Germany/France/Italy and Spain: Growth and Inflation Outlooks

· We have retained our 2026 GDP picture of 0.3% (Our Forecasts below) and actually pared back that for next year, with more and more signs that China is continuing to ship cheap products to Germany (lower energy prices post Iran war still help 2027). For France, we have made a 0.3% downgrade to the already soft and fragile French economic outlook for this year or next, now seeing GDP growth at 0.4% and 0.7% respectively. Meanwhile, we still expect a non National Rally candidate to win the 2027 presidential election.

· For Italy, the consumer is relatively more exposed to swings in energy and we see 0.5% GDP. Notably, into 2027, we see little better growth as unused and/or exhausted RRF payments fade. For Spain, under our main assumption of a reopening of the Straits of Hormuz, we see GDP growth of just 2.0% this year, a clear contrast to the 2.8% 2025 figure (lower migrant flows in 2026) and actually a 0.3 ppt upgrade from three months ago.

Our Forecasts

GDP Growth | HICP Inflation | Discount Rate (%) | |||||||

| 2025 | 2026e | 2027e | 2025 | 2026e | 2027e | 2025 | 2026e | 2027e |

Eurozone | 1.5% | 0.4% | 1.1% | 2.1% | 2.5% | 1.8% | 2.0 | 2.25 | 1.75 |

France | 0.9% | 0.4% | 0.8% | 0.9% | 2.4% | 1.9% | - | - | - |

Germany | 0.3% | 0.6% | 1.5% | 2.2% | 2.6% | 1.9% | - | - | - |

Italy | 0.6% | 0.5% | 0.6% | 1.7% | 2.9% | 1.9% | - | - | - |

Spain | 2.8% | 2.0% | 1.4% | 2.7% | 3.1% | 2.2% | - | - | - |

Germany: Still Fragile?

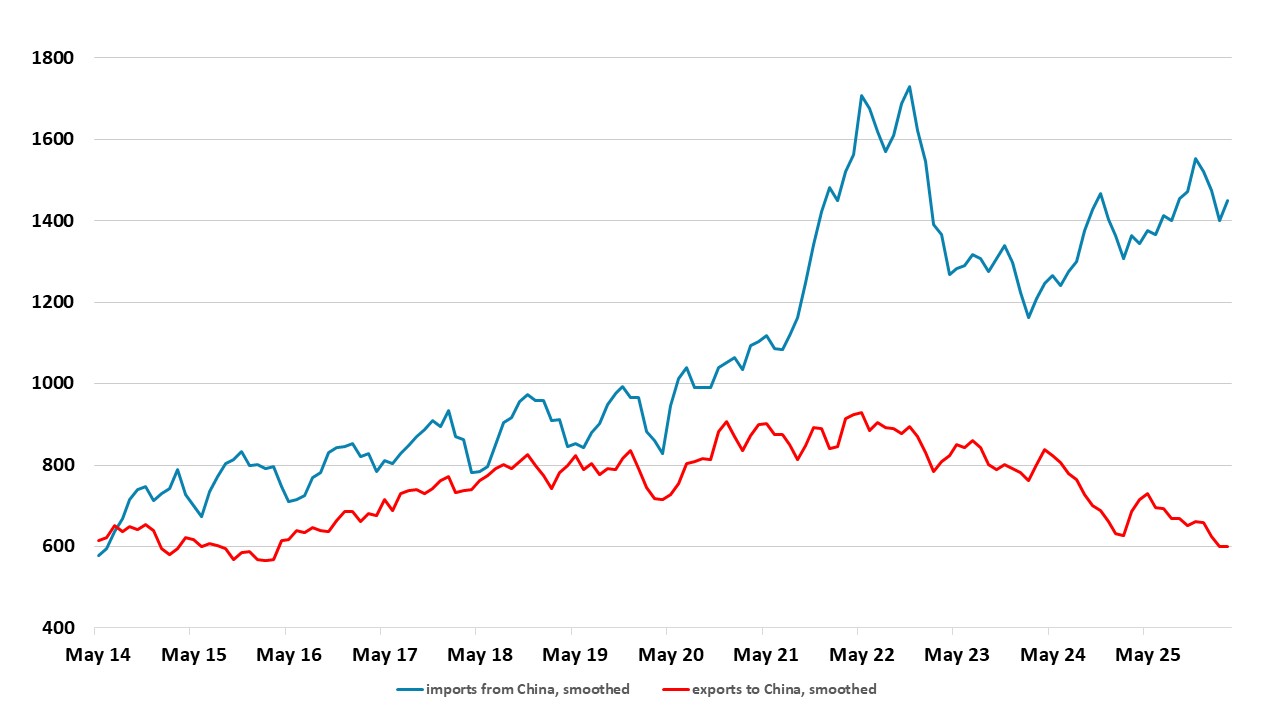

In surprisingly almost matching the better than expected end to 2025, GDP data very much surprised on the upside despite some clearly negative early-year monthly data. But survey data still imply that tariffs, the stronger exchange rate, political tensions and uncertainty are very much still hurting Germany’s aging and out-dated economy. It is against this backdrop that we have retained our 2026 GDP picture and actually pared back that for next year, with more and more signs that China is continuing to ship cheap products to Germany (Figure 3). As for trends, even given the solid Q1 2026 performance, the German economy has on average, shrunk by an average 0.1% q/q since end-2022. And the question is now just whether even the now more limited Middle East fall-out will offset the planned landmark fiscal expansion, the first signs of which appeared at end-2025.

Figure 1: Germany’s Trade Divide with China Continues to Grow

Source: German Fed Stats Office, EUR billion

The little changed GDP outlook implies a still large output gap of up to 2% of GDP that makes us still confident of continued underlying disinflation ahead. Admittedly, there will be a clear impact on CPI inflation from the conflict and we have raised the 2026 forecast by 0.3 ppt to 2.6%. This is seen being short-lived to a degree, we have pared back the 2027 outlook a notch to slightly higher 1.9% - this upgrade reflecting a likely reversal of the government fuel price subsidies. Even so, it would be wrong to overstate the impact of the planned German debt surge. Multiple challenges will impede the government’s spending plans, not least growing splits within the coalition over policy priorities, although we do not consider that these will be audible enough to prompt the government to collapse. Regardless, there is the (in)famously slow procurement process for military equipment widely regarded as overly bureaucratic. Secondly, there are the existing capacity constraints in the German and European defence sector. Moreover, Germany faces subdued productivity growth and adverse demographics.

The bottom line is that a German budget could turn into one of well over 4% (both headline and structural) probably not this year but into 2027. As a result, the government debt ratio would rise from its current 63% of GDP toward 80% over the next decade possibly without negative repercussions – not least as Germany has already suggested EU-wide fiscal rules (which this initiative compromises) need to be relaxed. But added government defence spending will boost imports.

France: Polarized Politics and Fiscal Woes Intertwined?

There are some upside risks in an economic outlook dominated by ever clearer, and likely to be sustained, fiscal problems. These are all centred around how next year’s presidential election may fare, where the risks remain very much that what are currently merely fiscal and political tensions could turn into a genuine crisis. The French political system is partly to blame; the two-stage process of French elections means that parties of the left and of the centre will likely combine to stop any National Rally candidate (currently ahead in the polls) winning. This implies more parliamentary deadlock, which in turn points to a continued fiscal stalemate, the latter suggesting further credit agency criticism and even downgrades. This will only add to existing economic weakness that may be exacerbated by market-induced fiscal policy consolidation and greater budget problems. Indeed, it is still likely that the budget gap this year will be no lower than the 5.4% seen last year, before edging up to 5.7% in 2027. Public debt is thus set to increase to some 120% of GDP by 2027, up from 115.6% in 2025, on the back of sizeable primary deficits.

All of which helps explain the attempt to find investment from abroad. It is seemingly going in the right direction as France secured more than EUR 110bn of proposed AI and data centre investments last (i.e. almost 4% of current GDP). The commitments, announced around Macron’s Choose France investment summit, amount to roughly 10 gigawatts of additional computing capacity — equivalent to the output of about 10 nuclear reactors. The projects will test whether President Macron can overcome longstanding energy bottlenecks in order to become Europe’s tech powerhouse.

Despite the emerging energy price shock, we have made a 0.3 pt downgrade to the already soft and fragile French economic outlook for this year or next, now seeing GDP growth at 0.4% and 0.7% respectively. The downgrade for this year makes a weak Q1 GDP outcome which still featured a marked rise in inventories, the later unlikely to be repeated and more likely reversed. This underscores an economy with plenty of spare capacity (Figure 4). The real economy picture is helped by what will still be low inflation rates but which is higher by a full ppt this year at 1.4% and 1.8%, the latter little changed from that envisaged three months ago.

Notably the pick-up in 2027 is on the back of fiscal expansion in Germany and better net exports partly related to increased EU defence sending (France’s large defense industry provides almost 10% of global arms exports). But the risks are clear from the above analysis. Notably, we do not see France being a major part of any clear defense-based fiscal expansion given its adverse budgetary backdrop and outlook.

Italy: Politics Vs Fiscal Fragility

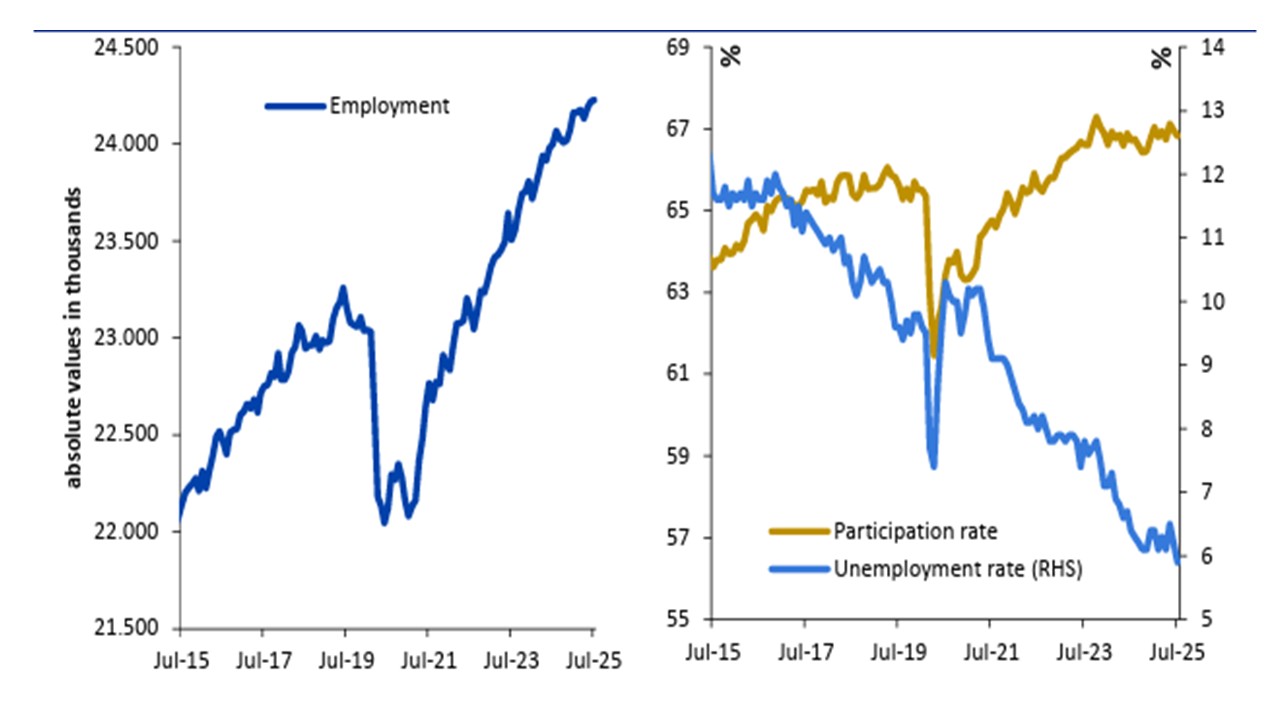

Although a general election is not due until end-2027, PM Meloni may be wary whether her Brothers of Italy Party can remain ahead in opinion polls until then. Indeed, electoral concerns may be behind her clear criticism of the U.S. attack on Iran, this all the more notable given the her relatively close relationship with Trump. But her motivation for this more pro-EU stance is that the conflict obviously has consequences for an already lacklustre Italian economy which if sustained could have electoral repercussions too. This is especially so for the consumer which is relatively more exposed to swings in energy. At this juncture, however, we see limited additional price pressures feeding through but CPI inflation this year may jump to average 2.9%, a full ppt higher than pre-conflict but fall back to below target in 2027, albeit with a declining trend through the rest of this year. Notably, into 2027, we see little better as unused and/or exhausted RRF payments fade. But there are upside risks too; Italy’s large arms exports (5% of the global market) may benefit from rising EU defense spending while household consumption, helped by a solid labour market (Figure 4 highlights record-high labour force participation) may still see actual real wage growth if our CPI projections prove anything like accurate.

Figure 2: Record Labour Participation

Source: ISTAT

Partly this reflects genuine fiscal improvements, including a primary fiscal surplus, though largely a one-off result of the unwind the Superbonus scheme. However, the overall budget deficit is projected to fall from 3.1% of GDP in 2025 to 2.9% in 2026 and 2027. Still, the debt ratio is set to rise further to over 139% in 2027. The bottom line is that while hardly yet in a fiscal vicious circle, budgetary dynamics are unfriendly and that is without the added formidable challenges in meeting Italy’s NATO defence spending commitments (which at face value could ramp the debt ratio much higher and much earlier).

Spain: Trump vs Sanchez?

Like the rest of Europe, Spain is very much sensitive to the Middle East conflict. Under our main assumption of a reopening of the Straits of Hormuz, we see GDP growth of just 2.0% this year, a clear contrast to the 2.8% 2025 figure and actually a 0.3 ppt upgrade from three months ago. Regardless, a better quarterly profile emerges into 2027 but with average growth still of 1.4%, this seeing similarly sized but negative downgrade. And there may be downside risks to both years especially given the possibility that even if the current conflict has ended, Spain may come under fresh attack from the Trump administration seeking retaliation for Prime Minister Pedro Sánchez’s refusal to let U.S. military use jointly operated air bases on Spanish soil to attack Iran. This was widely accepted by most Spanish political parties and is partly posturing ahead of the looming general election, due no later than August this year. Notably, the U.S. is Spain’s leading supplier of fossil fuels providing some 15% of crude oil and three times that of LNG imports. There are also the risks of financial sanctions on Spain, this notable given that Spain’s largest bank, Santander, is trying to increase its exposure to the US banking sector.

Regardless of how trade relations with the U.S. shift, Spain’s economy is already being affected by the attack on Iran and with business surveys continuing to suggest a slowing in activity already underway. Energy prices are already rising across the board, and although at this juncture we see limited second round effects, we have lifted our CPI projection this year by 0.7 ppt to 3.1%, but (again) with little change to 2027 forecast of 2.2%. Both figures encompass some early unwinding of recent government energy subsidies This will obviously have an adverse effect on real incomes with an added negative the likely impact on sentiment too. But there is also the likely negative impact on the tourist industry and not just from far less solid economic activity by Spain’s key trading partners but also from higher airfares and hotel costs, albeit some upside as some boost may come from tourism re-routed from the Gulf.

These risks are superimposed over what may be more structural issues; Spain is very much in the hot seat when it comes to climate change, having suffered clear damage from storms, heatwaves and drought. There is also going to be no rapid defence build-up, amid an aversion to the military. The main one, however, being a more-pronounced-than-anticipated slowdown of migration flows will reduce the dynamism of the labour market, explaining the pared back outlook we have for private consumption and investment. Indeed, migration flows of over 3% last year may give way to nearer 2% this year and something similar into 2027. This may still feed what has been strong import growth of late meaning we see the current account deficit in 2026 and 2027 staying at the narrower circa 2.7% we see for 2025.

This demographic backdrop, almost unique to Spain within the EU, is best understood by the fact that per capita GDP growth last year was around 1.5%, admittedly still well above the EZ average, but highlighting the extent to which population and workforce growth have been supporting activity. Note that productivity has been a more anaemic 0.5% which we think will persist into 2027, thereby reining back potential growth from its current circa 2.5%. But the clear beneficiary of this very solid overall GDP backdrop of recent years has been the marked swing on the fiscal side which had seen persistent budget gaps of around 7% of GDP a decade ago give way to a deficit last year just under 3%. This may even rise back this year however, given the weak economy and possible fiscal aid to households.