Eurozone: PMI Slump Shows Energy Surge Constraining Activity, Not Just Hitting Costs

Once again surprising on the downside flash Eurozone Composite PMI fell to 47.5 in May from 48.8 in April and below the 50.0 no-change mark for the second successive month. The latest reading thereby signalled a further and steeper m/m reduction in business activity, was the sharpest since October 2023. As S&P put it, the EZ economy is taking an increasingly severe toll from the war in the Middle East, with this survey data indicating that a GDP fall of 0.2% this quarter. At this juncture and noting that the PMI data do not cover vital areas such as government, retain and finance, that may be a little over the top. But it is in the right direction and suggests that the ECB faces a clear dilemma. After a GDP shortfall in Q1, its 0.1% Q2 estimates also looks rosy, while at 3.1%, its current quarter HICP estimate looks intact but without any sign of second-round effects that were seen as risks in its assumption.

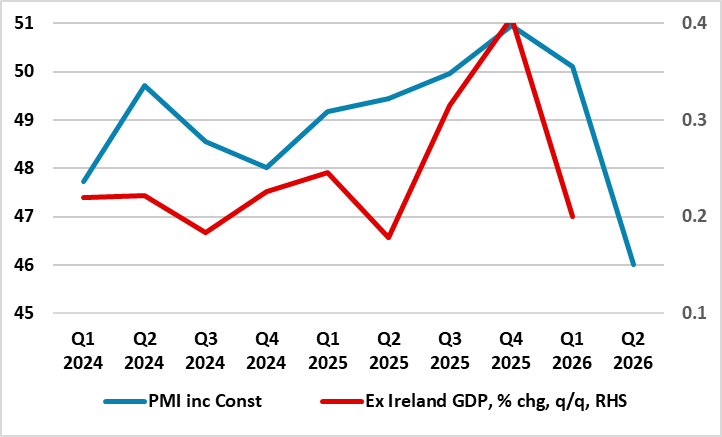

Figure 1: PMIs Show Downside Economy Risks

Source; Markit, Eurostat (ex-Ireland GDP measure is less volatile)

Otherwise, the data suggest also that job losses are also starting to become worryingly widespread as business confidence in any swift turnaround in the adverse economic climate fades further. Notably, the service sector is being hit especially hard by the cost surges created by the war. Moreover, the PMI data may still overstate manufacturing activity, confusing restricted supply as a demand positive signal, this being even more the case in the almost as weak, fresh fall into contraction territory in the UK May PMI. What is notable is that supply shortages not only pose upside risks to prices but can and seem to be constraining real activity already growth already and probably more so in the coming months but also have the potential to add further upward pressure to inflation.

Although not yet our official line of thinking, the ECB does seem to have its figure on the hiking trigger and will pull it without some positive news from Middle East conflict such as re-opening of the Straits of Hormuz. But if a hike occurs this is only going to add to real economy downside risks, both by damaging sentiment further, increasing costs and adding to what already signs of EZ banks wariness about lending, all suggesting rate hikes will not last.