U.S. Outlook: Consumers Looking Vulnerable

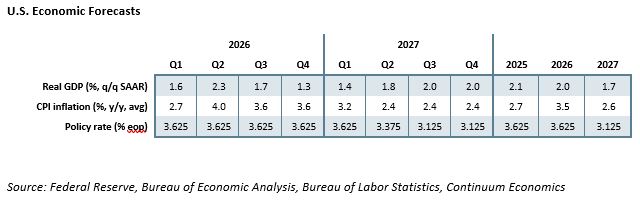

• The US economy is showing resilience with strength in investment offsetting a gradual slowing in consumption, though consumer spending, which is running well ahead of real disposable income, looks set to slow further. This is likely to see the economy slow in the second half of 2026 even with continued strength in business investment, which is narrowly based. We expect annualized GDP growth to slow below 2.0% in the second half of the year, bringing a modest increase in unemployment, before returning to a 2.0% pace in the second half of 2027 as inflation falls to near the 2.0% target. Inflation is currently elevated and we expect core PCE prices to remain above 3.0% on a yr/yr basis through 2026, before slowing to finish 2027 at 2.2%, with annualized growth in the second half of the year consistent with the 2.0% target. Uncertainty remains high, even if somewhat reduced in the Middle East. Renegotiation of the USMCA trade agreement is a significant near term risk. Midterm elections in November are likely to see the Democrats taking control of the House, which will restrain President Trump’s scope to act on fiscal policy, though the Senate looks too close to call.

• Incoming FOMC Chairman Kevin Warsh has committed himself to the 2.0% inflation target but has given few clear signals on policy. Elevated core inflation means easing is now unlikely in 2026 though tightening will probably require a further acceleration in inflationary pressures, which the Middle East deal makes less likely. We believe that by Q2 2027 inflation will be looking on track to return to target, and the Fed will deliver 25bps easings in both Q2 and Q3 of 2027, taking the Fed Funds target range to a neutral 3.0-3.25%. Warsh may try to balance this by reducing the size of the balance sheet but his ability to do so significantly may prove limited.

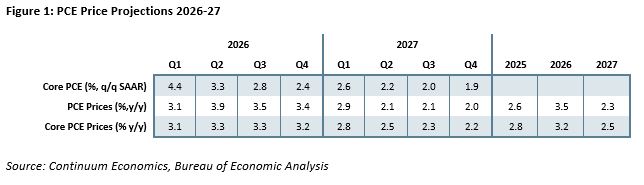

Forecast changes: The energy shock has been stronger than we assumed in March but looks set to gradually fade. We have revised our GDP forecasts only moderately lower, 2026 to 2.0% from 2.2% and 2027 to 1.7% from 1.8%. We have however revised our inflation forecasts higher, with CPI now seen at 3.5% versus 3.2% in 2026 with 2027 now 2.6% rather than 2.2%. For PCE prices, we have revised 2026 to 3.5% from 3.2% and 2027 to 2.3% from 2.0%, with the 2026 core rate at 3.2% from 2.9% and 2027’s at 2.5% from 2.2%. Our forecast for core PCE prices in Q4 2027 is however unrevised at 2.2% yr/yr. We now expect the Fed to leave rates unchanged through 2026, contrasting our March view for two 25bps easings. We now expect two 25bps easings in 2027. While this contrasts a March view for no change our view that the Fed Funds target range will end 2027 at 3.0%-3.25% is unchanged from March.

Slowing consumption to outweigh continued strength in investment

The U.S. economy has a mixed picture, with strong business investment fueling respectable GDP growth at present but consumer spending looking vulnerable to a slowdown given weakness in real disposable income. Recent data has seen perceived risks of labor market weakness fading but worries about inflation picking up, and not only in energy, where uncertainty remains high but may have peaked given the Middle East peace deal. We are likely to see a moderate slowing in GDP and inflation coming off the highs, though with core inflation still too high we now do not expect easing until 2027. Renewed conflict in the Middle East would raise stagflation risks, though we expect Fed tightening to be modest even in this scenario, as downside risks to employment would also pick up.

Q1 GDP saw only a modest 1.6% annualized increase despite a lift from government after the Q4 2025 shutdown. Details were mixed with consumer spending slowing to a four-quarter low of 1.4% but business investment at an 11-quarter high of 10.1%. While the contrast was less stark on a yr/yr basis, with consumer spending at 2.3%, business investment at 5.7% and GDP at 2.6%, the contrast between consumer weakness and business investment strength is likely to become increasingly evident, with slowing in consumer spending, which makes up almost 70% of GDP, to be of greater significance. Consumer spending, while slowing, has been running increasingly ahead of real disposable income, which was down by 1.1% yr/yr in April, leaving the savings ratio at 2.6%. Only one month of the post-Covid rebound, June 2022, saw a lower savings ratio than this. Consumers have been spending beyond their means, sustaining spending in the hope that the gasoline price surge will be brief. This suggests limited upside to consumer spending from a sustained resolution of the Middle East conflict, and significant downside without one. Some may feel that recent signs of labor market resilience will support consumer spending, but we believe the strong payroll growth of the three months to May will be difficult to sustain, and that unemployment will see a modest increase in the second half of the year. Wage growth is gradually slowing and likely to underperform inflation in 2026 as a whole, though moderate real wage growth is likely to resume in 2027. We expect consumer spending to grow at an annualized pace below 1.0% in the second half of 2026 before moving back to near 2.0% in late 2027.

Business investment strength is being led by AI, and little slowing is likely there, though the 10.1% annualized increase of Q1 needs to be seen alongside gains of 2.4% in Q4 and 3.2% in Q3 of 2025. Outside AI-related spending the business investment picture is subdued, with structures having seen five straight negative quarters. We expect business investment to increase by a pace averaging a little above 4% through the remaining quarters of 2026 and 2027, which would be over twice what we expect from GDP. Trends in the housing sector are looking fairly flat at the moment but we expect this to turn marginally negative as consumer income is squeezed and scope for Fed easing remains limited. Government will see a lift from defense as weapon stocks are rebuilt but will remain subdued elsewhere, with the State and Local sector likely to see a modest slowing. For net exports we expect a modest negative, with the correction from the pre-tariff surge in the trade deficit now looking done, which will probably outweigh a modest positive contribution from inventories. Early signals for Q2 GDP are positive and while some loss of momentum is likely as the quarter progresses, the World Cup will provide temporary support. However, after a modest acceleration in Q2, we expect annualized GDP growth to slow to a low of 1.3% in Q4 2026 before picking up to 2.0% in the second half of 2027. For the years as a whole we expect gains of 2.0% in 2026 and 1.7% in 2027, but on a Q4/Q4 basis 2027 at 1.8% will be slightly faster than 2026 at 1.7%.

Resilient inflation leaves the Warsh Fed limited scope to ease

The inflation picture is not all bad. While the labor market remains far from weak it is generating little inflationary pressure, with wage growth slowing marginally even as inflation has accelerated. Unit labor costs, supported by healthy productivity, rose by only 0.5% yr/yr in Q1 though strength in non-labor costs has the implicit deflator of the productivity and costs report at a three-year high of 3.5%. The tariff impact has probably peaked, even if President Trump finds some measures to replace the tariffs which the Supreme Court ruled against. The oil price shock is likely to have peaked, even if its unwind will be gradual and incomplete. However, the Fed should not dismiss the inflation problem as down only to temporary factors. April’s core PCE price index of 3.3% yr/yr is the highest since November 2023, unusually accelerating ahead of core CPI, though even the latter at 2.9% yr/yr in May is the highest since September 2025. The strength in AI investment is generating inflationary pressures in IT and electricity, and this suggests hopes that this will spur a surge in productivity that reduces inflation look premature at best. We expect yr/yr core PCE prices to remain above 3.0% through 2026 though annualized rates are likely to slip below 3.0% in the second half of the year. 2027 is likely to see a move closer to the 2.0% target, ending the year at 2.2%, with the annualized pace reaching 2.0% in Q3 2027. For 2027 as a whole, we expect core PCE prices to average 2.5%, down from 3.2% in 2026.

Incoming Chair Kevin Warsh has committed the FOMC to reaching the 2.0% target but has avoided giving forward guidance on policy. Many officials have stated that they view strong investment as likely to raise the neutral rate, and concern over the underlying strength of inflation is rising at the Fed, while worries over labor market weakness have faded since 2025. Easing now looks unlikely this year even if the peace deal in the Middle East holds. The latest FOMC dots show a fairly even split between those advocating tightening this year and those seeing policy kept on hold, though we believe the majority of voters are in the latter camp, including Warsh, though he declined to provide a dot. Many of the hawkish dots are likely to come from non-voting district presidents. We thus do not expect any tightening this year. That could change if energy prices take a fresh leap higher, or core PCE data shows no sign of slowing in the second half of the year, but we would expect no more than 50bps of tightening even then. If core PCE prices start looking consistent with a move to target, easing may resume, and our core PCE price forecasts suggest that can happen in Q2 2027. The Fed is likely to want to make sure that Q1 2027 does not repeat the strength of Q1 2026 before moving. We expect 25bps moves in Q2 and Q3 of 2027, which would take the Fed Funds target to a 3.0-3.25% range, which the Fed currently sees as neutral. It is more likely that the Fed will do less than this than more, with our forecast probably the maximum that can be done while maintaining credibility, which is what we expect Warsh to push for. Warsh may wish to reduce the balance sheet to compensate for a dovish lean on rates, but his ability to do so may be limited, both by the views of others on the FOMC and the potential for cuts in the balance sheet to create tensions in money markets, as was the case in 2019.

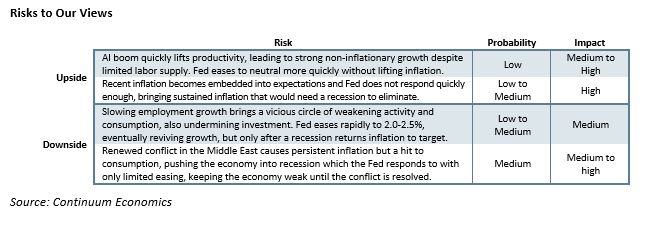

Plenty of risks, including the midterm elections

Risks to our growth view are significant on both sides, but fairly balanced. Business investment could prove even stronger than we expect, though still probably narrowly based. If recent labor market strength persists and energy prices fall significantly consumer spending may slow less than we expect, though a significant acceleration will remain unlikely. However should increasing consumer weakness feed through into the labor market, a vicious circle could develop if the Fed is unwilling to ease, and as is also likely, scope for fiscal stimulus is limited by the midterm elections. The downside risks on a revival of conflict in the Middle East would be substantial.

On inflation the risks are skewed to the upside of our view. Prospects of underlying inflation gradually moving close to target as temporary factors drop out are reasonable, but a move below target does not look likely in the next few years outside the headline once recent energy price strength drops out of the year ago comparison. Core inflation remaining above target is an increasing risk if inflation expectations move higher. It is unclear if this Fed will act quickly and decisively enough if inflation continues to disappoint.

Significant risks remain in the Middle East, while trade policy is another near term risk, with the USMCA trade agreement due for renewal. There the negotiations may drag on for some time, with a dramatic escalation of tariffs a low but not minimal risk. Midterm elections in November may end up having a limited impact on the markets, assuming the Democrats, as looks likely, take control of the House, and thus leave Trump with limited scope to act on fiscal policy. The Senate is a much closer call. Democrats need only to take control of the House to contain Trump on fiscal policy, though if they manage the Senate too Trump will struggle to get his appointments confirmed. The Democrats need to gain four seats, and five if they do not want to rely on Pennsylvania’s John Fetterman who often votes with Republicans. A Democratic gain in North Carolina looks likely, and Alaska and Maine are leaning to the Democrats, though the Democratic candidate in the latter is a controversial one. Ohio, Texas and Iowa are also possible Democratic pick-ups, though they are also defending close seats in Michigan, Georgia and New Hampshire. If control of the Senate is at stake, there could be legal challenges if the results in some of these states are close.