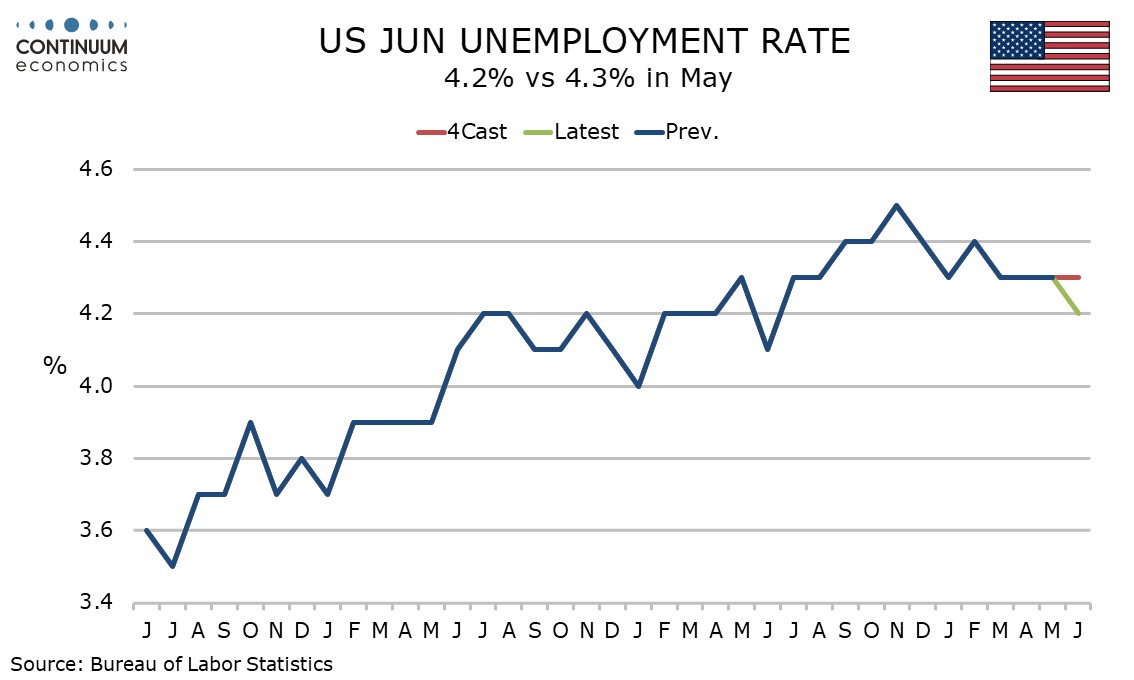

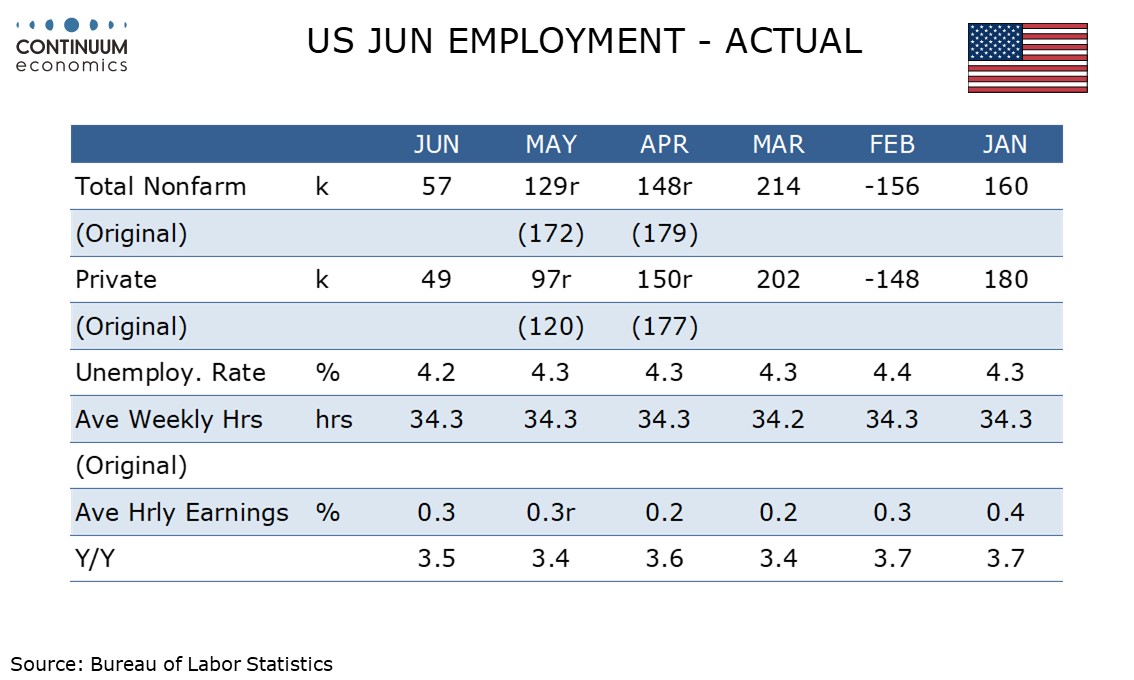

U.S. June Employment - Upside May surprise offset, but unemployment falls on lower labor force

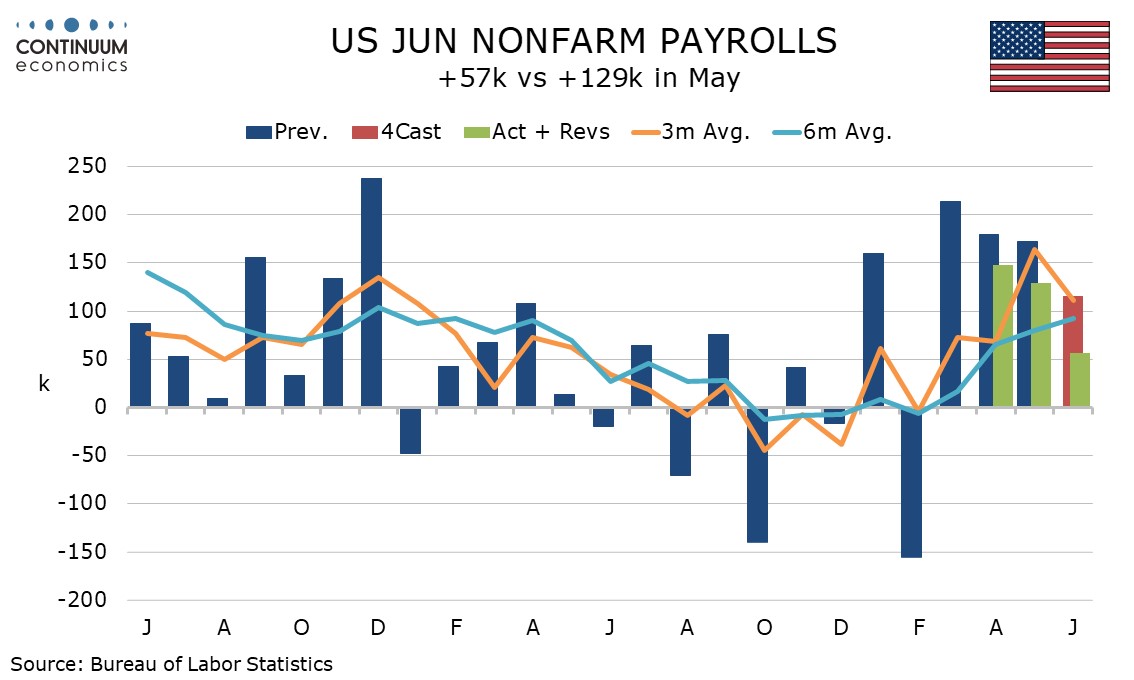

June’s non-farm payroll is weaker than expected with a 57k increase, 49k private, with downward revisions to April and May. The slowing is consistent with an upturn in the initial and continued claims trends, though both were almost unchanged (-1k to 215k and +2k to 1.814m respectively) in the latest weekly release. Unemployment did slip to 4.2% from 3.3%, but this was on a fall in the labor force. Average hourly earnings were in line with expectations, up by 0.3%.

May’s payroll was revised lower to 129k from 172k with April revised to 148k from 179k, a net downward revision of 74k making the overall net figure negative. For private payrolls the net downward revision was 50k, just enough to leave a marginal net negative.

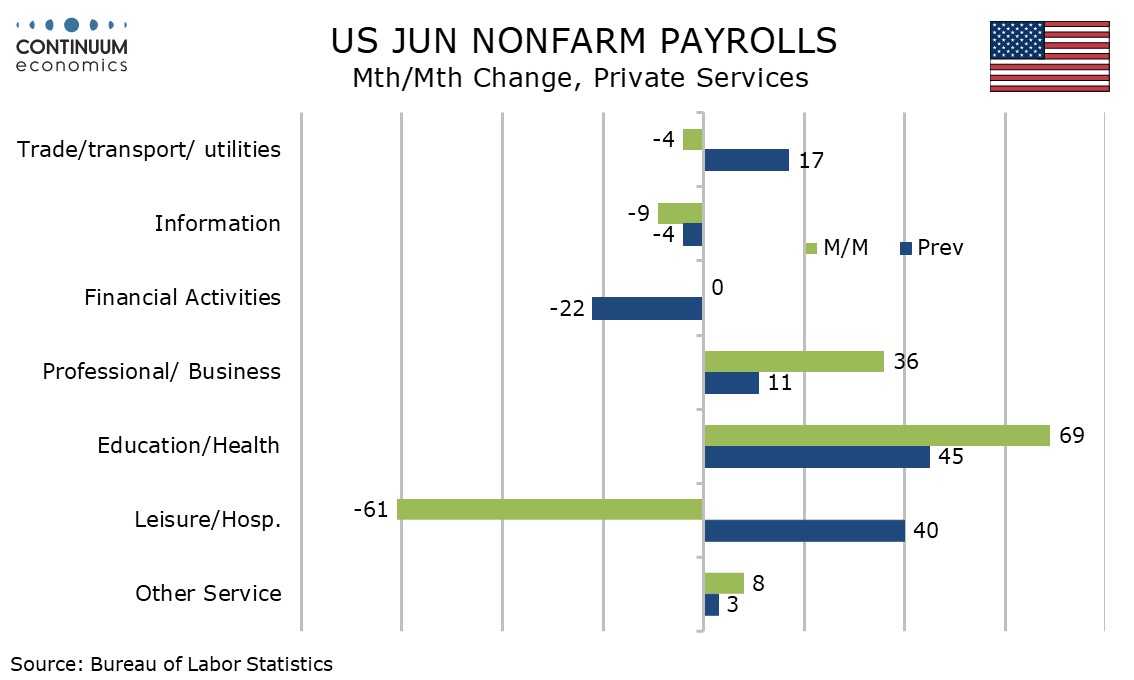

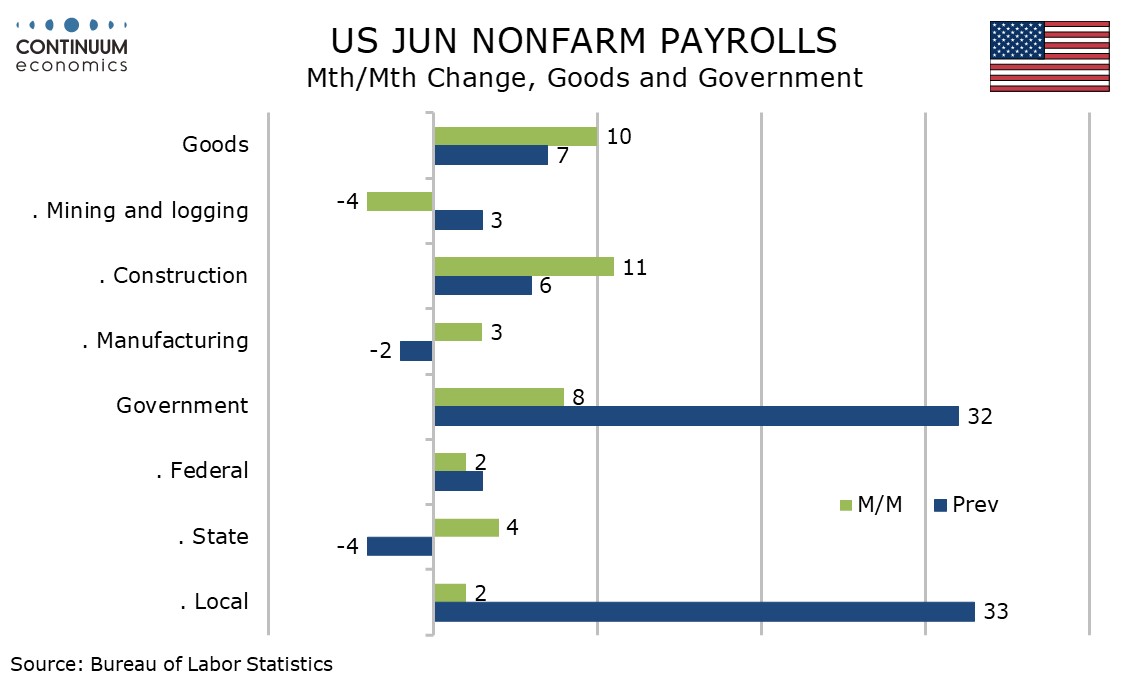

Two of the components that were surprisingly strong in May, leisure and hospitality and government, were revised lower, and leisure and hospitality actually fell in June by 61k, more that reversing a revised 40k increase in May, suggesting the World Cup is not providing the boost that May data hinted at. Government saw a modest 8k increase after a revised rise of 32k in May.

Education and health remains the strongest sector, up by 69k after a 45k rise in May that is now above the revised leisure and hospitality gain. Professional and business was above trend with a rise of 36k with 9k of that in temporary help, which could be World Cup related. Most components of the breakdown were subdued. Manufacturing at 3k and construction at 11k managed modest gains but retail fell by 7.5k.

The household survey, which calculates the unemployment rate, does not look impressive despite a fall in the rate to a 12-month low of 4.2% after three months at 4.3%. Detail shows a 720k fall in the labor force exceeding a 507k fall in the survey’s employment estimate.

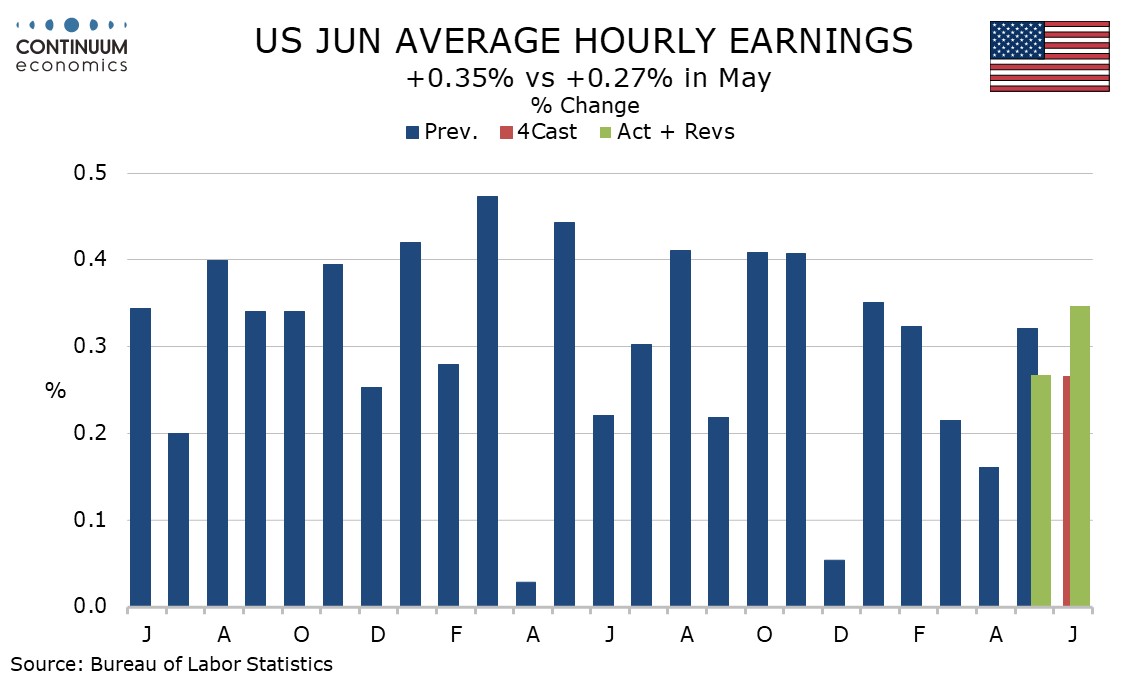

Average hourly earnings rose by 0.347% before rounding, but a marginal upside surprise before rounding is offset by May being revised down to 0.267% from 0.321%. Yr/yr growth of 3.5% from 3.4% is still consistent with a trend marginally below 0.3% per month.

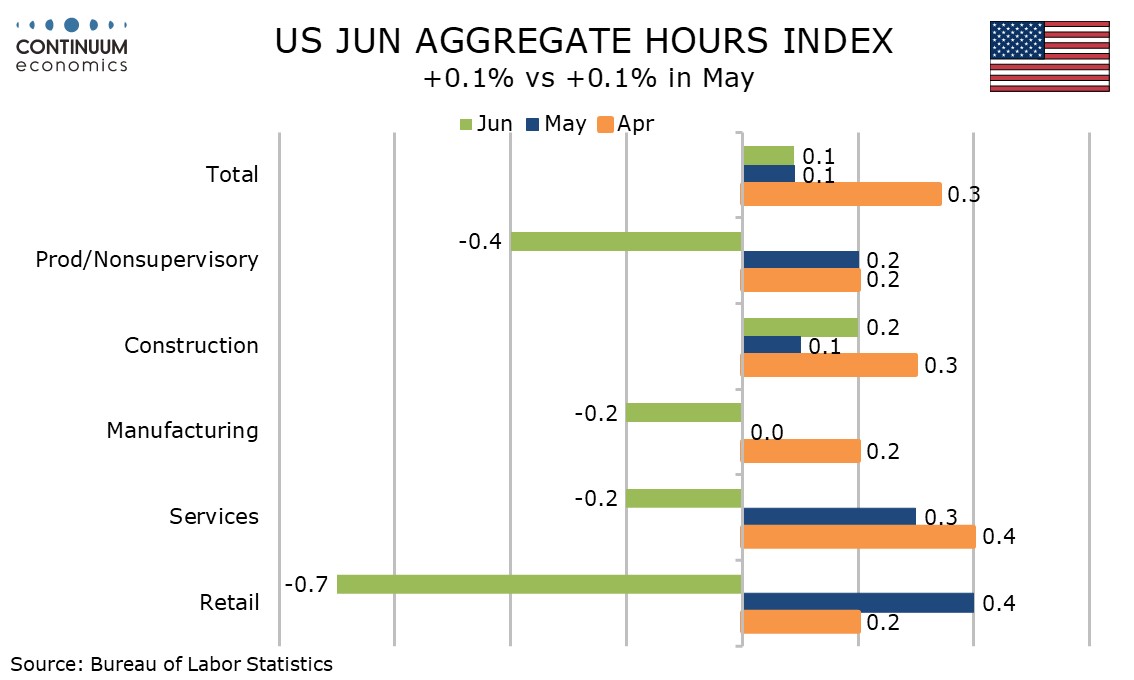

An unchanged workweek of 34.3 hours left aggregate hours worked up by 0.1% on the month, and 1.3% annualized in Q2. The quarterly gain is consistent with healthy GDP growth if productivity gains are assumed, but a wider May trade deficit suggests productivity may not lift GDP above aggregate hours in the quarter.

Construction saw a modest rise in aggregate hours worked, but manufacturing and services slipped, with retail particularly weak.

The data probably dies not make a major difference to the Fed. Doves will argue there is risk of the slowdown extending further, but peaking of energy prices reduces the downside risk. Hawks can point to the low unemployment rate, though tightening is likely to require an upside inflation shock. Fed speakers can continue describing the labor market picture as stable.