The Whig History of late-90s Fed Policy

Bessent's approving 1997-Fed anecdote raises eyebrows and debate about its implications

It's important to recall how that era played out however: a sequence of many global events, not a grand vision

Politics, at its heart, is storytelling. And so, let's be honest, are markets. And even central-bank policy. The tendency to rewrite, rose-tint and narrativise what was, in truth, chaotic real-time history, is human nature, but also guided by agenda. And this is nowhere more true than in the retrospective mythologising of Fed policy into and out of the noughties.

Why this comes up is the arresting and seemingly highly-loaded recent speech and subsequent interview from US Treasury Secretary Bessent. There, unprompted (other than by the timing of Greenspan's passing), Bessent pointed approvingly to 1997. According to the story, the Fed hiked once then, "to dab the brake", before entering an easing cycle that heralded the "longest sustained growth period in history". Thanks, the anecdote goes, to Greenspan's apparent foresight on productivity and non-inflationary growth.

Before addressing the potential political and informational significance of the musing, it is worth stepping back to remember the unvarnished version of lived events. The Fed hiked in 1997 to the much higher rate of 5.5%, before actually being forced into a sustained pause by the Asia crisis. The subsequent renewed easing was then not part of a grand strategy, but instead again driven by events, and the "put" reaction to the LTCM crisis. Subsequent policy then remained over-accommodative, fuelling the build and bust through the dot-com and year-2000 peak. And from there the story actually moves on to the dramatic launch of globalisation, the end of the cold war, China driving both goods prices and the huge recycling into major bonds and wider assets. A gilded rather than necessarily golden age of Fed policy through the "conundrum years". And the 2008 Great Financial Crisis that (inevitably?) followed.

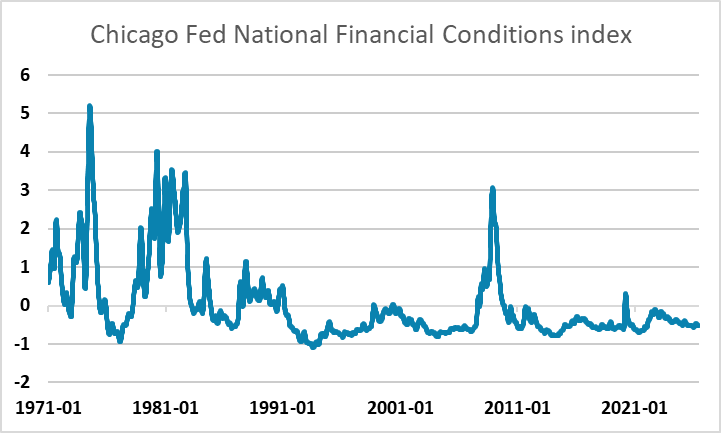

Source: Datastream/Chicago Fed

The sanitised parallel is tempting and perhaps self-serving, but treating it as a model rather than a largely reactive sequence of events creates strategy out of tactics. The realities of the current world are rather different. Globalisation is frictioned, supply shocks are seemingly a constant stream of one-offs in sequence and frequently systemic rather than truly exogenous, fixed income is in a different regime, and Fed policy faces the same real-time dilemmas rather than a post-fact roadmap.

As far as markets are concerned though, in this era of even-more-politics-directed reaction functions, the market's main interest is the rather more prosaic one: is Bessent giving a "permission" and a message (ironically, despite sharing Warsh's dislike of forward guidance), and speaking about a thought that was somehow triggered by breakfast with the Fed chair? Who knows. What it may tend to do, however, is reinforce the seed of an idea in the market that a "dab" is not taboo (very near-term data dependent), but that this would be a Greenspan dab, before completing the easing cycle quite soon after once Iran is fully cleared. That can further shape the market's pricing of the Fed curve. In truth, the history of the AI era, told from the 2040s, will no doubt itself skirt over "events", as the trajectory of Fed policy and the economy through the clashing supply and demand, and financial leverage, of AI plays out.