EMEA Outlook: Domestic Uncertainties Dominate

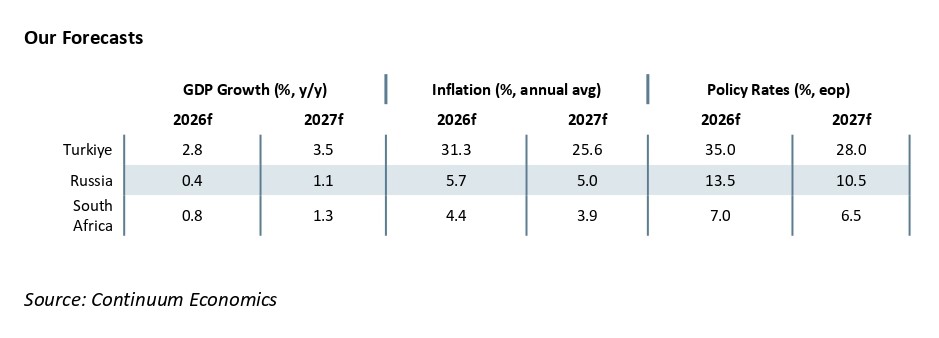

· In South Africa, we foresee average headline inflation will stand at 4.4% and 3.9% in 2026 and 2027, respectively. This baseline assumes easing energy prices starting in Q3, though second-round inflationary pressures from the Iran conflict will linger for some time. Accordingly, we forecast GDP growth at 0.8% in 2026 and 1.3% in 2027; while ongoing renewable energy investments and reduced loadshedding will support activity, growth will be constrained in H2 by energy shocks, high unemployment, and elevated borrowing costs. Given these risks, a cautious South African Reserve Bank (SARB) is expected to hold the policy rate at 7.00% through the end of 2026, before cutting it to 6.50% by late 2027 as inflation nears the 3% target.

· In Turkiye, rising energy prices, unanchored pricing behavior, and sticky services costs continue to threaten the disinflationary process. Due to upside risks, our average inflation forecast for 2026 has been revised upward to 31.3%. We expect the Central Bank of the Republic of Turkiye (CBRT) to lower its policy rate to 35.0% in Q4 after fall in oil prices, which should continue into 2027 as price pressures cool. Meanwhile, high inflation, elevated interest rates, and tighter fiscal policy continue to weigh on economic activity, keeping our GDP growth forecasts at 2.8% for 2026 and 3.5% for 2027.We think growth could see an earlier-than-expected boost if a presidential election is called for October–November 2027 rather than 2028.

· In Russia, the Ukraine war continues to create high military spending and strong fiscal stimulus in addition to aggravation of staff shortages. Our baseline scenario in Ukraine is the war dragging on throughout 2026 (70%) and the alternative is a Russia-friendly peace deal (30%) likely in H2 2027 due to exhaustion. Our 2026 average headline inflation forecast is 5.7% owing to lagged impacts of previous aggressive monetary tightening and relative resilience of RUB. Our end-year policy rate prediction stands at 13.5% for 2026 as we foresee Central Bank of Russia (CBR) will continue its easing cycle in H2, with a slower pace. We envisage growth to hit 0.4% in 2026 due to expected fall in oil prices in H2 as Iran conflict dissipates coupled with adverse impacts of sanctions.

Forecast changes: From our March outlook, we lifted our 2026 end-year key policy rate for Turkiye to 35.0% due to stubborn inflation and energy shocks; and hiked our 2026 average inflation forecast for Turkiye to 31.3% due to inflationary risks and sticky core services prices. We also increased our 2027 end-year key policy rate for South Africa to 7.0% due to inflationary pressures. We reduced our 2026 GDP growth forecast for Russia to 0.4%.

Fragmentation in EMEA: Geopolitical Headwinds and Diverse Domestic Dynamics

We believe the volatile food and energy prices, global uncertainties, weak Chinese demand and country‑specific dynamics will continue to shape the EMEA outlook in H2 2026.

While geopolitical tensions persist, we anticipate the Straits of Hormuz will reopen and remain clear following the conclusion of the U.S. naval blockade, which has been facilitated by the signing of an interim agreement. We feel the direct economic fallout and second-round inflationary pressures on EMEAs should remain modest in H2. As the conflict in Iran deescalates, easing energy prices and fertilizer costs are expected to pull down headline inflation across the EMEA, but slowly in H2.

Monetary policy across the region remains highly fragmented, reflecting uneven progress toward inflation targets, the diverse impacts of the Iran conflict, and differing domestic conditions. The main macro risk in H2 is that the lagged effects of the higher energy prices March-June 2026 could cause a greater growth hit than expected. Despite cooling prices, we think EMEA central banks are poised to remain cautious through Q3, as the second-round effects of previous energy price surges continue to ripple through. We think EMEA central banks will reconsider cutting the policy rates in Q4 2026/Q1 2027 if inflationary pressures soften as expected, but deceleration pace will be the key.

Elsewhere, our major in-House scenario is that the inflation comes down in the U.S. in 2027, and we will likely see two 25bps rate cuts providing breathing room for EMEA markets. While the current U.S.-China trade truce is holding, a comprehensive deal remains unlikely. The lingering threat of aggressive trade disputes through the remainder of the year poses a distinct downside risk to the EMEA growth path despite EMEAs will continue to benefit from greater labor market slack than was seen in 2022, except Russia.

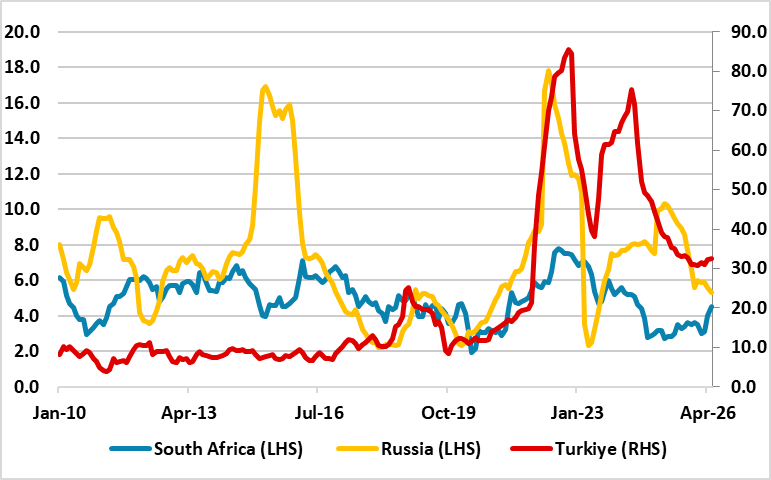

Figure 1: South Africa, Russia (LHS) and Turkiye Inflation (RHS) (%, YoY), January 2010 – May 2026

Source: Continuum Economics, Datastream

South Africa

South Africa had enjoyed moderate inflation remaining within South African Reserve Bank’s (SARB) target band of 2% and 4% in Q1, but inflation reached 4.5% in May, more than the upper end of SARB’s target band. Despite the absence of power cuts (loadshedding) in H1; surges in oil prices, electricity tariff adjustments, and logistical constraints continued to exert upward pressure. (Note: The core inflation surged to 3.8% y/y in May from 3.6% in the previous month, marking the highest reading since October 2024). Because the country imports the majority of its petroleum products, it remained vulnerable to swings in global energy prices in Q2.

While inflation should moderately ease in H2 as Iran tensions subside, the recovery will be gradual. Returning to the 3% target will be slow as modest second-round pressures and rising utility costs will hinder progress in Q3, likely keeping inflation above 4% for the rest of H2. Furthermore, sticky services inflation remaining over 4% and potential El Niño-driven agricultural disruptions present key upside risks for Q4 while the structural impediments inside South Africa's domestic supply chains continue to slow down the speed of disinflation. The headline inflation remains vulnerable to administrative price increases and food price volatility.

We now forecast average CPI at 4.4% in 2026 and 3.9% in 2027, reflecting a higher inflation path than previously expected in the March outlook. We believe the inflation trajectory will continue to be driven primarily by global developments and domestic dynamics while the government’s determination to address electricity shortages, logistical constraints, and financing requirements will be key determinants of the outlook.

Despite concerns regarding the inflation trajectory, there is good news from the power cuts front. South Africa’s national electricity utility company Eskom announced on June 5 that South Africa has now experienced 385 consecutive days without an interrupted supply, with only 26 hours of loadshedding recorded in April and May, 2025. Despite no loadshedding so far in 2026, energy analysts think continued investment build out of energy infrastructure remain key.

The combination of geopolitical uncertainty and domestic price pressures suggests a more cautious approach for SARB the rest of the year despite the conflict in Iran deescalates. We expect SARB to remain on hold in 2026 and keep rate at 7.0% until clearer disinflation emerges and inflation expectations edge down; delaying any meaningful easing until early 2027. Rate cuts should resume once oil prices fully realign with fundamentals and secondary impacts will disappear. We envisage the policy rate will fall to 6.50% by end‑2027 as SARB will likely continue cuts in 2027 once most of the geopolitical risk premium dissipates and headline inflation softens below 4% threshold.

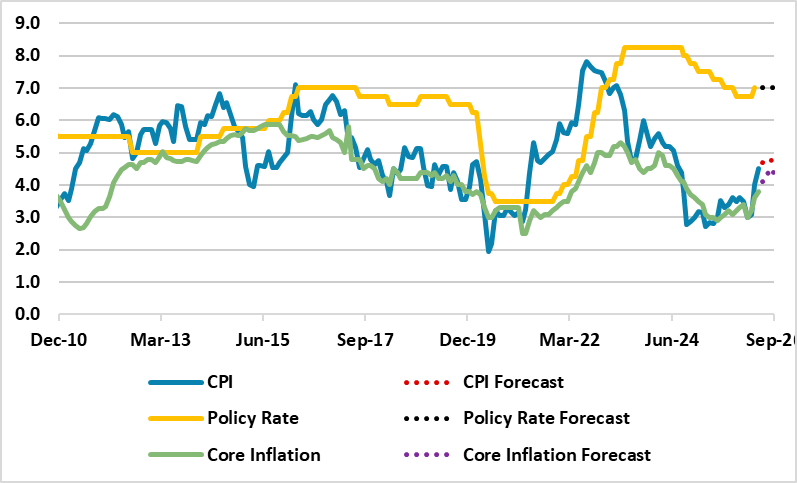

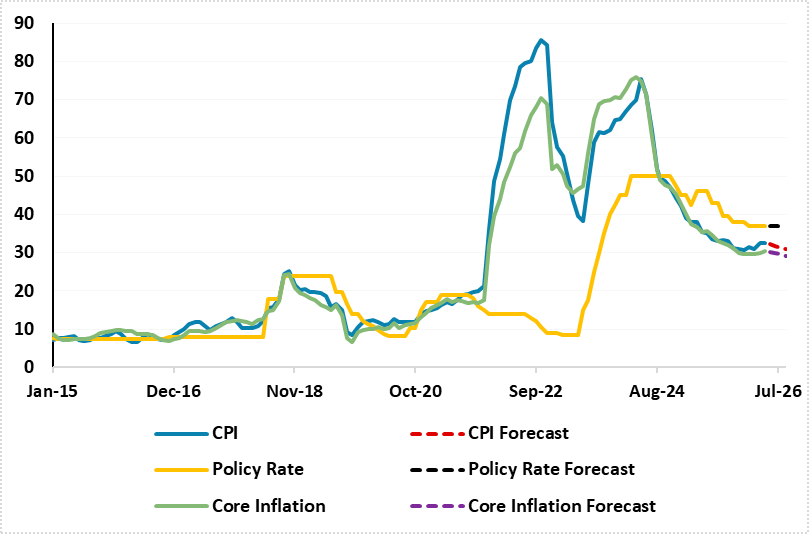

Figure 2: CPI, Core Inflation (YoY, % Change) and Policy Rate (%), January 2010 – September 2026

Source: Continuum Economics

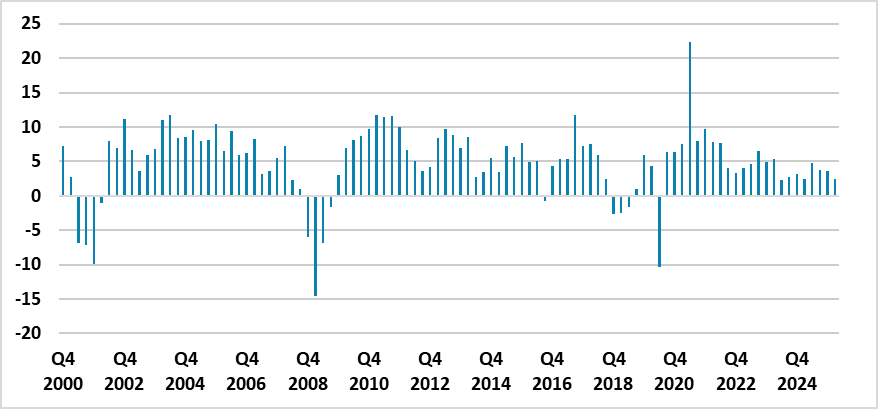

Growth remains modest driven primarily by household consumption. The economy expanded 0.5% in Q1, and we expect 0.8% growth in 2026 before rising to 1.3% in 2027. While improved consumer sentiment, ongoing investment in renewable energy and reduced loadshedding support activity; energy shocks, high unemployment, higher borrowing costs, and logistical bottlenecks will continue to limit the growth trajectory especially in H2. Weak China demand remains a downside risk as well.

Domestic factors such as persistent structural challenges such as unemployment and lack of fiscal space will continue to temper the outlook. Unemployment remains stubbornly high, which require urgent labor market reforms to unlock inclusive growth. (Note: The unemployment rate rose to 32.7% in Q1, with youth unemployment hitting an alarming 60.9%). We think continued implementation of Operation Vulindlela reforms specifically in removing state-monopoly inefficiencies within water infrastructure, digital spectrum, and Transnet’s logistical rail corridors— will be important to unlocking productivity and competitiveness via sparking private sector fixed investment.

Elsewhere, political friction, slow reforms, and fiscal slippage remain key internal risks. (Note: Although some analysts forecast the ANC-DA coalition will collapse before 2029, our baseline scenario assumes it will remain intact). On the fiscal front, South Africa faces a narrow path. The National Treasury maintains fiscal consolidation, with the budget deficit projected to narrow gradually from 4.7% of GDP toward 2.9% by FY2028/29, supported by strong revenue collection while downside risks remain from slower growth due to high interest rates and global financial volatility.

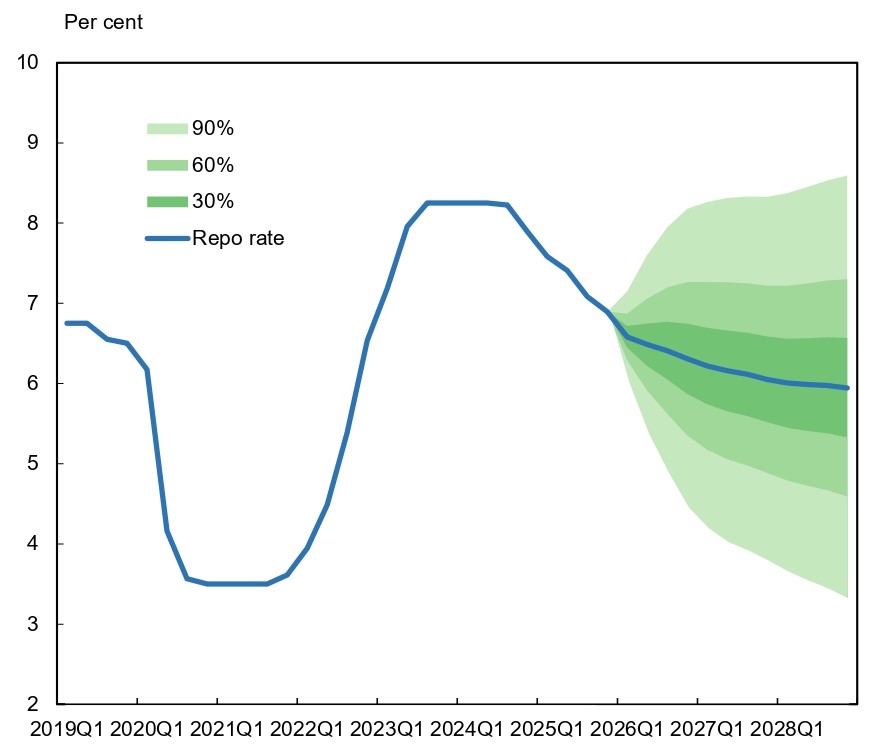

Figure 3: SARB Interest Rate Forecast (%), 2019 – 2028

Source: SARB Forecast Report

Turkiye

Annual inflation in Turkiye slightly edged up to 32.6% in May due to rising housing and energy costs as sticky inflation remains the central challenge. Geopolitical risks, supply‑side constraints and energy prices volatility continue to exert pressure on the inflation outlook causing disinflation process to go slow and uneven.

The Central Bank of Turkiye (CBRT) hiked its end-year inflation target to 26% for 2026, 15% for 2027 and 9% for 2028 in its second Inflation Report of 2026 published on May 14 due to these risks. We think inflation is likely to remain above the CBRT’s upper forecast band by year-end. Our average inflation forecast for 2026 has increased to 31.3% when compared with 28.4% in March outlook. Our updated forecast for average CPI is at 25.6% in 2027. We think inflation will continue to remain sticky, requiring tight monetary conditions for longer. We envisage it will be difficult to grind sticky inflation from 30%s to 20%s rapidly, taking into account that persistent core services inflation, combined with the secondary impacts of Q2 oil and fertilizer price hikes, will require real interest rates to remain elevated for some time.

We envisage the recent resolution to the Iran conflict will provide significant economic relief to Turkiye, primarily by easing heavy energy-import bill and relieving fertilizer costs (and food inflation). Under a baseline scenario where global oil prices soften toward the USD 70–90 per barrel range, we assess the domestic inflation will start to cool off moderately late Q3/Q4, but gradually.

Investor confidence has recently weakened due to regulatory unpredictability and alleged judicial pressure on the opposition - headlined by the continued imprisonment of opposition’s presidential candidate Ekrem Imamoglu. This fragile political framework coupled with concerns on reserve adequacy and FX interventions have driven up risk premiums and constrained capital inflows in H1. (Turkiye's 5-year CDS spread spiked to 327 basis points in April as CBRT intervened in the foreign exchange market to defend TRY against balance-of-payments and energy-import pressures). The political tensions culminated in late May 2026, when a regional court in Ankara annulled the Republican People’s Party’s (CHP) 2023 leadership congress. The ruling shocked the markets by removing elected chairman Ozgur Ozel and reinstating former leader Kemal Kilicdaroglu, triggering an immediate 5% plunge in the Istanbul stock exchange and a 2% drop in TRY.

Despite inflationary risks and political fluctuations, CBRT held the key rate stable at 37% during the MPC meeting on June 11. We expect the CBRT will likely begin considering modest interest rate cuts in Q4 - but with caution- once these secondary inflationary effects of Iran conflict are alleviated. Our end-year key rate prediction for 2026 has increased to 35% from 32% in the March outlook due to inflationary pressures and we foresee CBRT will likely accelerate cuts in 2027.

It is worth mentioning that parliamentary elections in Turkiye are scheduled to occur no later than May 14, 2028, alongside presidential elections could affect CBRT’s rate decisions. (Note: We expect the elections to be held in October/November 2027, earlier than the scheduled time. This timing is critical, as an early election called by Parliament is the only constitutional path for President Erdogan to seek another term). The CBRT’s medium-term trajectory could face structural shifts if President Erdogan pressures for a more aggressive monetary easing cycle in 2027 to stimulate growth. Such a push would fundamentally disrupt the CBRT’s plans for 2027 and data-driven disinflation path. (Note: This risk is underscored by the Erdogan’s recent statement, in which he urged that interest rates be reduced as soon as possible to alleviate funding constraints).

Figure 4: CPI, Core Inflation (YoY, % Change) and Policy Rate (%), January 2015 – September 2026

Source: Continuum Economics

As the weight of high interest rates and inflation continue to dominate the growth outlook, the Turkish economy expanded by a mere 2.5% y/y in Q1 supported by consumption and services while industry remained under pressure from weak external demand and supply disruptions. (Note: Industrial production has faced pressure in Q2 due to Iran conflict, with the manufacturing PMI hovering just below the 50 expansion threshold). A deteriorating external balance and domestic challenges will likely limit room for fiscal and monetary support in H2, capping our 2026 GDP growth forecast at 2.8%. We foresee growth to stand at 3.5% in 2027, driven by interest rate cuts and pre-election fiscal stimulus. We think a decline in the inflation rate in 2027 and beyond could boost confidence coupled with accelerated structural reforms, and stable global conditions could lift growth back toward potential of around 4% after 2027/28.

On the other side of the coin, tight monetary and income policies, along with any unexpected resurgence of inflation and accelerated TRY depreciation could derail the recovery and reignite macro instability. There is still a downside risk that growth can be lower than expected, particularly considering all the tightening measures in place. Turkiye’s external financing needs, growing current account deficit, elevated external debt, and volatile capital flows continue to pose risks.

Figure 5: GDP Growth (%, YoY), Q1 2000 – Q1 2026

Source: Continuum Economics

Russia

The Russian economy continues to navigate structural challenges, ranging from persistent sanctions and supply chain fragmentation to demographic decline and fiscal volatility. The overall environment for doing business in and with Russia remains unfavorable, while the conflict in Ukraine is the primary determinant of the economic outlook.

On the inflation front, CPI moderately down to 5.3% y/y in May owing to the lagged impacts of previous tight monetary policy and the relatively resilient RUB. This was the lowest reading since August 2023 despite inflation remained above the CBR’s midterm target of 4%. This trend was supported by improving inflation expectations; recent data showed household expectations edged down to 12.4% in June from 13% in May.

Though CBR is projecting that inflation returns to the 4.5-5.5% target in 2026, we think reaching this target will not be easy due to continued military spending, labor shortages, and supply-chain disruptions coupled with adverse effects of the value-added tax (VAT) increase and excise taxes. Our CPI forecasts stand at 5.7% and 5.0% in 2026 and 2027 as we anticipate inflation will continue to soften moderately as previous tight monetary policy will continue to affect bank lending and private consumption, but slowly.

Backed by a softening inflation, CBR continues its easing cycle and reduced the key rate to 14.25% per annum on June 19 citing global inflationary risks. CBR said in its written MPC statement that pro-inflationary risks are supported by the external backdrop of higher energy prices due to the war in the Middle East, higher energy prices domestically as refineries are targeted by Ukraine, and higher inflation expectations as wage growth outpaces productivity growth. We think CBR will likely resume cutting rates (moderately) in Q4 and 2027 if the inflation trajectory allows and inflation expectations converge towards CBR’s forecasts.

Our end-year key rate forecast is at 13.5% and 10.5% for 2026 and 2027, respectively. Russia will have to keep rates high as the country need higher real yields. (Note: As an alternative scenario, we think a faster CBR easing cycle is possible in 2027, if a full scale peace deal is signed in Ukraine relieving the Russian economy, and President Putin could request a domestic demand boost as military spending slows).

The inflation trajectory and rate decisions will heavily depend on how peace negotiations in Ukraine will proceed in H2 2026/2027. An unexpected peace deal in H2 2026/H1 2027 could help Russian economy to feel relief since military spending growth will slow, average headline inflation will soften, and fiscal pressure will ease, particularly if sanctions will be lifted.

The probability of the conflict in Ukraine continuing throughout 2026 remains at 70% and there is a 30% probability to a Russia‑friendly peace deal, likely in late 2027. First, the battlefield remains in a state of grinding attrition, with limited tactical breakthroughs and significant unresolved issues, most notably the status of the eastern Donbas and territories in the eastern oblasts. Both sides are exhausted because of man loss and economic pressures; and the Russia’s summer offensive has effectively slowed down making Russian territorial gains in May were nearly net-zero.

We foresee Putin will be eager to finalize an agreement before the end of Trump’s term in January 2029. On the Ukrainian front, President Zelenskyy recently noted they also want to force Russia into viable peace negotiations before winter. (Note: We anticipate that as the Iran conflict dissipates, U.S. president Trump’s focus will likely shift first toward Cuba. However, a return of U.S. attention to Ukraine in Q4 2026/Q1 2027 could reaccelerate stagnant peace talks but this would first require a compromise by Putin).

We continue to think Ukraine remains in a weaker negotiating place and, at some point Ukraine will have to admit giving up some land to Russia. Under any Russia-friendly peace deal framework, the deal would likely involve Russia annexing parts of the four occupied Ukrainian oblasts while securing a commitment that Ukraine will not join NATO or host foreign troops.

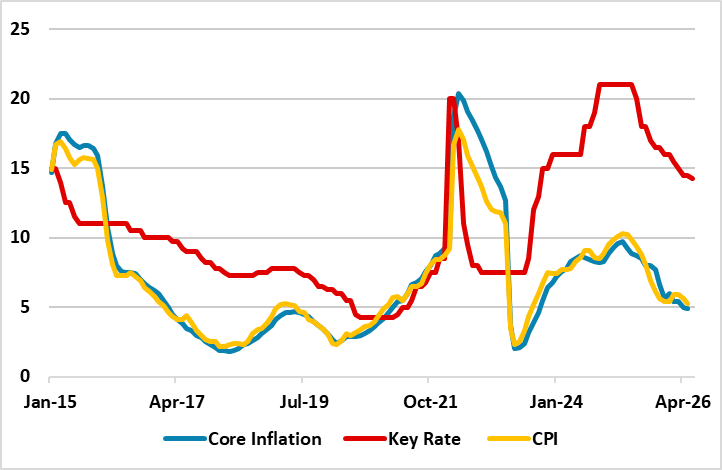

Figure 6: CPI, Core Inflation (YoY, % Change) and Policy Rate (%), January 2015 – June 2026

Source: Continuum Economics

The primary driver of Russian GDP growth remains a surge in military spending, bolstered by increased social support outlays, rising wages, and strong fiscal stimulus. However, the economy faces headwinds from higher policy rates, ongoing sanctions, supply-side constraints, and an anticipated drop in crude oil prices as the Iran conflict dissipates. Furthermore, capacity utilization has hit multi-year highs, and severe labor shortages driven by troop call-ups are unlikely to ease in the near term.

We expect GDP growth of 0.4% in 2026, rising to 1.1% in 2027, as the previous tightening cycle is still feeding through and easing effects will only come through fully into H2 2027/2028. We think the growth will remain limited in 2026 mainly due to expected fall in oil prices in H2 coupled with adverse impacts of sanctions. The key for Russian economic growth in the next few years will be if a deal in Ukraine will be sealed, when (and which) sanctions will be lifted.