ECB April 30 Account: Not Willing to Look Through Energy Shock?

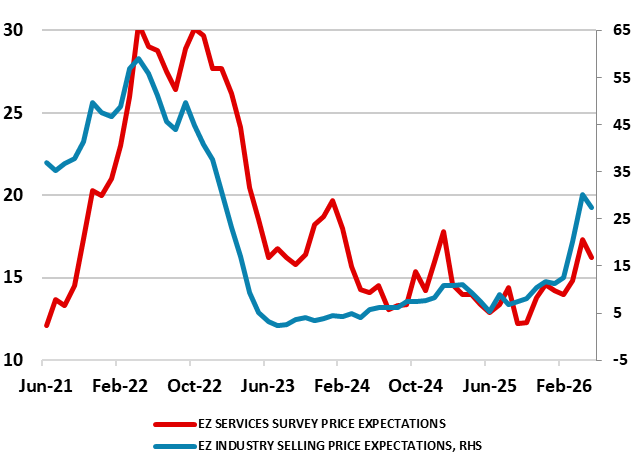

The Account of the April 30 ECB meeting offers few added clues with comments from Council member since more directly suggesting a precautionary if not pre-emptive 25 bp rate hike on June 11. As was case back then, markets are seeing two such moves by September and a strong probability of a third by December. We think that the June meeting hike is now a done deal, with the April decision actually having been a close call to some members. But we remain wary about both the size, timing and durability of any subsequent hikes, not least amid what have been soggier real economy numbers that will only accentuate ECB concerns that markets have a dissonance with the current pricing of energy. Even so, compared to late April, it is worth noting that the energy backdrop currently has eased with gas prices largely in line with ECB March projection thinking while oil prices have fallen almost 20% from the highs they saw then. Moreover, while the ECB has asserted that its statistical techniques point to higher core inflation, we note data very much to the contrary (Figure 1).

Figure 1: Service and Factory Sector Selling Price Expectations Backing Off?

Source; European Commission

Regardless, it does not seem as if the ECB will look through the energy supply shock, In April having stressed the need to signal vigilance and communicate that upside risks to inflation and downside risks to growth had intensified, but where implicitly the former is dominating the policy debate.

Part of that debate noted that the current shock was more global in nature than the 2022 shock, which had affected Europe the most. This is important as a global shock with production networks generated a more negative hit to economic activity as well as more pressure on import prices than a local shock, as higher energy costs were embedded in the prices of imported intermediate and final goods. Indeed, and arguing against any clear wage spiral emergence, an ever-wider array of survey data suggest also that job losses are also starting to become worryingly widespread as business confidence in any swift turnaround in the adverse economic climate fades further. Notably, the service sector is being hit especially hard by the cost surges created by the war. Moreover, what is even more notable is that supply shortages not only pose upside risks to prices but can and seem to be constraining real activity already growth already and probably more so in the coming months but also have the potential to add further upward pressure to inflation. With this in mind, in assessing the post- June policy outlook, how the ECB revises it real economy outlook next month will be as important as how inflation is altered, the former very much helping determine both the size and persistence of any prove shock – one that does seem to be increasingly supply related.

As for inflation the data is far from conclusive that second-round effects are likely to be sizeable. As the ECB noted, survey data indicated an increase in the expectations of firms regarding non-wage cost components and selling prices, suggesting that indirect effects were materialising, although there was limited hard data as yet. The flash PMIs for April had shown the fastest increase in the input costs of firms since 2022 and selling price expectations had increased to their highest level in three years. But European Commission data (offering a wider sector and geographical perspective than the PMIs) suggest otherwise, with not only far more muted rises in price expectations but where that latter seemed to have started to reverse already (Figure 1).