EZ HICP Review: Absence Second-Round Effects Continues

Contrary to some thinking, EZ HICP inflation continues to behave, both absolutely and relatively – ie to what looks ever excessive ECB price thinking. The question must be if and when the ECB chooses to note friendlier price and costs signals, rather than pander to the upside prices risks that only some (and may be fewer) pieces of data have been flagging. Regardless, the ECB cannot disregard the June HICP flash (Wed), which dropped markedly and with no sign of second-round effects, thereby suggesting that headline inflation has not only already passed its peak and maybe clearly so but should fall further even in the near-term and widely so. These data may have a material impact on ECB thinking, especially as the data arrive toward the end of this week’s key ECB monetary annual gathering in Sintra.

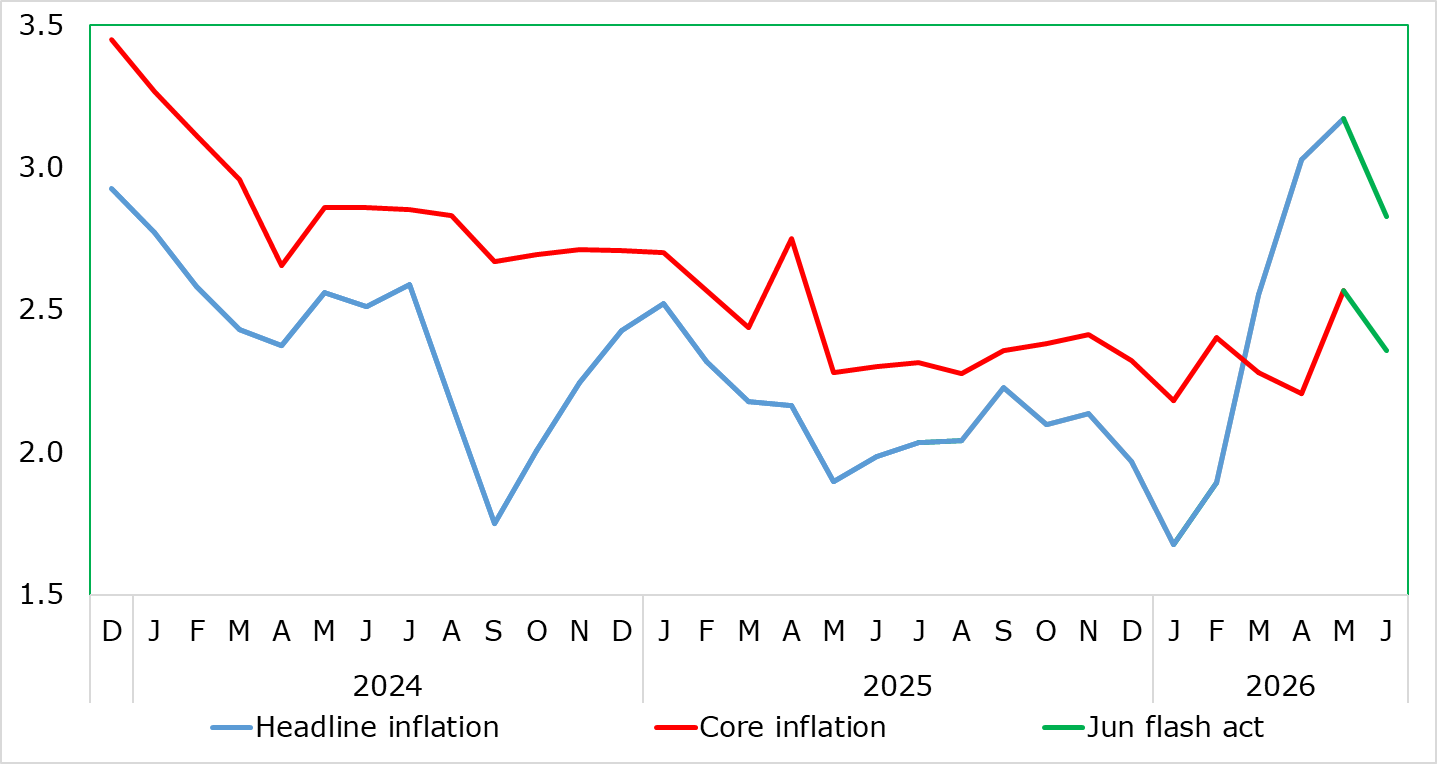

Figure 1: Headline HICP Plunges And Core Eases Modestly Too?

Source: Eurostat, CE

There are at least three price-friendly aspects to these June HICP flash numbers, which suggests the headline rate peaked at 3.2% in May and not the 3.4% rate implicit for June in the ECB quarterly projections released earlier last month. In fact, we see the headline down to as low as 2.5% this month pulled down not just by hefty energy price falls which largely failed to spill into the June numbers. Indeed, our below consensus June estimate of 2.7% (0.1 ppt below the actual) was based around a fall in energy cost of which only half came through, the rest (see Figure 2) seemingly baked in July’s cake to reduce inflation even more then. But a reminder of ECB lack of analysis, as unlike many, they were not overtly expecting an unwind to a seasonal aberration in travel prices last month that pushed up services inflation in May. This pulled services and the core down too (Figure 1).

But apart from seasonal quirks and energy weakness, the data continue to show no sign of global supply problems – the very opposite with core goods inflation still around 1% y/y, surely symptomatic of Chinese dumping, an issue so worrying Germany. All of which is backed up a second successive friendlier price and cost message from the latest PMI data, which did note further signs of inflationary pressures easing in June. Although input costs continued to rise rapidly during the month, the rate of inflation eased to the slowest since February, just before the outbreak of war in the Middle East. Weaker increases in input prices were seen across both the manufacturing and service sectors, with the pace of inflation remaining sharper in the former. In turn, the rate of output price inflation also slowed in June, albeit to a lesser extent than was seen for input costs. Here too, manufacturers continued to record stronger inflation than their services counterparts.

While tilted to the upside, which produces risks on both sides but those possibly precipitating second-round effects, we note the marked contrast in the labor market and consumer price expectations compared to the inflation surge that followed the invasion of Ukraine four years ago. Of course, and as surveys have highlighted, costs may be rising fast, but nowhere near as much as seen in 2022.

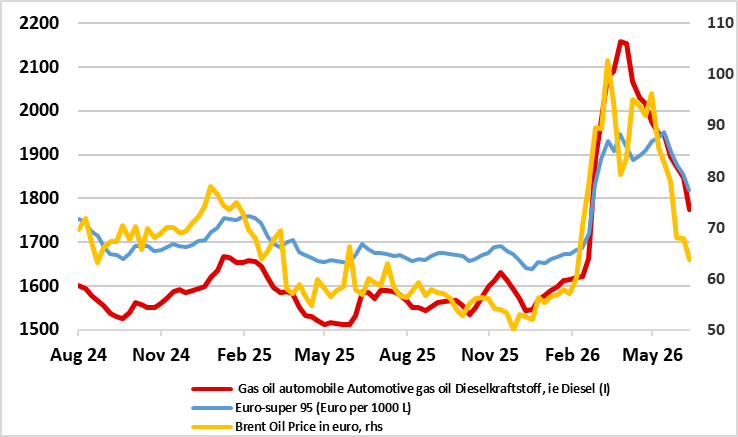

Figure 2: Retail Fuel Prices Plunging

Source: European Commission

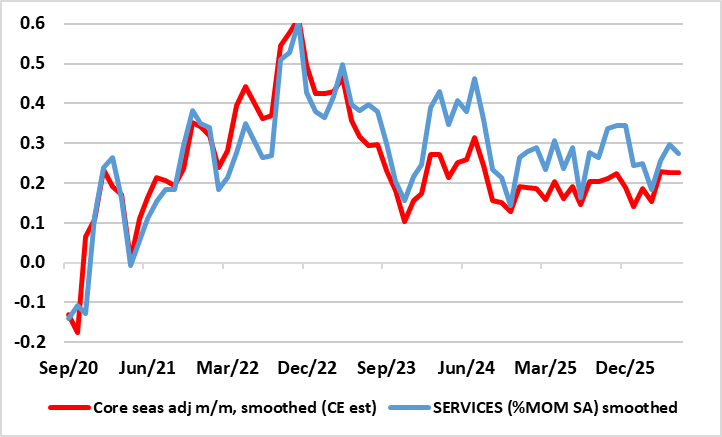

Regardless, and arguing against any clear wage spiral emergence, an ever-wider array of survey data suggest also that job losses are also starting to become worryingly widespread as business confidence in any swift turnaround in the adverse economic climate fades further. Notably, the service sector is being hit especially hard by the cost surges created by the war. Moreover, what is even more notable is that supply shortages not only pose upside risks to prices but can and seem to be constraining real activity already growth already and probably more so in the coming months but also have the potential to add further upward pressure to inflation. As a result, short-term adjusted HICP measures confirm no second-round effects well into the third month of post Middle East conflict strains (Figure 3).

Figure 3: Core HICP Messages Still Benign

Source: Eurostat, CE

In fact, we continue to see inflation averaging around current level for the rest of the (notwithstanding a possible dip to 2.5%) his month and then dropping back to 1.8% for 2027. This will be partly on account of the likely real economy damage from the conflict but also reflects our long-standing view that the ECB has been complacent, downplaying what we regard are downside real economy and monetary risks which may now be materialising and possibly more intensely given the manner in which financial conditions have tightened.