U.S. Private Credit: One To Watch Rather than Systemic Issue

While the U.S. private credit sector could face further problems in 2026/27 (due to the lagged impact of the end of ultra-low rates in 2021-23), this appears to be a sectoral issue. U.S. banks equity capital and funding are robust enough to weather a further deterioration, though some corporates could see restrained credit supply with the adjustment in private credit and thus a select economic impact could be seen.

Could the U.S. private credit problems become a big financial stability issue?

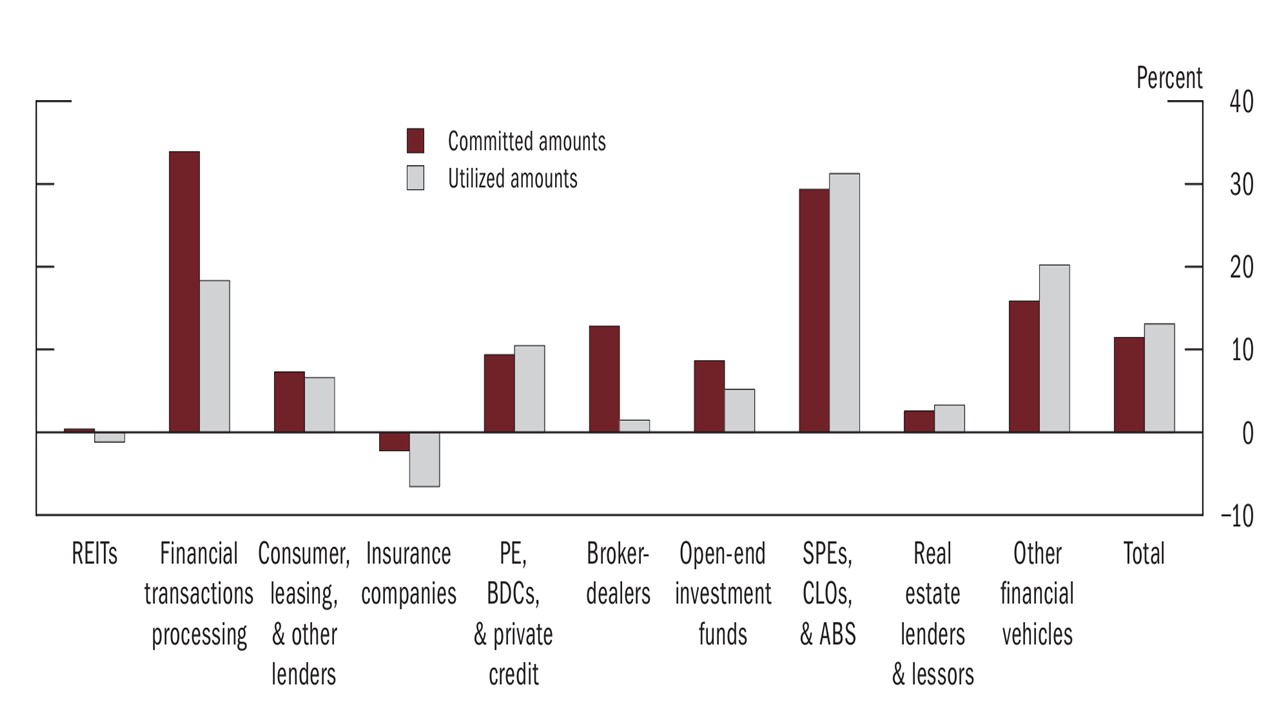

Figure 1: Bank credit growth between 2024:Q2 and 2025:Q2 (%)

Source: Federal Reserve Financial Stability Report November 2025

Private Credit in the U.S. has been in the spotlight, but some context is worthwhile

· Selection of problems. Private credit funds have been restricting withdrawals given a deterioration in sentiment towards the sector, after a number of failures in the U.S. (e.g. First Brand/Tricolour). Some of the problem has been overleverage of mediocre companies, but in Tricolour case also involves fraud allegations. Some of the publicity is due to retail investors having become involved in the private credit party.

· Contagion. Due to the opaque nature of some funds and also infrequent mark to market, the sentiment shift is raising question about good as well as average private credit funds. Separately, private equity has had its own difficulties, with the 2021-23 shift away from ultra-low interest rates also changing long-term profitability and ability to exit from holdings. Private credit and equity will likely have a hangover for the rest of 2026 and the tension could increase in private credit, unless a surprise large rate reduction is delivered. ECB and BOE financial stability report are also monitoring developments as well. The situation could deteriorate significantly if the U.S. sees a recession, but this is a 20% probability scenario in the next 12-24 months.

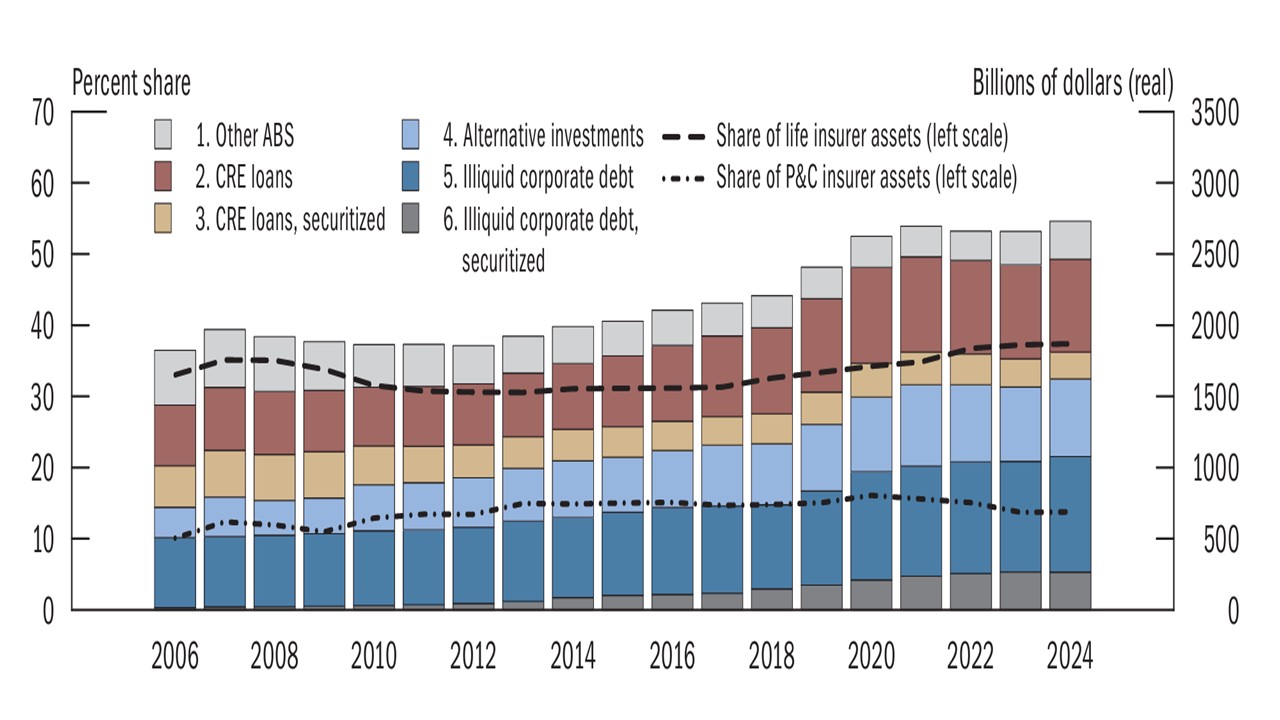

· Not systemic. While banks have increased lending to private credit, bank stress tests show that the banking system is robust in terms of equity capital and liquidity and a sectoral issue (outside of the recession scenario) should not be a major issue for the banking system or the economy. The November 2025 Federal Reserve financial stability report shows a broad range of sectors that the banking system is working with (Figure 1). However, it could lead banks to be more cautious in new lending to private credit, which could have an impact on some U.S. corporates that are dependent on private credit. One final point is that the Fed do maintain a spotlight of concern on high U.S. life insurance company leverage and the large share of illiquid assets (Figure 2) including private credit.

Figure 2: U.S. Life insurers continued to hold a significant share of illiquid assets (% and USD Blns)

Source: Federal Reserve Financial Stability Report November 2025