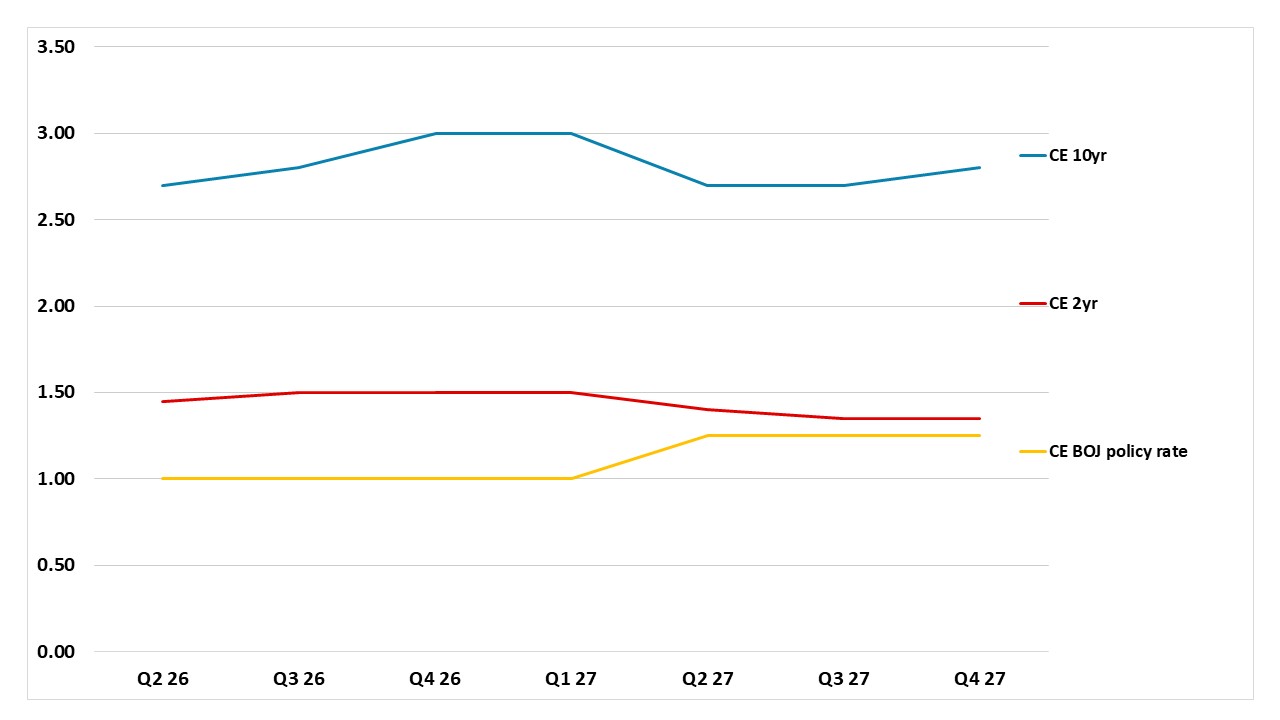

Figure 2: 10, 2yr JGB and BOJ Policy Rate Forecasts (%)

Source: Continuum Economics

In Japan, though the BOJ forward guidance is weak after the 25bps June hike to 1.00%, the multi-year normalization profile is still expected by the market. We see a 25bps hike in Q2 2027 to 1.25%, in the aftermath of a 2027 wage round that is likely to be consistent with 2% inflation. The BOJ neutral policy rate estimate of 1-2.5% means that expectations will linger of a 2028 hike all the way through 2027 and hence why we see a gently rising path for 2yr yields (Figure 8). However, we do not feel that the BOJ will speed up, as the U.S./Iran interim deal reduce 2027 inflation risks. We also feel Japanese consumers will be somewhat resistant to 2% inflation in the shops next year and this can slow consumption and then inflation. 10-2yr will thus steepen further in a policy hike cycle.