AI Labs IPO Fever

· Space X could get an initial good reception, but then go flat waiting for the Open AI and Anthropic IPO’s. Space X is an AI enterprise play rather than space and xAI is lagging. This could mean a modest correction in the U.S. equity market at some stage in the summer, but then the Anthropic IPO trigger new optimism. The key to watch is reports of AI labs revenue growth. If this remains strong it not only keep the AI labs buoyant, but also semiconductor and cloud computing sectors in tech as well.

· In terms of the S&P500, we remain less concerned about high valuation in the tech sector provided AI labs growth remains fast. 12mth fwd information technology are mid-range in the 2020-26 experience rather than at the highs. The problem is more non tech in terms of either a cyclical slowdown in consumption due to lower real income growth or a structural scare of AI replacing some U.S. employment permanently. The S&P500 could run up to 7800 in 2026, with small intermittent corrections and we have lifted our end year target from 7200, but not the vulnerability in the non tech sector.

3 Big IPO’s (Space X June 12; Open AI and Anthropic Q4 2026) are prompting how it will impact the U.S. equity market.

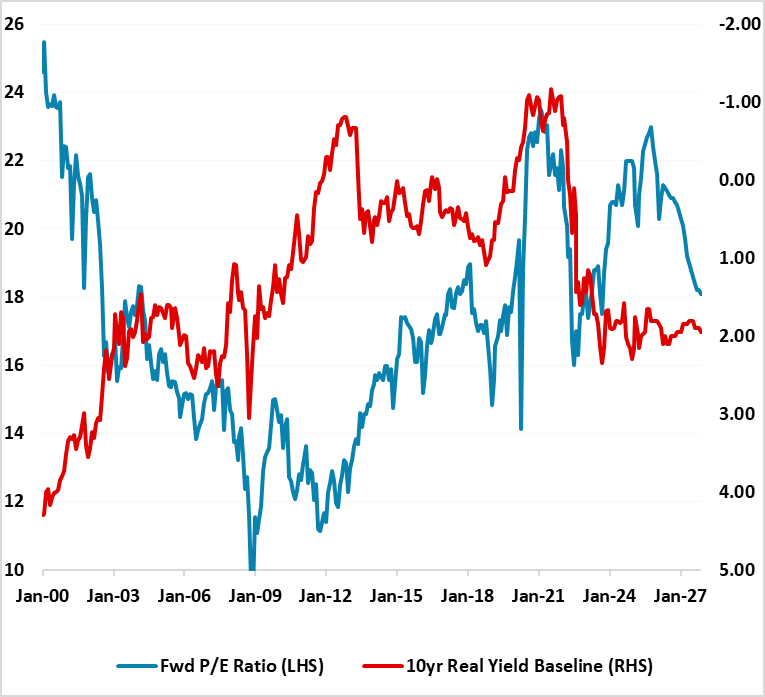

Figure 1: 12mth Fwd S&P500 P/E Ratio and 10yr Real U.S. Treasury Yield Inverted Until end 2027 (Ratio and %)

Source: Continuum Economics with forecasts to end 2027 for 10yr real bond yields and fwd P/E ratio.

The technology sector has led the U.S. equity market higher from the Iran war lows, both as tech valuations had moved towards the bottom of recent experience and corporate earnings remain buoyant. This has left the information technology sector back in the middle of the 2020-26 range, but off the 2025 highs and prompted the question of how the Space X/Open AI and Anthropic IPO’s will be received. Revenue for AI labs such as Anthropic and Open AI is booming, with Anthropic run rate reported to be up 500% since the start of the year. This exponential revenue growth allows analysts to deploy growth models that look out to 2030 to produce revenue and EBITA figures that can back the valuations for the three IPO’s. Additionally, all three will be big tech stocks and will attract index funds that could quickly absorb the equity being raised in the IPO’s.

The three are different however. Anthropic has the best story having leapfrogged Open AI and seen to be the leader in business enterprise AI. This track record should mean a keen demand across the tech sector at high price/current revenue rates. Open AI has supporters and critics. Leadership in the consumer sector/large secured AI datacentres capacity to make the next leap forward/2nd place in the enterprise market. Both benefit from U.S. restrictions on China in acquiring the new generation of Nvidia Blackwell and Rubin chips. However, after a USD180bln of funding raising, Open AI still need more funding to pay for huge semiconductor orders and cloud computing commitments, which could be testing if Open AI revenue growth slows.

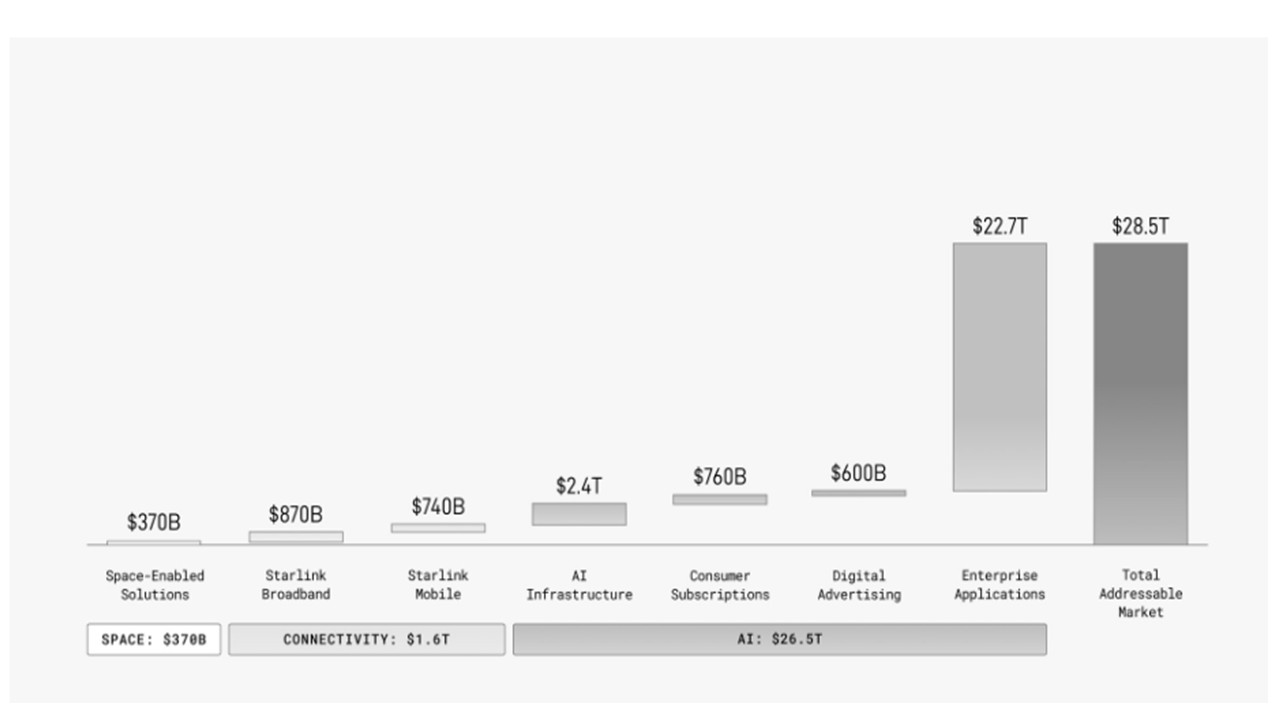

Space X is also mainly an AI trade looking at SEC filing in terms of Total Addressable Market into the 2030’s (Figure 2). Space is a moderate marketplace, while Starlink is overshadowed by a huge AI opportunity – most scientists argue that cost effective space datacentres are well into the 2030’s and highly uncertain. Musk success with Tesla helps initial optimism. The problem is that Space X xAI is lagging other AI labs. Some investors also do not like the two tier share structure that favours Elon Musk heavily. This looks the most speculative and with long-term risks behind the story.

Figure 2: Total Addressable Market for Space X (%)

Source: Space X S1 Filing

Space X could get an initial good reception, but then go flat waiting for the Open AI and Anthropic IPO’s. This could mean a modest correction in the U.S. equity market at some stage in the summer, but then the Anthropic IPO triggers new optimism. The key to watch is reports of AI labs revenue growth. If this remain strong it not only keeps the AI labs buoyant, but also semiconductor and cloud computing sector in tech as well. However, the AI story can cause further disruption in the software sector, which means that not all tech are winners.

In terms of the overall U.S. equity market, the outlook for the non tech sector is also important. Corporate earnings have been better than we thought in 2026, which can always sustain short-term optimism. However, hopes of Fed rate cuts will likely be difficult to be realised in 2026. Though Warsh argues that productivity is high currently due to AI and will lead to disinflation, many FOMC members argue that the AI buildout could first boost inflation. Focus will be on the June 17 FOMC meeting where it is likely that the easing bias will be dropped, but Warsh Q/A will still provide hints that developments could still allow easing into 2027. The key problem for the non tech sector is if corporate earnings growth slows, with the biggest risk remaining that the overstretched low and middle income households could slow consumption growth (here). The latest GDP breakdown shows that income growth has been revised down and mean a still lower household savings ratio (here).

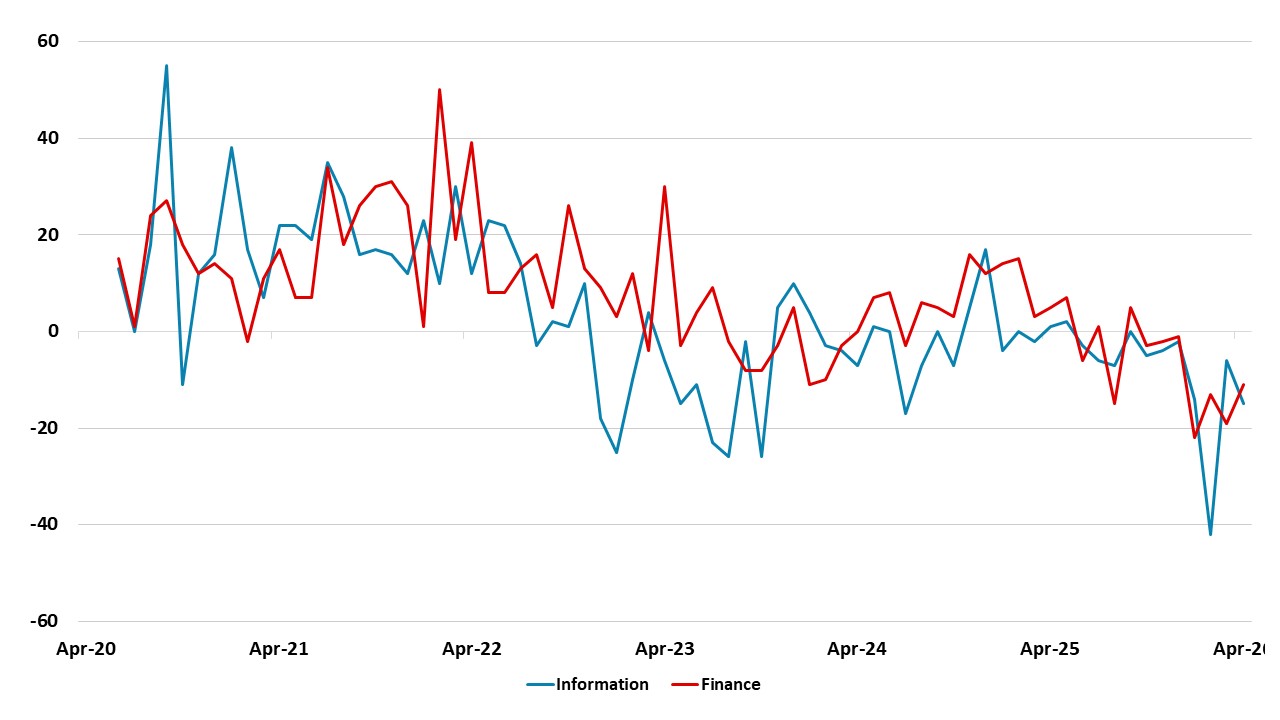

The other issue for the U.S. non tech sector is whether structurally AI means net job losses that hurt income then consumption and GDP. The trend in information technology and finance sectors shows that monthly net jobs have turned negative (Figure 3). This could be further deployment of AI and companies anticipating that it will mean leaner workforces. This is a theme to watch at the moment, as AI is being rolled out most aggressively in these sectors and these patterns may not be repeated elsewhere (they are around 8% of non-farm employment). AI Humanoid robots are also limited by hardware rather than software, including high cost/limited battery life and lack of full movement in line with a human hand. Most experts view humanoid robots as a 2030 story not the 2020’s. This means blue collar jobs are more secure. However, if fear of AI displacing human jobs grows, then it could prompt slow consumption growth.

Figure 3: Change in Employment for Information Technology and Finance Sector (monthly change K)

Source: Datastream/Continuum Economics

In terms of the S&P500, we remain less concerned about high valuation in the tech sector provided AI labs growth remains fast. 12mth fwd information technology are mid-range in the 2020-26 experience rather than at the highs. The problem is more non tech in terms of either a cyclical slowdown in consumption due to lower real income growth or a structural scare of AI replacing some U.S. employment permanently. The S&P500 could run up to 7800 in 2026, with small intermittent corrections and we have lifted our end year target from 7200, but note the vulnerability in the non tech sector.