ECB Review: If Not Insurance, Why the Hike?

The 25 bp official rate hike unveiled today was so well-flagged it is hard to suggest that it is consistent with a decision process on a meeting-by-meeting basis. Similarly, the dominance of inflation upside risks, alongside another dose of optimistic real economy projections, is hardly proper data-dependency. All of which shows where the ECB focus lies (a sharp contrast perhaps to the BoE). But while the projections show HICP inflation back in line with target by Q4 next year, this though largely validates the market view of around three 25 bp hikes that the outlook is based on. But the projections show hardly any further damage to the GDP picture, with the ECB understating the combination of tight(er) financial conditions, banking sector reservations and ill sentiment that should combine to pull HICP inflation back to, if not below, 2% by mid-2027 and thus create both rationale and room for fresh policy easing. While a further hike cannot be ruled out given the ECB’s biased reaction function, we think that this 25 bp hike is more than enough and that this misplaced move will be more than reversed into 2027 (ie thinking largely siding with the OECD).

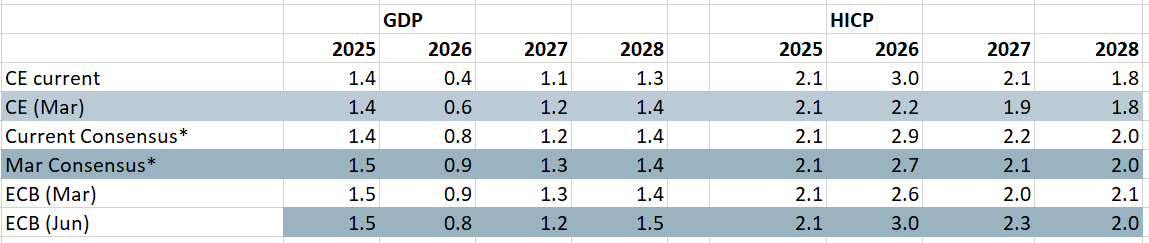

Figure 1: Economic Outlook from Various Perspectives

Source: CE, ECB, Consensus Economics

We still think the ECB is and will remain too pessimistic about inflation and too optimistic about growth (Figure 1). Despite what have been clearly weak business survey data and weak growth numbers, the cumulative downgrade to the GDP outlook over three years is a bare 0.1 ppt. Given the GDP downgrades unearthed last week (ie, well after the May 20 cut-off date for the new projections) the ECB is assuming 2% annual rate growth per quarter for the rest of the year. Admittedly, this downgrade is refection of anomalies in Irish national accounts without which EZ GDP would have growth nearer 0.4 q/q of late. But when the ex-Ireland GDP numbers were labouring over a year ago, the ECB was happy to take the headline numbers at face value. Indeed, it is notable how little the GDP outlook varies among the (now) four scenarios the ECB is offering, with the ECB suggesting all are consistent with the need for at least this hike. Admittedly, these forecasts made ready by late May explain the chorus of comments flagging this hike even if that is not really consistent with the ECB so-called meeting by meeting approach.

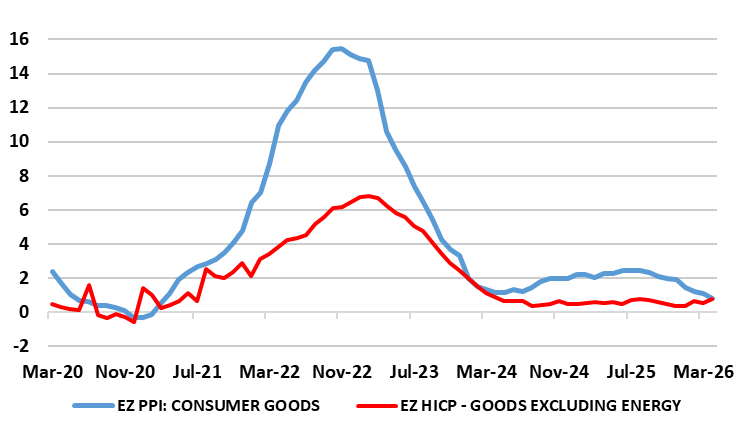

But the ECB’s data dependency is also in question, not least by ignoring the weak GDP and survey backdrop alluded to above, but also focusing on indicators pointing almost purely to upside HICP risks possibly having materialized already. As Figure 2 shows, this is far from the case as consumer goods PPI data (up to April) has reached new lows at under 1% y/y, and suggest little sign that HICP core goods has stayed to rise. Furthermore, noting higher services inflation ignores the strong likelihood that this is mainly a calendar effect due to the timing of Easter. Moreover, rather than continuing to rise thorough the summer as the ECB hints at, already falling fuel prices may start to pare back overall HICP numbers from this month on – fuel prices could knock some 0.2 ppt of the figure for June. And of course, this also sits alongside continued signs of softer wage growth, something that sits uneasily with services inflation moving in the opposite direction – at 3.2% out to 2028 the ECB projection for employee compensation sits well with the 2% HICP target

Figure 2: Not Everything Suggests Price Pressures Broadening Out

Source: Eurostat, CE, % chg y/y

Indeed, and arguing against any clear wage spiral emergence, an ever-wider array of survey data suggest also that job losses are also starting to become worryingly widespread as business confidence spirals down. Notably, the service sector is being hit especially hard by the cost surges created by the war. Moreover, what is even more notable is that supply shortages not only pose upside risks to prices but can and seem to be constraining real activity already growth already and probably more so in the coming months. With this in mind, how little the ECB revised it real economy outlook this month is as important as how inflation was altered, the former very much helping determine both the size and persistence of any price shock – one that does seem to be increasingly supply related. But these factors explain our below-consensus GDP outlook, one that is very much with downside risks that reflect obvious adverse global factors and real income damage from higher fuel prices, but also ECB policy.

Moreover, ECB policy is biting adversely, either directly or indirectly through three channels. Firstly, financial conditions have tightened even further, underscoring that the discount rate was and is a poor guide to the policy stance. Secondly, the ECB is still drawing down its balance sheet with excess liquidity (at EUR 2.4 trillion) having halved from its peak and set to fall toward EUR 1.5 trillion by end-2027. Since the ECB’s bond portfolios very well might continue to shrink even then, the idea is that regular liquidity operations would become more used by banks to offset that effect. Then, at some point, the ECB would introduce structural liquidity operations. Thirdly, as lending surveys have reputedly shown, banks are not just more reluctant to lend but are actually rejecting an increasing amount of possible loans, especially those that have less collateral attached (Figure 2).

However, it is the case that the ECB is still reverberating from the 2022 energy shock and criticism it faced of hiking both too late and too slowly. If so, the ECB is getting confused. What is notable is that this energy shock and the ECB’s positioning is very much different to that of 2022, occurring at a point when the EZ economy is operating with a margin of spare capacity as opposed to one reviving from a pandemic induced demand shock. This is accepted clearly by the ECB!