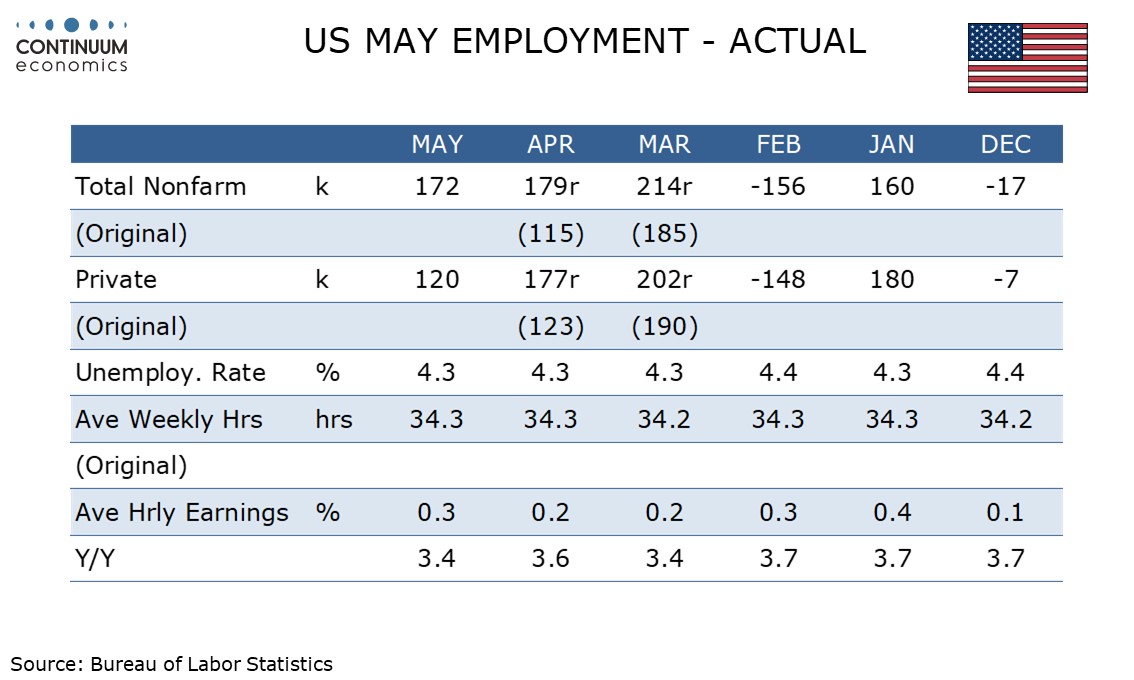

U.S. May Employment - Surprise came from local government and leisure and hospitality

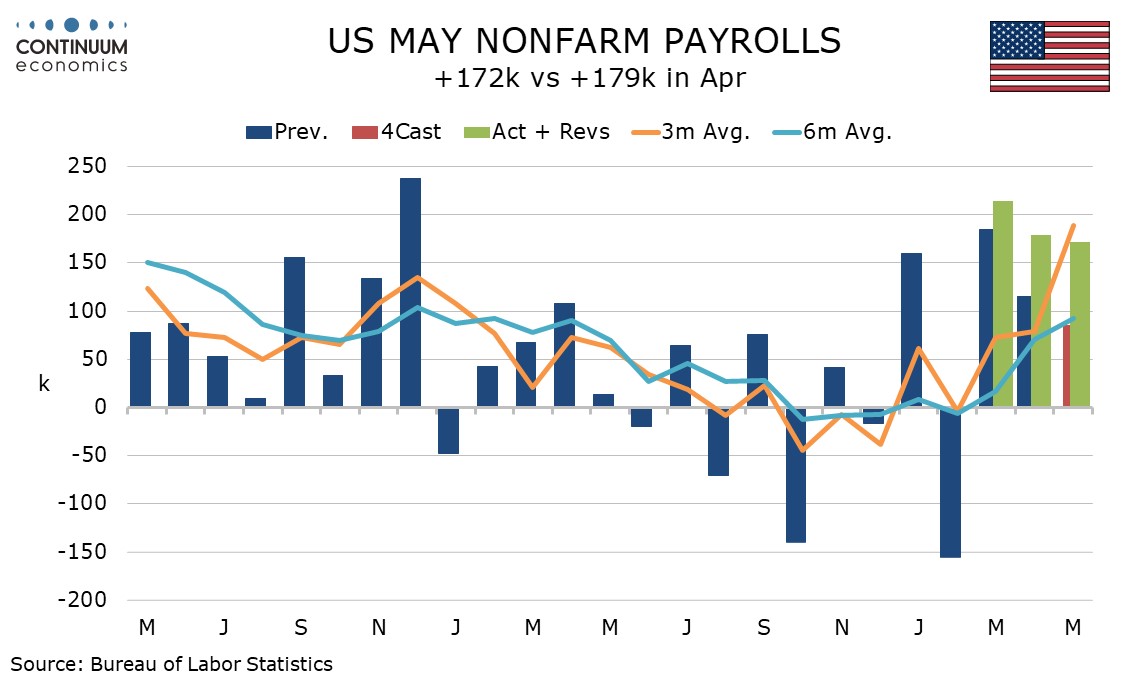

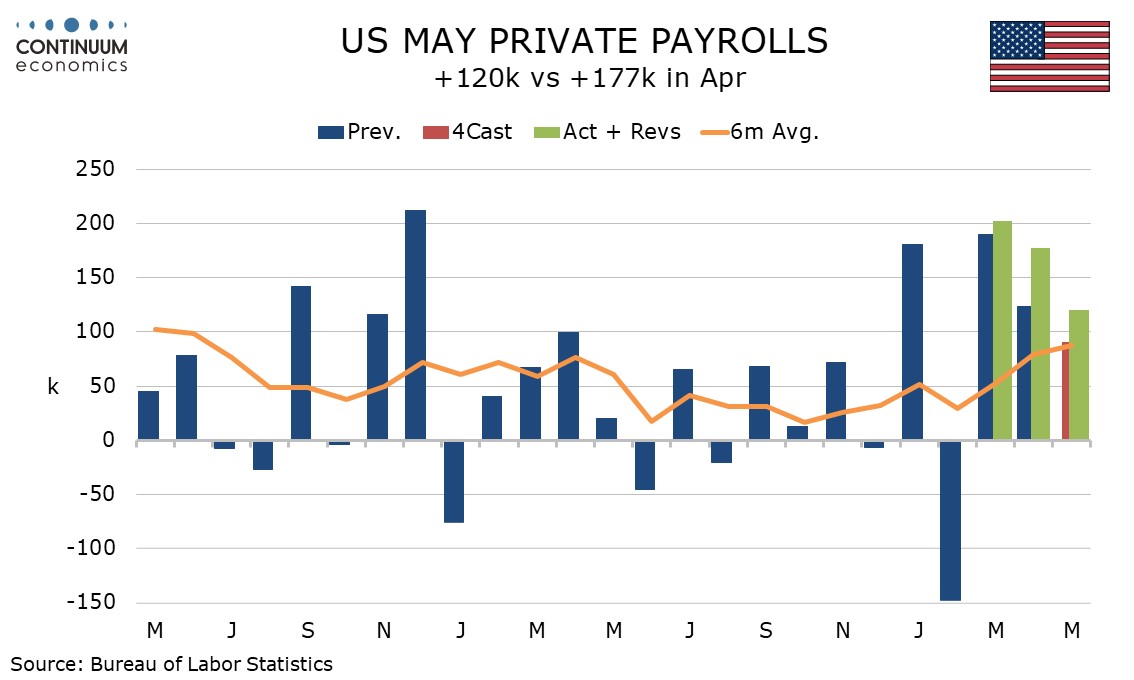

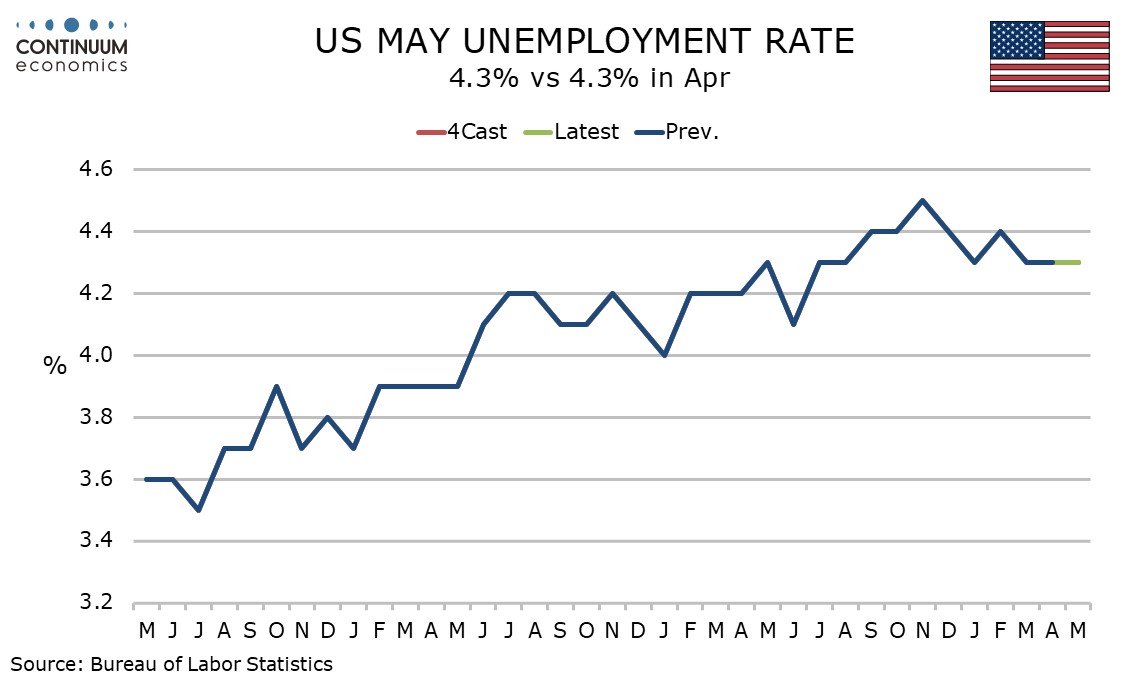

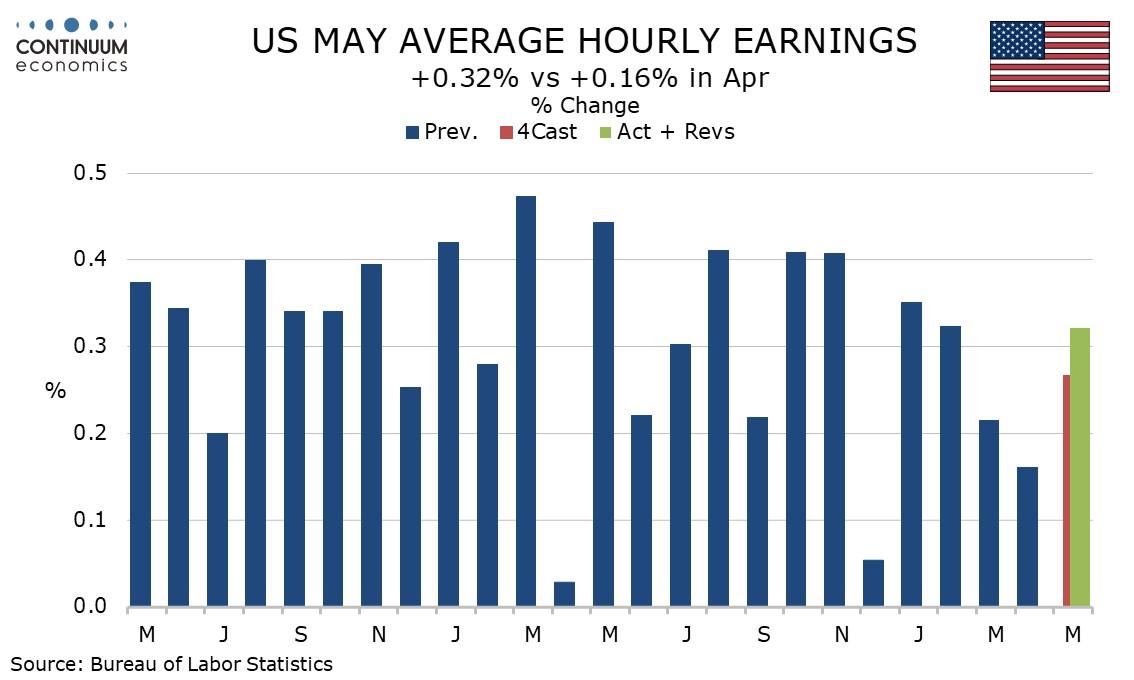

May’s non-farm payroll is significantly stronger than expected with a rise of 172k though the private sector was less impressive at 120k, if still healthy. Upward revisions to March and April add to the positive message. In addition to government, leisure and hospitality with a 70k increase was particularly strong, possibly on World Cup hiring. Unchanged unemployment at 4.3%, an unchanged workweek of 34.3 hours, and a 0.3% rise in average hourly earnings were all in line with expectations.

April was revised to 179k from 115k and March to 214k from 185k, meaning 93k in net upward revisions. The private sector saw April revised to 177k from 123k and March to 202k from 190k, meaning a net revision of 66k. That makes three straight strong gains and supportive of strong early estimates for Q2 GDP.

The three month average of 188k is the highest since March 2024 and the six month average of 92k the highest since February 2025. The healthy job gains are coming despite negative seasonal adjustments assuming strong hiring in the spring, showing that workers are available despite worries over slowing labor force growth.

The household survey shows employment up by 149k, close to the non-farm payroll, while the labor force increased by 83k. While the unemployment rate remained at 4.3% for a third straight month before rounding it fell to 4.296% from 4.337%. The Fed does not seem to have much reason to be concerned about the labor market, meaning that its focus should be on upside inflation risks.

Inflationary pressures from the labor market remain limited. Average hourly earnings rose by 0.32% before rounding, a pick up from two straight gains that rounded to 0.2%, though there is some slowing in trend. Yr/yr growth slipped back to March’s 3.4% pace after rising to 3.6% in April. This is falling behind accelerating inflation.

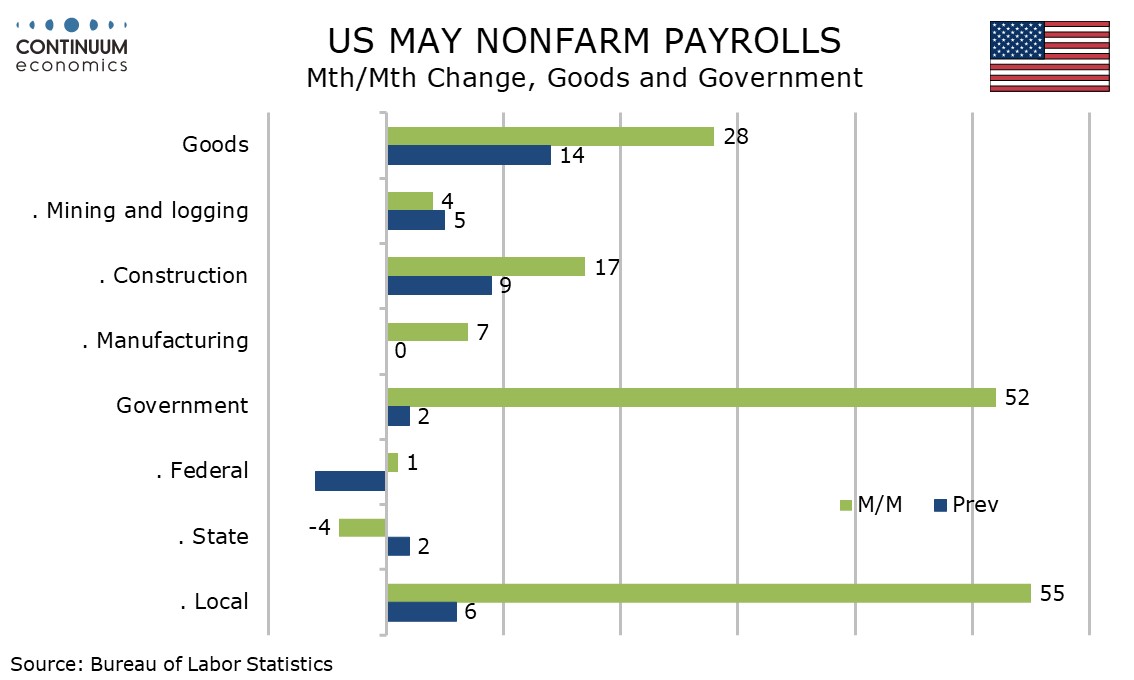

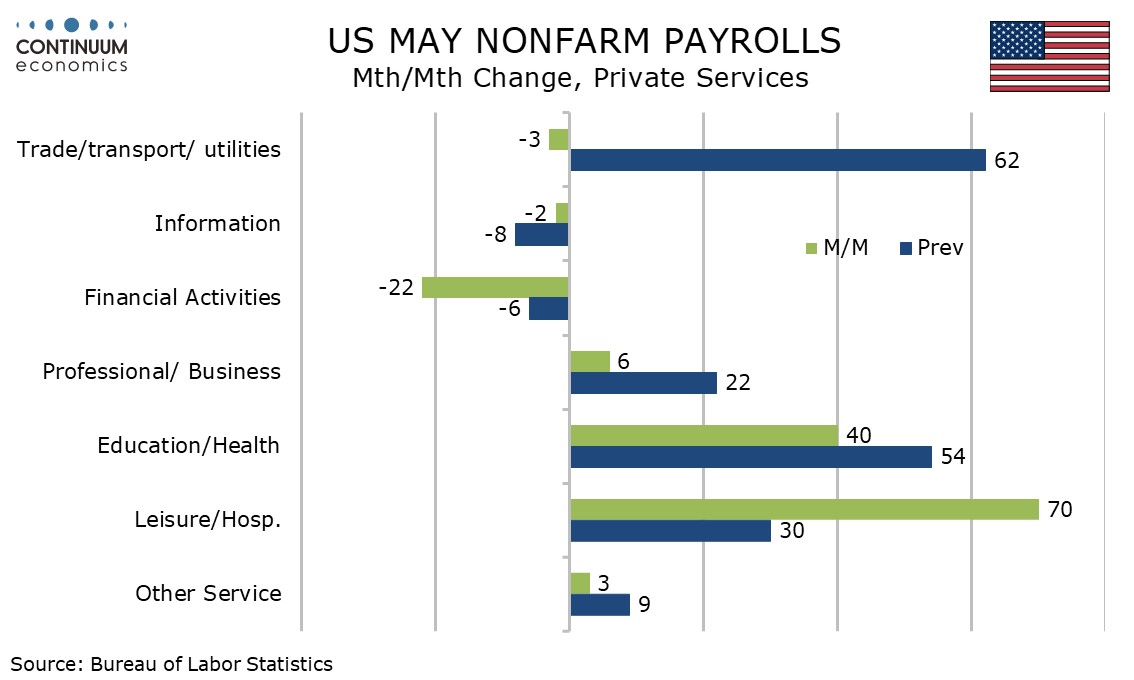

Looking at the non-farm payroll detail, a 52k rise in government was fully explained by a 55k rise in local government which looks erratic. The private sector was supported by a stronger 70k rise in leisure and hospitality with the sector apparently having no trouble fining workers as it approaches the summer. The approaching soccer World Cup may be a factor here. Within the leisure and hospitality detail accommodation rose 11k and food services and drinking rose by 48k.

Education and health, which has led most recent payroll gains, was below trend at 40k with health at 47k. Outside local government, leisure and hospitality and health, payrolls were unchanged. Manufacturing at 7k and construction at 17k both saw moderate gains with the manufacturing six month average turning positive for the first time since January 2024.

Financial activities were weak at -22k with AI probably behind an increasingly negative trend here. Trade, transport and utilities at -3k took a pause after two straight healthy gains. Retail at -1k may be a hint of slowing consumer spending while airlines at -9k reflects the closure of Spirit Airlines. Couriers and messengers rose by only 1k after two straight strong gains.

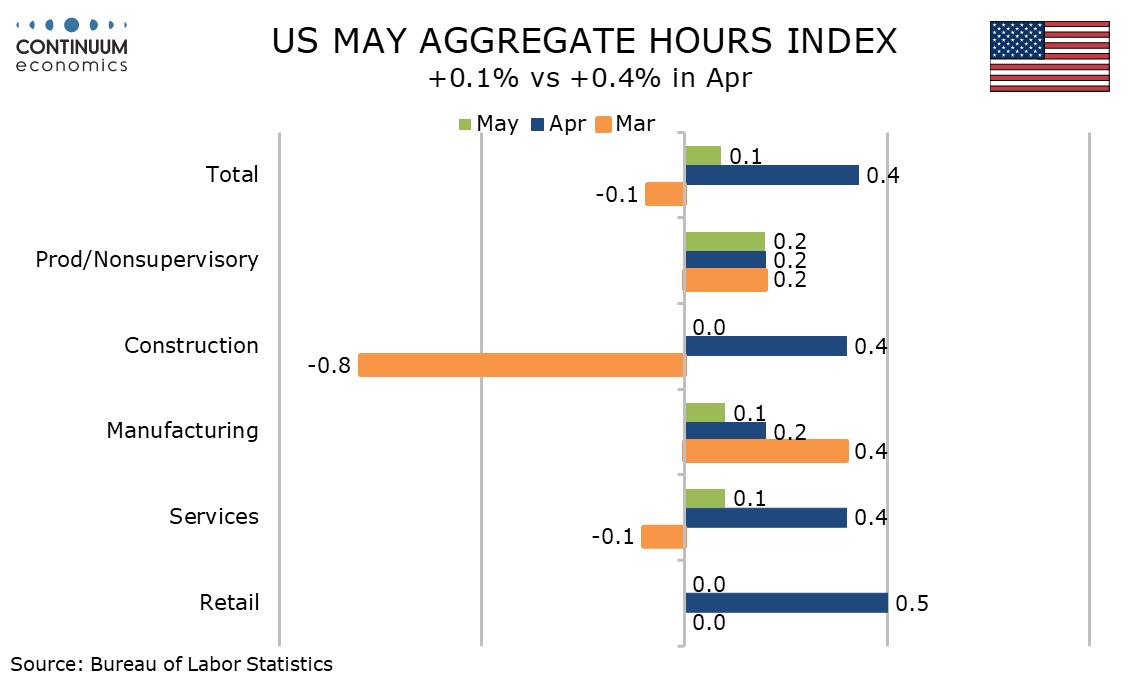

The average workweek remained at 34.3 hours and in the last six months has seen four at this pace and only two at 34.2. This left aggregate hours worked up by a modest 0.1%, with not much diversity in the detail. Information, where employment remains weak, saw a rise of 1.8%, while mining and logging rose by 0.8%, possibly a response to higher oil prices. Employment in the sector rose by 4k.