Economic Data and Events Week Ahead Jun 29 - Jul 3

The week ahead has plenty of notable events, spanning Eurozone inflation on one side, to US payrolls on the other, and with central bank speakers all round - the ECB Sintra conference at the start of the week hears from Lagarde and then a panel that includes Warsh and Bailey.

Data and events for the week ahead

USA

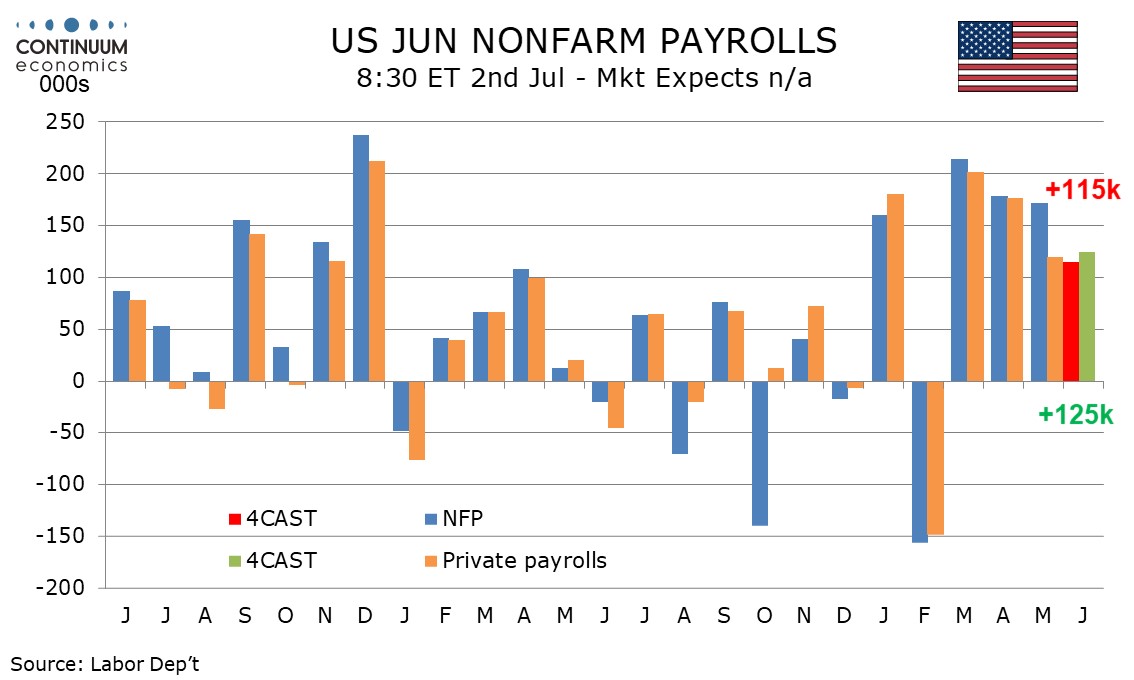

The data highlight in the US will be June’s non-farm payroll, due on Thursday due to Friday seeing the Independence Day holiday. We expect a rise of 115k, 125k in the private sector, with temporary hiring for the World Cup likely to weigh against a loss of underlying momentum. We expect unemployment to be unchanged at 4.3% and an in line with trend 0.3% increase in average hourly earnings. Other labor market indicators come from May’s JOLTS report on job openings on Tuesday, Wednesday’s ADP report of private sector employment, for which we also expect a rise of 125k, and weekly jobless claims on Thursday.

Tuesday sees June consumer confidence as well as April house price data from S and P Case-Shiller and FHFA. Wednesday sees May construction spending and June’s ISM manufacturing index, which we expect to be unchanged at 54.0. May factory orders are due on Thursday. Fed’s Warsh will speak on Wednesday and will be closely listened to.

Canada

Canada releases April GDP on Tuesday. We expect a 0.3% increase, slightly below a 0.4% estimate made with March data. June’s S and P manufacturing PMI is due in Thursday.

UK

Coming before final PMI data (Wed & Fri), there are final Q1 GDP numbers where no revision is envisaged (Mon). Published alongside, will be current account data, the gap likely to widen slightly beyond 2.5% of GDP. Otherwise, the BoE dominates the week with Monday’s money/credit data likely to show more signs of a softer housing market, thereby chiming with anecdotal evidence. Such signs may get short shrift from MPC hawk Mann who speaks (Thu) but may mention in updated BoE Credit Condition Survey data (Thu) or via the latest Decision Maker’s Panel (Fri).

Eurozone

Data wise, there are final manufacturing and services PMI numbers (Wed/Fri). Otherwise, the week is dominated by Monday’s actual money and credit figures, where some credit weakness is emerging, these coming almost alongside Thursday’s labor market data which still suggest abundant workforce supply. Monday also sees key survey data for the European Commission, likely to chime with PMIs in signalling on-going economic fragility.

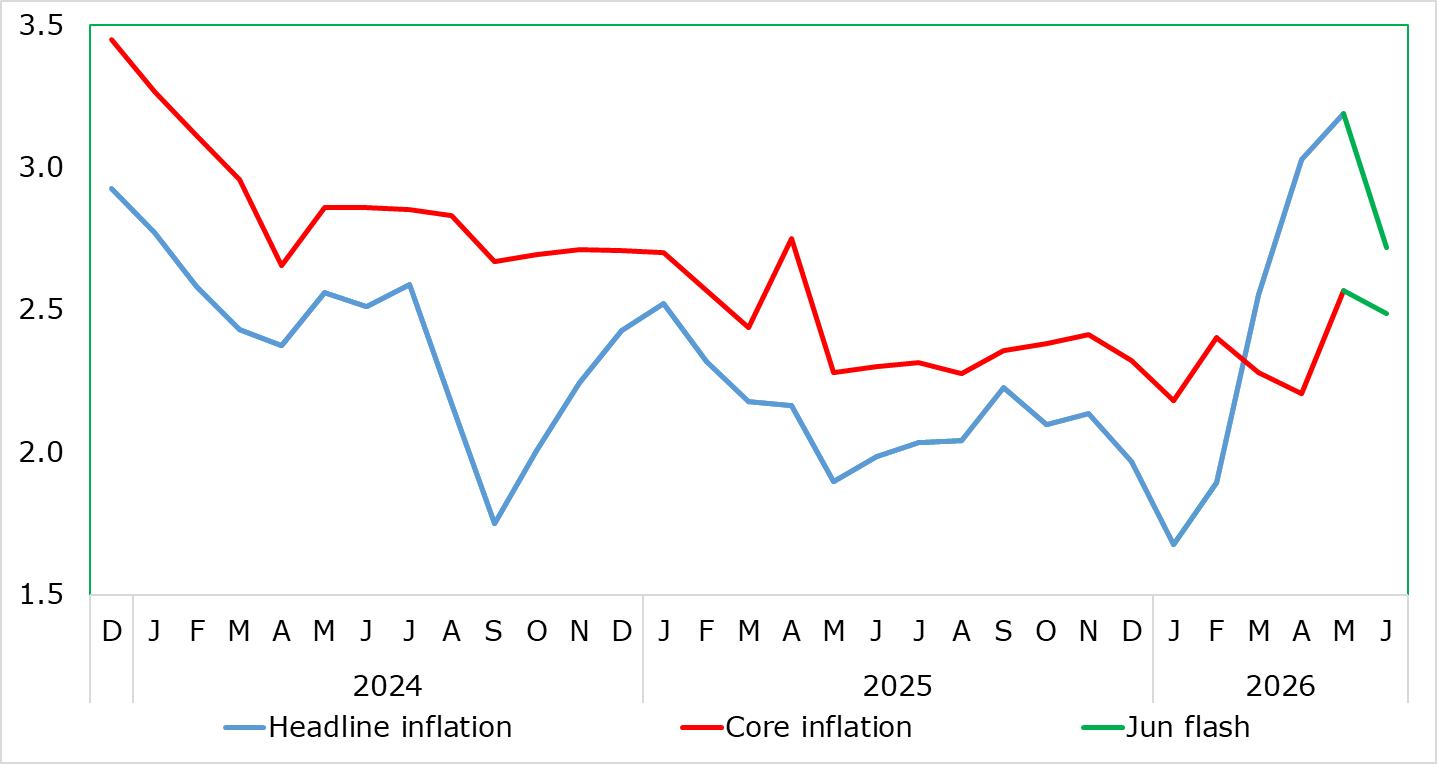

But the main event will be the June HICP flash (Wed), partly flagged by German HICP numbers (Tue). These data may have a material impact on ECB thinking, especially as they arrive toward the end of the ECB monetary annual gathering in Sintra (Mon-Wed). Indeed, the numbers may suggest the headline rate peaked at 3.2% in May and not the 3.4% rate implicit for June in the ECB quarterly projections released earlier this month. In fact, we see the headline down to as low as 2.7% pulled down not just by hefty energy price falls but also a seasonal aberration in travel prices that pushed up services inflation in May. This could involve small dip in the core too. House price data arrive on Thursday.

Rest of Western Europe

There are few key events in Sweden. In Switzerland, Tuesday sees the latest KOF survey update and Thursday sees what may be near-unchanged headline June CPI numbers, such an outcome chiming with the SNB latest projection. The SNB also releases its latest Financial Stability Report. Norway on Friday releases the latest credit numbers, alongside updated Unemployment figures.

JP

Kickstarting the week with Retail sales. It would be great to see a positive outcome as consumption has been lagging behind real wage gains. Followed by labor data on Tuesday and other tier two data throughout the week. Both shouldn’t be JPY moving.

AU

RBA Governor Bullock will be speaking on late Sunday yet unlikely to provide new cues for rate move, given the current inflation dynamics. So as the meeting minutes on Tuesday. Trade balance on Thursday will likely be more important for changes in energy import.

NZ

Only consumer confidence on Friday may catch an eye.