EZ HICP Preview (Jun 2): Headline To Surge Again as Core Starts To Rise?

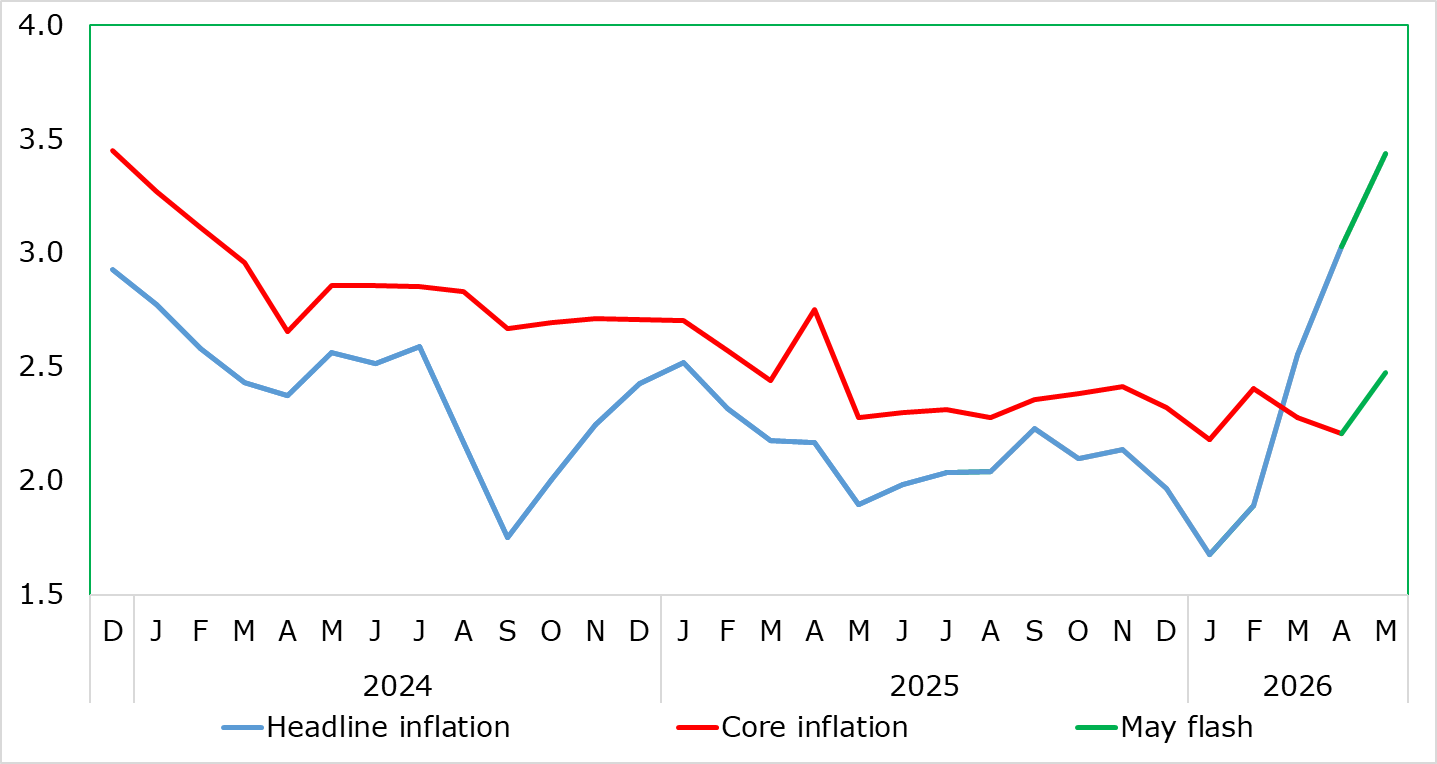

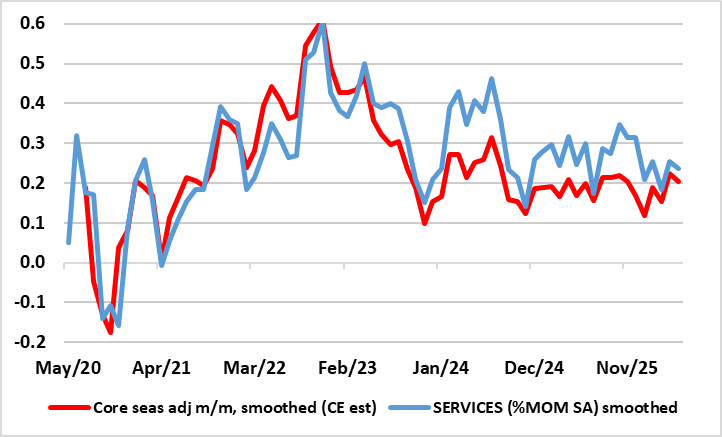

While somewhat important, the May flash HICP data is unlikely to have a material impact on ECB thinking, irrespective of whichever way it may surprise. Most likely the data will show a further and still largely energy driven rise of 0.4 ppt, matching the April gain, but now to a 32-mth high of 3.4%. This could involve small rise in the core too, albeit mainly aberrant seasonals pulling up services, but where the resultant core of 2.4% (0.2 ppt up) would mean a double-whammy in that both it and the headline would be above existing (ie March) projections. But the ECB (via Chief Economist Lane) has already noted that those projections are out date whilst also highlighting various statistical methods to suggest that energy-induced price pressures are already starting to broaden out (Figure 2), albeit something we do not see being backed up by actual data, most notably short-term adjusted HICP figures (Figure 3).

Figure 1: Headline Sharply Higher Again And Core Up Too?

Source: Eurostat, CE

As for actual recent HICP inflation, it rose broadly as expected in the April numbers, up 0.4 ppt to a 33-mth high of 3.0% but what was not expected was the drop in the core rate, down notch to a 3-mth low of 2.2% on the back of what the weakness services reading (3.0%) in over four years. To what degree this reflects the timing of Easter is unclear at this juncture, but it does not seem to have found much of a welcome in ECB thinking.

But given what are we are still unresolved evens in Middle East, we now see the peak in HICP inflation at around 3.5% though this and the next quarter. We accept risks not least stemming from our assumption of the Iran conflict, with perhaps the extent and form of any end to hostilities being the key conundrum. While tilted to the upside, this produces risks on both sides but those possibly precipitating second-round effects, we note the marked contrast in the labor market and consumer perceptions compared to the inflation surge that followed the invasion of Ukraine four years ago.

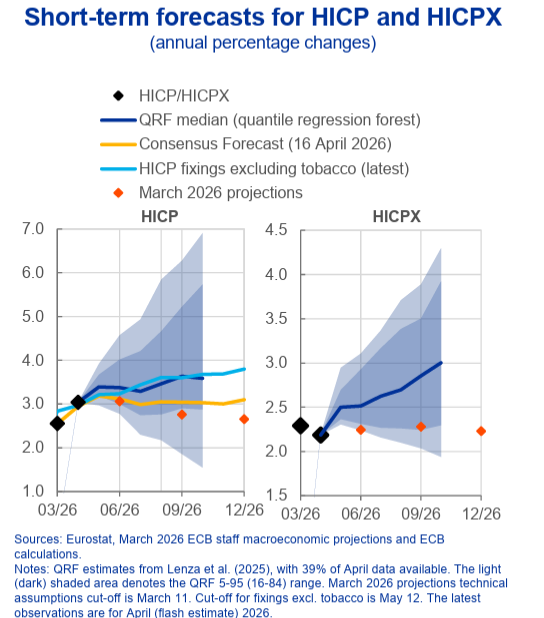

Figure 2: ECB Projections See Higher Core Getting Embedded

Regardless, and arguing against any clear wage spiral emergence, an ever-wider array of survey data suggest also that job losses are also starting to become worryingly widespread as business confidence in any swift turnaround in the adverse economic climate fades further. Notably, the service sector is being hit especially hard by the cost surges created by the war. Moreover, what is even more notable is that supply shortages not only pose upside risks to prices but can and seem to be constraining real activity already growth already and probably more so in the coming months but also have the potential to add further upward pressure to inflation. With this in mind, how the ECB revises it real economy outlook next month will be as important as how inflation is altered, the former very much helping determine both the size and persistence of any prove shock – one that does seem to be increasingly supply related.

But the ECB is seeing a clear and wider price shock. It is using so-called Quantile Regression Forests (QRF), an advanced machine learning and AI tool integrated into the ECB’s forecasting toolkit. It is used to generate real-time, short-term inflation projections and to "nowcast" GDP growth and its latest result are seen in Figure 2 which suggest a core rate rising to 3% before year end, almost a full ppt above that projected in March. Even so, actual HICP data are still showing no such signs, but the ECB is more mindful of its credibility and it does look almost nailed on for at least one hike in June, the question being if another will follow soon after!

Figure 3: Actual Core HICP Messages Still Benign

Source: Eurostat, CE