U.S. May CPI - Surprising fall in transport services despite continued gains in air fares

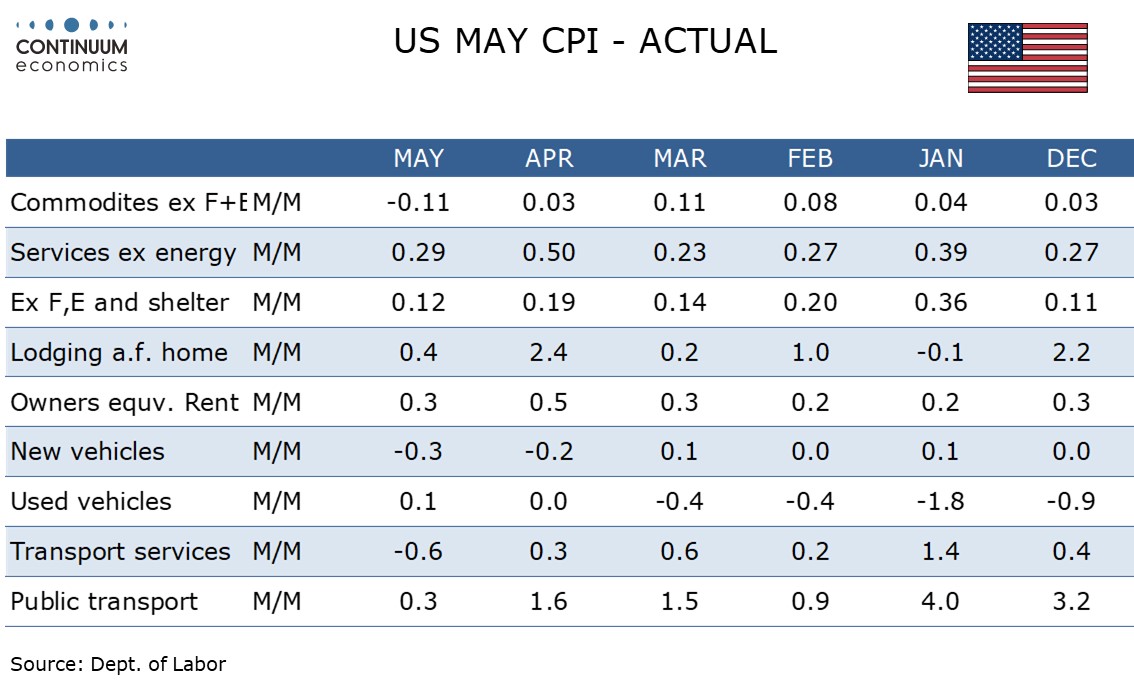

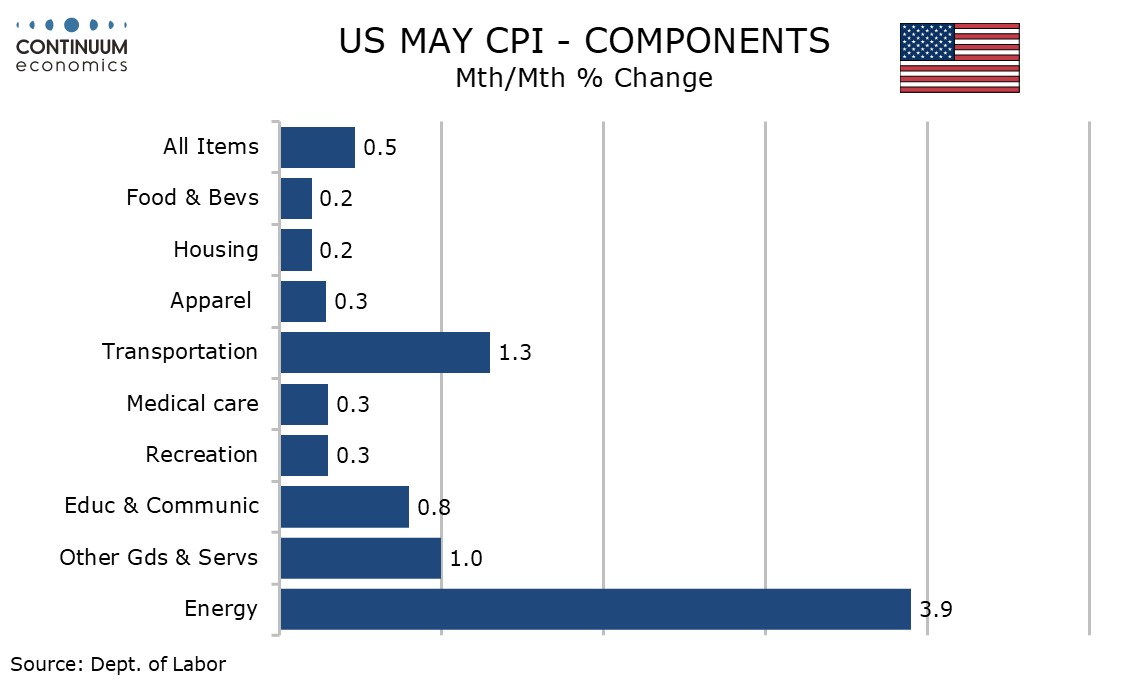

May CPI is in line with expectations at 0.5% overall but the core rate ex food and energy was softer than expected at 0.2%, with the rise before rousing being 0.208%. The most surprising restraint on the data was a 0.6% fall in transportation services, despite continued gains in air fares.

Air fares rose by 2.7%, similar to their gains seen in March and April, but this was outweighed by a 1.7% fall in motor vehicle insurance, which has over twice the weighting of air fares. Public transportation rose by only 0.3% despite the rise in air fares, with declines seen in ship fares and intracity transportation.

Services less energy rose by 0.3%. Strength was seen in education and communication at 0.9% led by postage and delivery services which may be a pass on of transport costs, while miscellaneous personal services were strong at 2.1% led by tax preparation and other accounting fees, which does not appear related to energy. Medical care services rose by 0.5% after two straight flat months.

Shelter returned to trend at 0.3% after a 0.6% rise in April which was distorted by components which are updated every six months having a missing month in October due to the government shutdown. Owners’ equivalent rent also rose by 0.3% while lodging away from home, often a source of volatility, was similar at 0.4%. CPI ex food, energy and shelter rose by only 0.1%.

Commodities less food and energy fell by 0.1%. Used autos saw their first increase since October (it was one of the few components to be surveyed that month) but this was outweighed by a steeper decline in new autos. Apparel continues to rise but at a moderate pace of 0.3%. Most components were subdued with the tariff impact fading with medical care commodities particularly so at -0.7%.

Energy at 3.9% was led higher by an expected strong 7.0% rise in gasoline but food was subdued at 0.2%. The overall CPI rise was slightly less than 0.5% before rousing, at 0.473%.

While the energy strength cannot be dismissed with the situation in the Middle East still far from a resolution, the Fed can be relieved by this release, and feel little pressure for a near term tightening. Still, yr/yr core CPI did pick up to 2.9% from 2.8%, reaching its highest since September (there was no survey in October) while overall CPI at 4.2% yr/yr from 3.8% is the highest since April 2023.