U.S. Personal Income and Spending, Durable Goods Orders, GDP and Initial Claims - Consumers look vulnerable

The latest US data can be seen as on balance softer than expected, with a falling savings ratio in April suggesting downside risks to consumers, with consumer spending with inventories bringing a downward revision to Q1 GDP. Core PCE prices were softer than expected in April but revised up in Q1. April durable goods orders were mostly strong, but initial claims have moved up from recent lows.

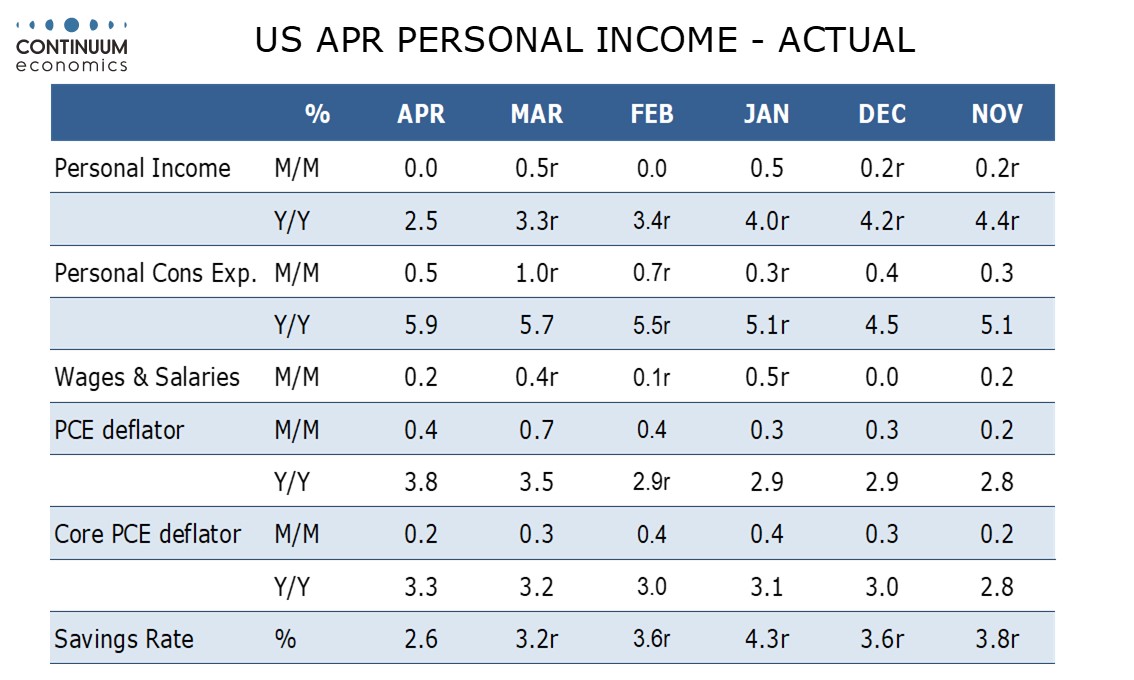

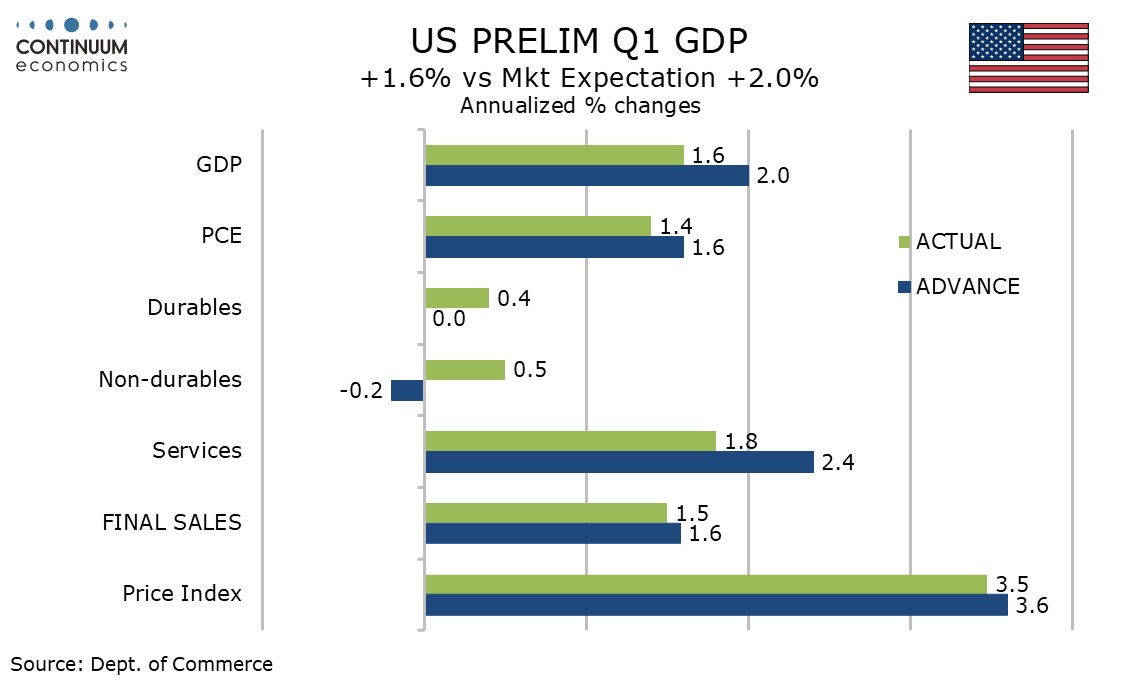

April personal income was unchanged with real disposable income down by 0.5%, significantly underperforming consumer spending which rose by 0.5% in nominal and 0.1% in real terms. Both income and spending were revised lower in Q1, real spending to 1.4% annualized from 1.6% and real disposable income to 0.7% from 1.1%, with Q4 revised to 1.0% from 1.3%.

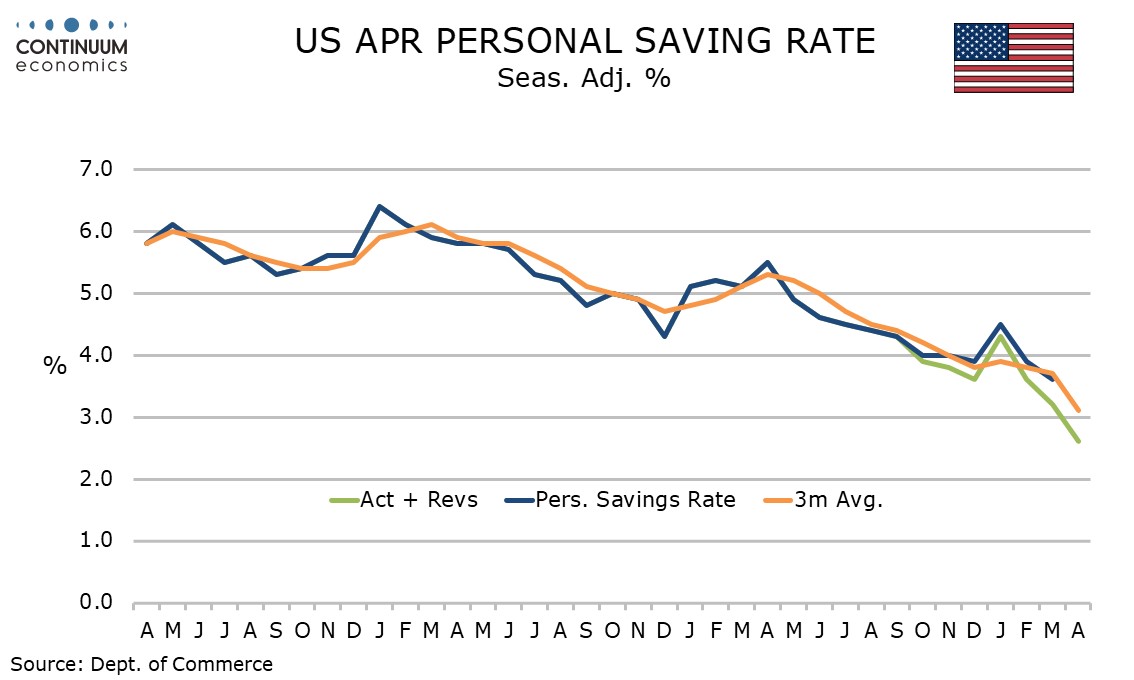

April’s savings rate of 2.6% in the lowest since June 2022 and down from 3.2% in March and 4.3% in January. Tax cuts gave some support to real disposable income in January but not in April when tax payments are heaviest, suggesting that consumers have dipped into savings to sustain spending as energy prices surge. If high energy prices persist, consumers may be forced to cut back.

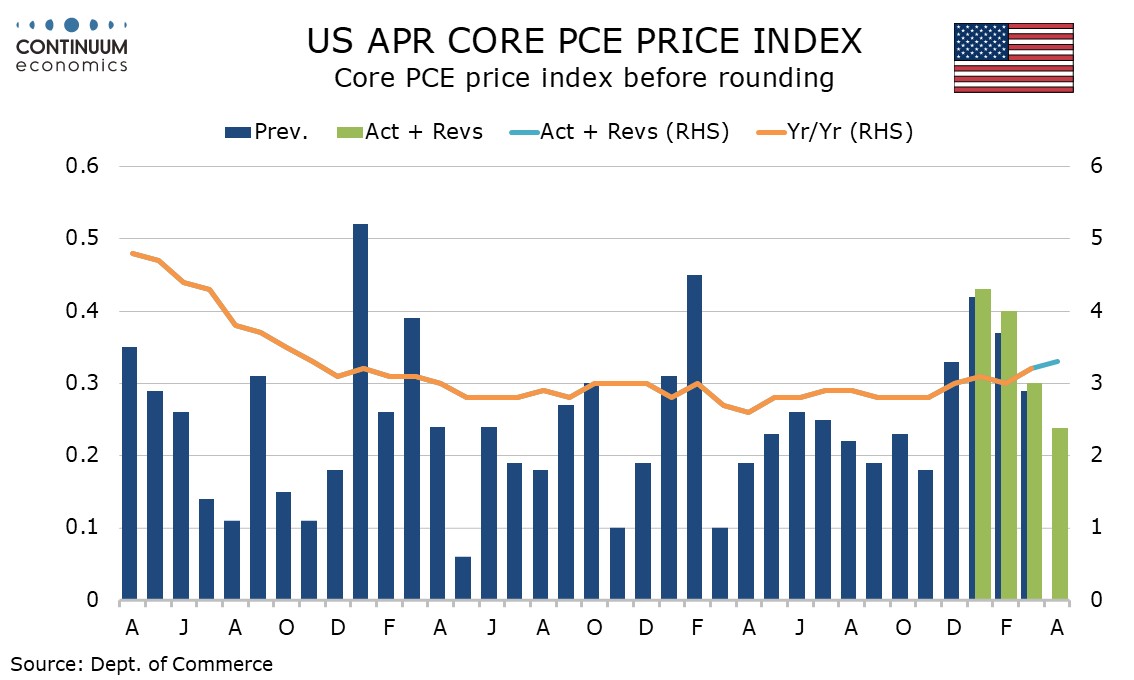

April core PCE prices at 0.239% before rounding were lower than expected and confirm that April’s 0.4% core CPI was inflated by a one-time distortion in housing, with items measured on a 6-monthly basis seeing a catch up from a lack of measurement on October due to the government shutdown. However with each month of Q1 seeing marginal upward revisions (noticeable only before rounding) the yr/yr rate of 3.3% was on expectations, and the highest since November 2023.

Overall PCE prices rose by 0.4% on the month with yr/yr growth at 3.8%, from 3.5% in March and the highest since May 2023. Q1 PCE prices were revised up to 4.4% annualized from 4.3% but overall PCE prices were unrevised at 4.5%. The GDP price index was revised down to 3.5% from 3.6%.

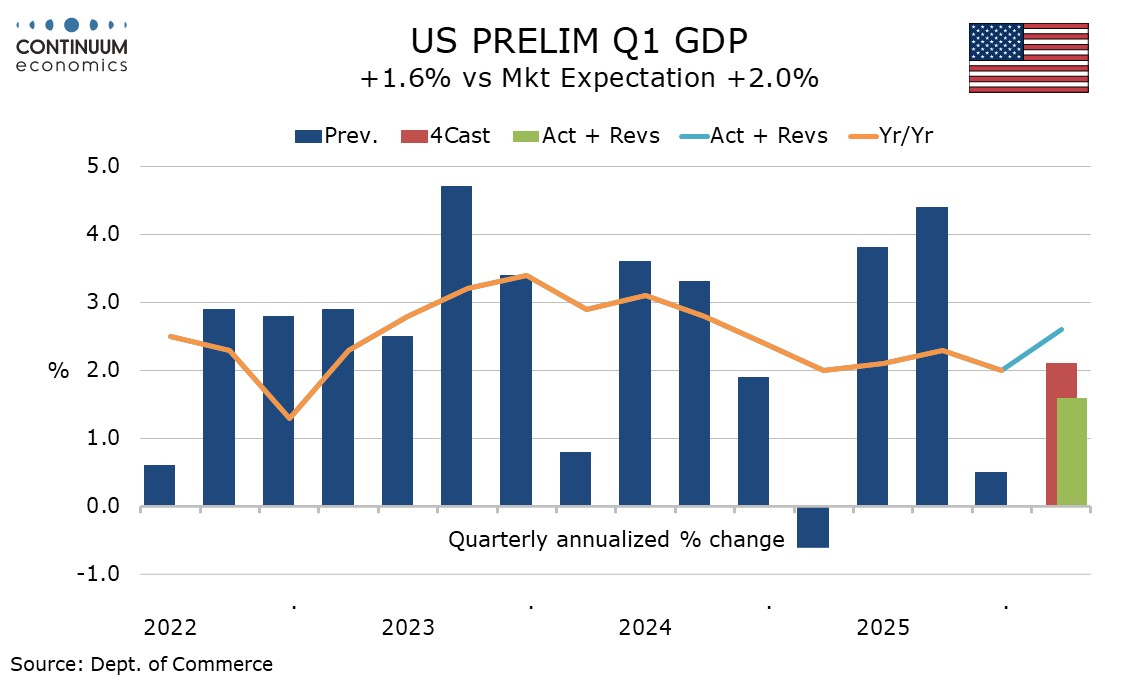

The downward revision to Q1 consumer spending as more than fully explained by services with retail sales revised higher. The downward revision to services was one of two significant negatives in a downward Q1 GDP revision, to 1.6% from 2.0%. The other, and largest, was inventories. Final sales (GDP less inventories) were revised only marginally lower to 1.5% from 1.6%. Final sales to domestic buyers (GDP less inventories and net exports) saw a similar revision, to 2.7% from 2.8%.

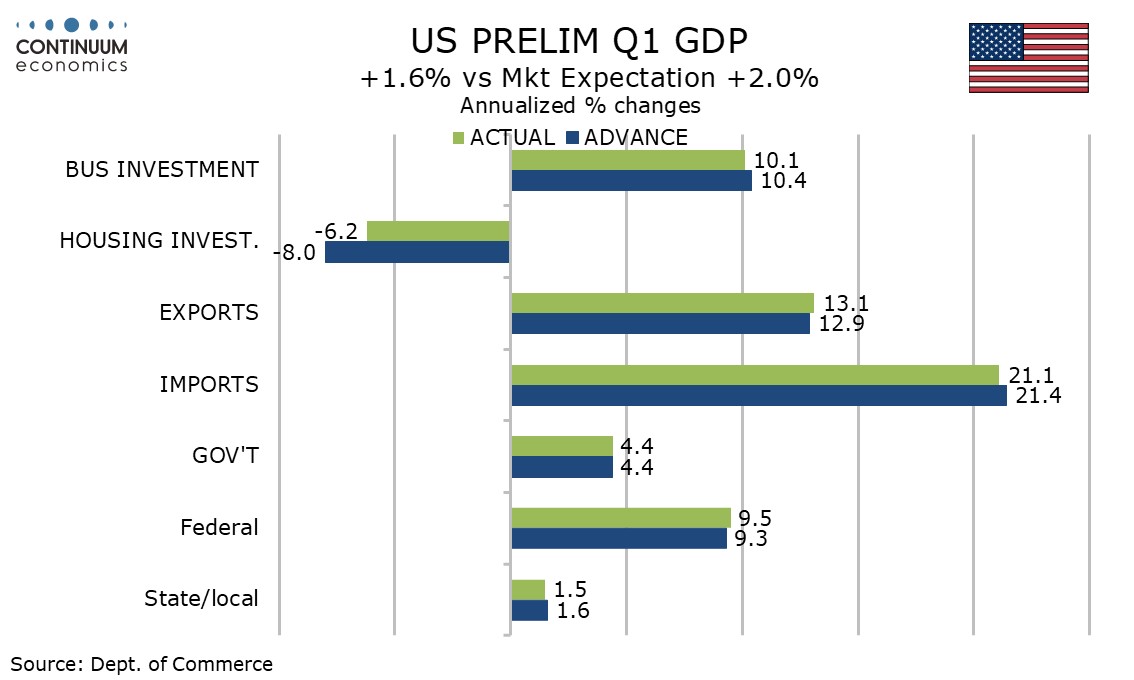

Elsewhere in the GDP revision business investment was revised marginally lower on intellectual property, but more than offset by a revision that made housing less negative. Government saw Federal revised marginally higher but State and Local marginally lower. Net exports were revised slightly higher with exports revised up and imports revised down.

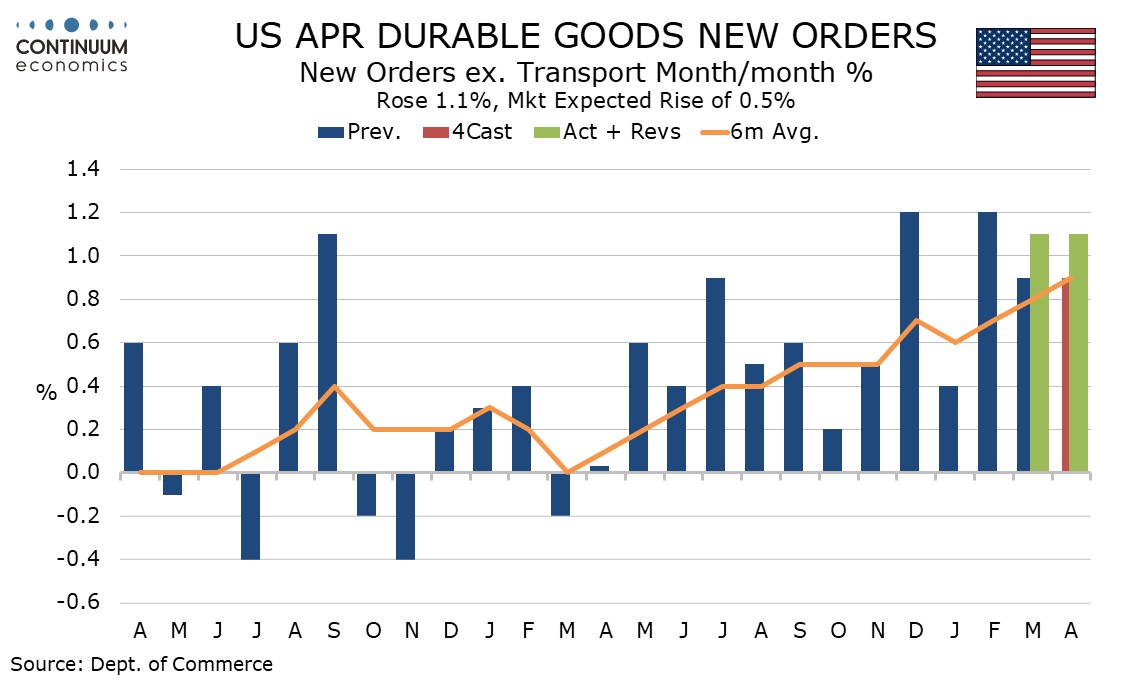

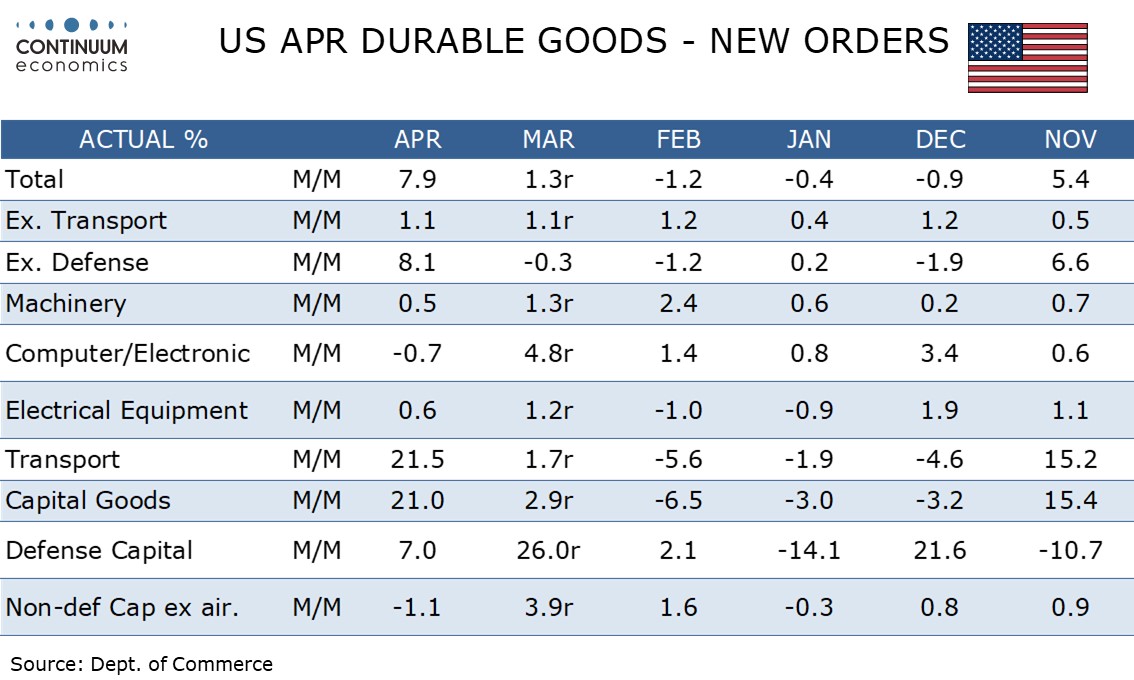

While the consumer still looks vulnerable the business investment picture remains healthy, with durable goods orders positive in April. The overall increase of 7.9% was led by transport, specifically the volatile civil aircraft, though the ex transport gain of 1.1% was the third straight rise of similar magnitude. This represents an acceleration in trend though acceleration in prices pay be playing a part.

Defense capital saw a second straight rise but orders ex defense outperformed the headline with a rise of 8.1%. Non-defense capital orders ex aircraft, a key indicator of business investment, fell by 1.1%, but this needs to be seen alongside an exceptional 3.9% rise in March. Shipments in the sector rose by a modest 0.4%, after two straight gains of 1.3%, hinting Q2 will be slower but not weak.

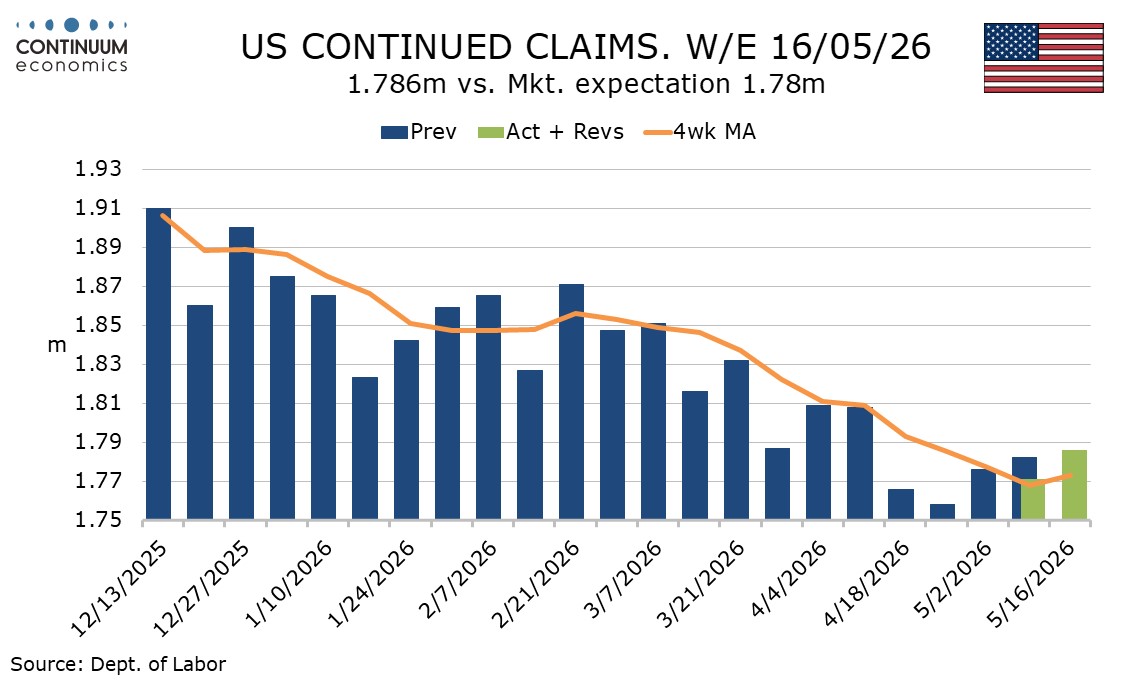

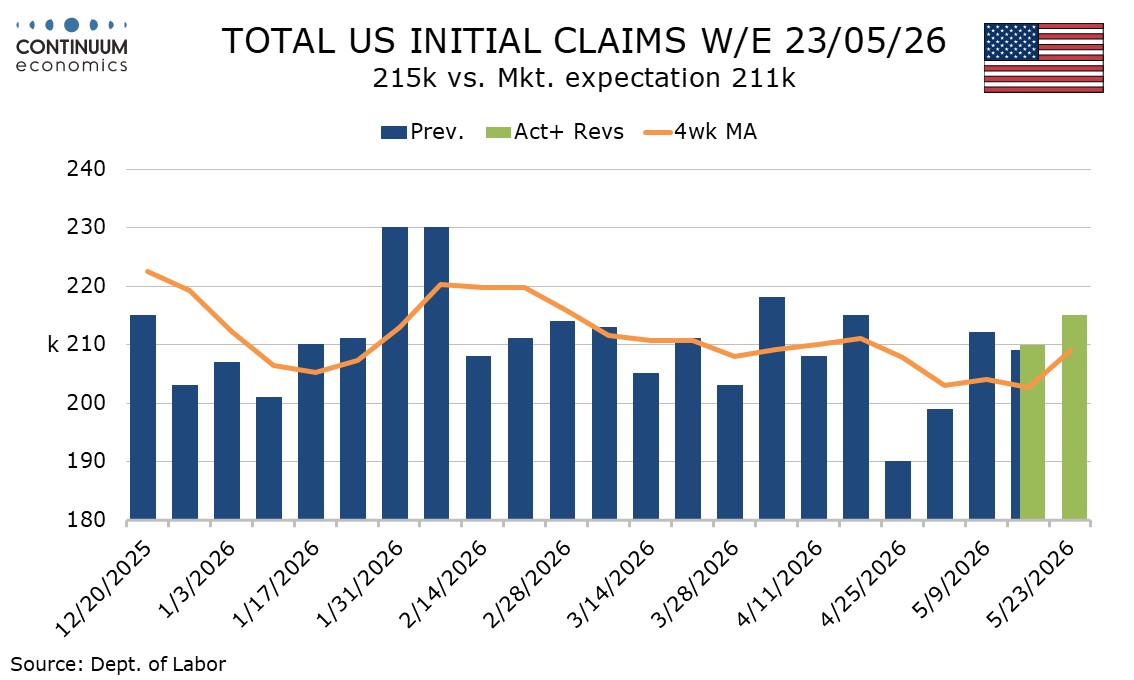

Weekly initial claims at 215k are at a 5-week high and trend appears to have returned to where it was before two straight outcomes below 200k seen three and four weeks ago. The latest data covers the week after the May non-farm payroll was surveyed.

The latest continued claims data covers the payroll survey week. This series also saw a modest rise, by 15k to 1.786k. The labor market still looks healthy but there may be some loss of momentum starting in mid-May. This does not imply weakness in May’s payroll but there may be risk of a more significant slowing in the coming months if consumers remain constrained by elevated energy prices.