Japan’s GPIF: Can it turn back the clock on the yen?

· The GPIF story is not that one public fund can singlehandedly ‘rescue the yen’. The question is more whether Japan can use one of the central institutions that helped drive the Abenomics flow-of-funds regime revolution to change the narrative, re-influence domestic allocation and sentiment.

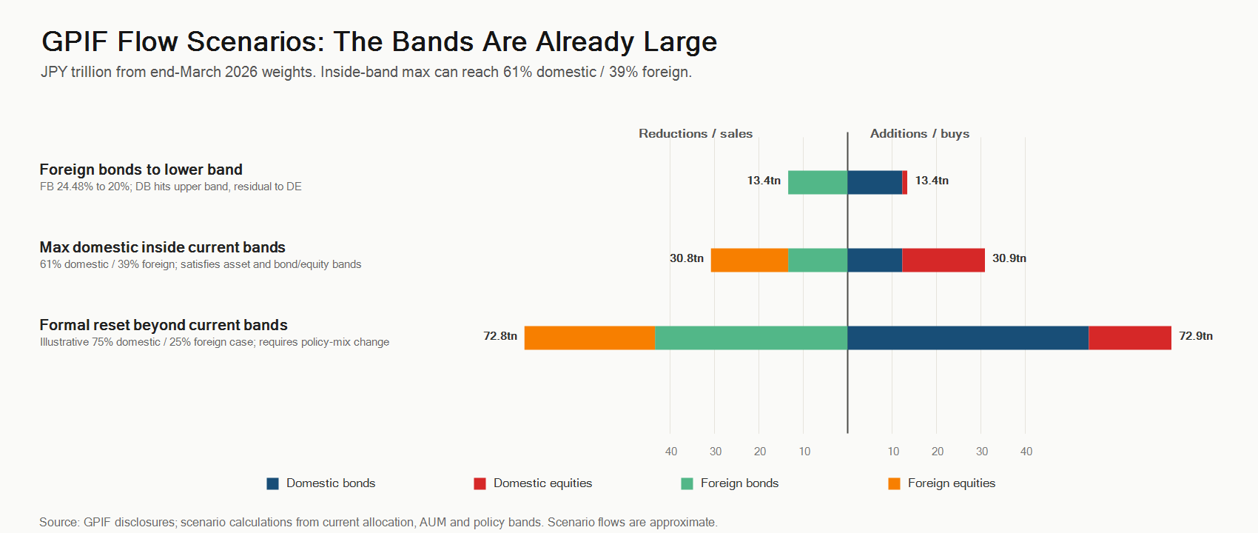

· The direct numbers are not trivial though. GPIF's current bands currently already allow a move from roughly 51% domestic, 49% foreign today to about 61% domestic, 39% foreign without a formal target reset: around JPY 30.8tn, or just under USD200bn, of foreign-to-domestic room.

· Within that, the pure domestic-bond channel is about JPY 12.3tn. Recent rebalancing - rather than re-allocation - has already generated JPY 32.5tn of domestic-bond buying over the FY2023-FY2025 period though, if partly driven by the dynamics Japan wants to arrest.

· The flow only becomes more fundamentally macro and market relevant if it does two things: creates a domestic institutional ‘multiplier’, and mitigates the market script on reinforcing outflows and global carry.

The Abenomics legacy

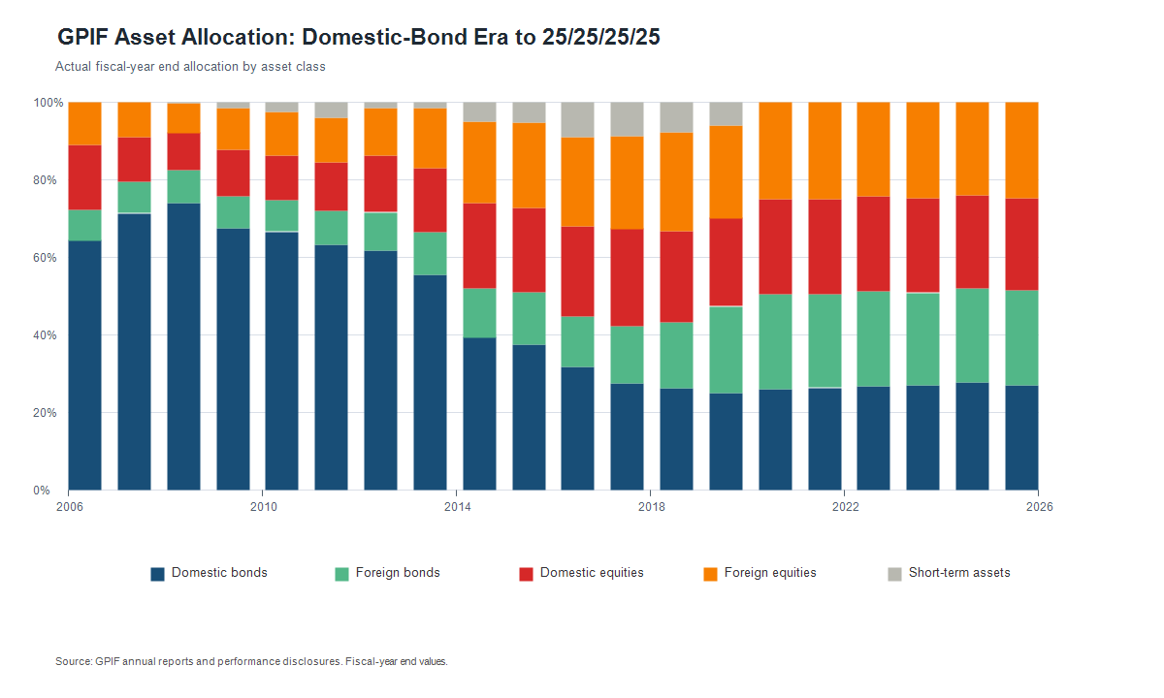

Behind that arithmetic sits the Abenomics legacy. The 2014-2020 GPIF shift was part of an orchestration and unleashing of a broader decade long flow-of-funds regime break: GPIF and other institutions were directed into equities, foreign assets and portfolio risk while the BoJ absorbed the domestic-bond burden through QE and yield-curve control. The 2014 reset pushed GPIF away from the old quasi-governmental domestic-bond-heavy portfolio and toward equities and foreign assets. The 2020 move to 25/25/25/25 allocation completed the reset. The old, deeply embedded conservative domestic-bond-heavy equilibrium was broken in the process as the benchmarking and wider window guidance effect spilt out.

Figure 1: Shift in asset allocation as a regime change

Source: GPIF annual reports and performance disclosures, CE

That regime reset worked, perhaps too well, as some of the resulting constraints and excess momentum now featuring come back to bite. The BoJ is now unwinding an extreme stock of purchases, inflation expectations have partly shifted, domestic yields are no longer pinned, and the foreign-asset allocation for domestic institutions psychology created in the Abenomics era has become part of the yen's self-reinforcing weakness. Intervention can chop at the exchange-rate move but it cannot easily reverse the regime unless the authorities can also alter the expected direction of domestic balance-sheet and, with it, global FX flows. Hence, the renewed interest in getting the GPIF genie back in the bottle.

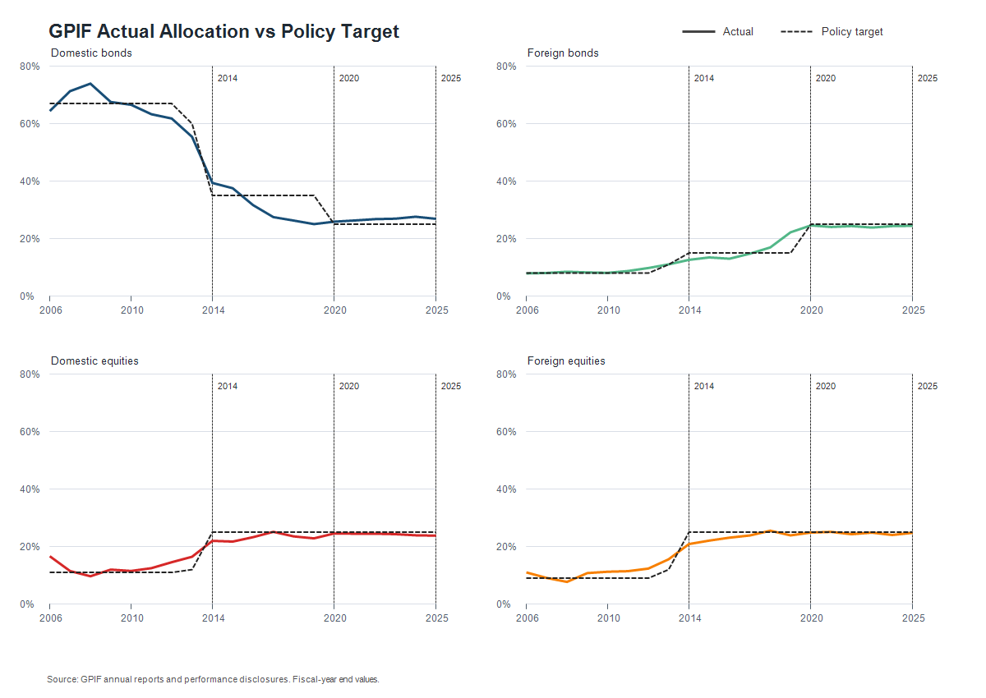

Figure 2: Asset allocations vs the central allocation target over 2014-2020-present

Source: GPIF annual reports and performance disclosures, CE

The problem is that Abenomics also changed the institutional language. The old fudge between public-policy ‘guidance’ and fiduciary purpose is harder to sustain after allocations have normalised and diversification has been legitimised as the beneficiary-maximising governance outcome. The latest five-year framework has also only just been approved moreover, making a full reversal procedurally and intellectually difficult. (Ironically, the 5th framework tightened the bands by 1-2pp across the classes vs the 4th, something the government might be regretting).

The current, latest framework nonetheless still leaves meaningful room for domestic tilts without formally rewriting the policy mix, provided the move can be framed as risk management rather than idiosyncratic.

Rebalancing is already a notable flow

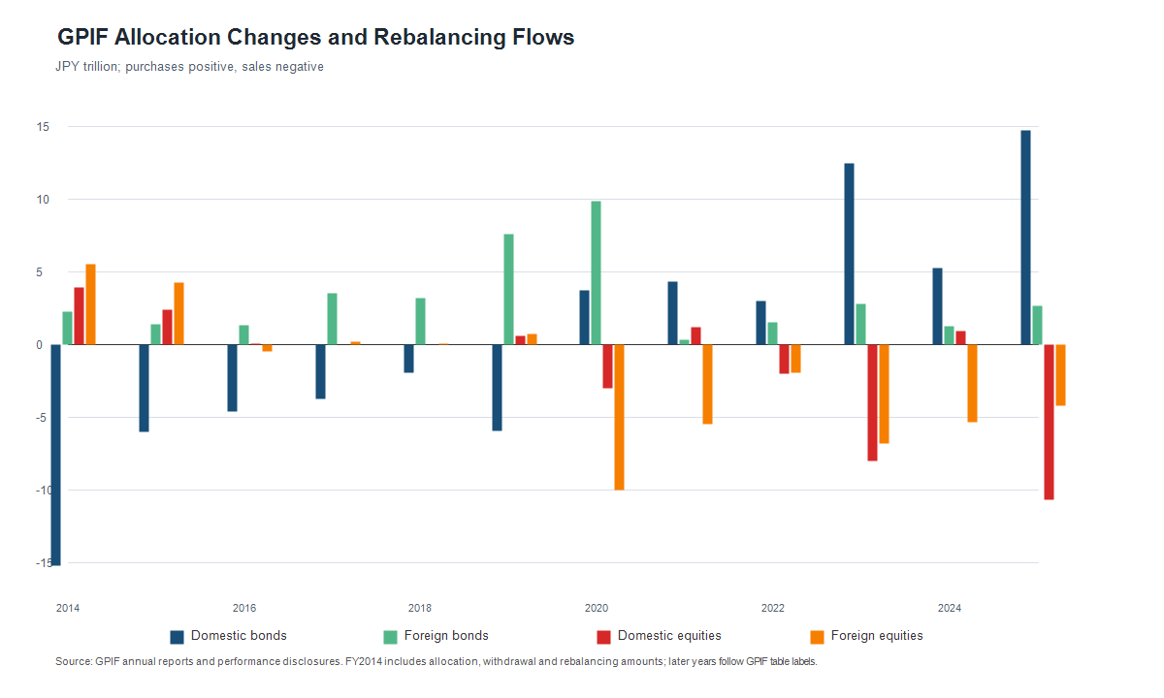

Mechanically, it is worth just noting in passing that GPIF's existing framework already creates large domestic-bond flows when the reflation/carry side of the portfolio is in flight, via more standard rebalancing rather than re-allocation adjustments.

Recent disclosed allocation/rebalancing flows show the scale: over FY2023-FY2025, GPIF bought about JPY 32.5tn of domestic bonds and JPY 6.8tn of foreign bonds, while selling JPY 17.7tn of domestic equities and JPY 16.4tn of foreign equities. Weak-yen/reflation trade thus does currently generate some notable offsetting JGB support, albeit not enough to counter the scale of BoJ balance sheet run off (here).

Figure 3: Re-balancing flows have been a JGB cushion, albeit on reflation valuation effects

Source: GPIF annual reports and performance disclosures, CE

Wiggle room is larger than it may seem

Re-allocation in contrast is the new option on the table and even without new formal changes, the current bands are wide enough to be used in semi-strategic way.

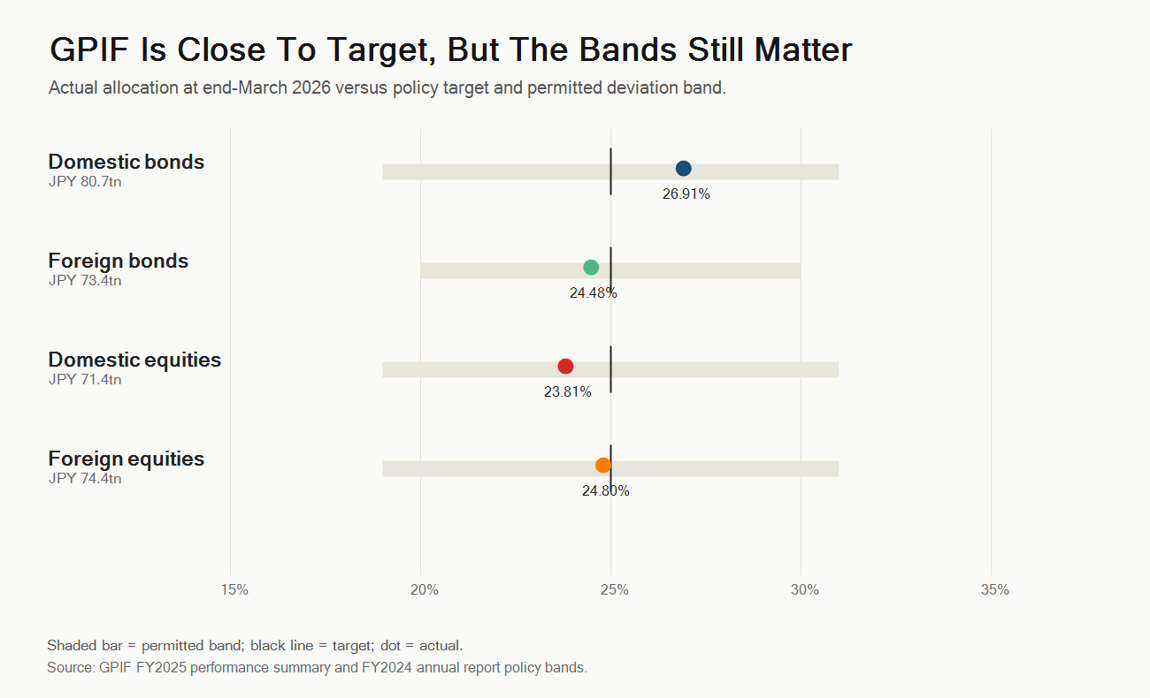

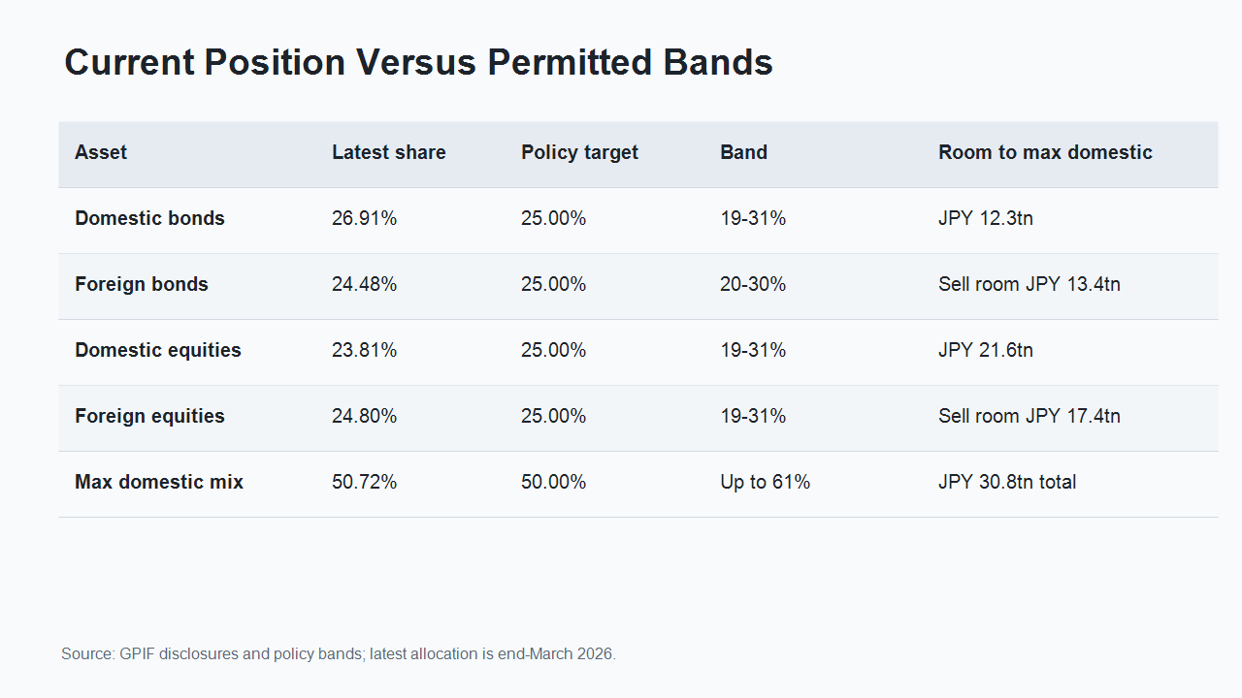

At end-March 2026, GPIF had about JPY 299.8tn of pension reserves managed by GPIF and the Pension Special Account. The actual allocation was domestic bonds 26.91%, foreign bonds 24.48%, domestic equities 23.81% and foreign equities 24.80%. The headline policy mix remains 25/25/25/25, but the deviation bands are wide: domestic bonds +/-6pp, foreign bonds +/-5pp, domestic equities +/-6pp and foreign equities +/-6pp (while also satisfying the aggregate bond/equity constraint).

Figure 4: Current allocations vs allocation +/- bands around core allocation target

Source: GPIF annual reports and performance disclosures, CE

Domestic bonds are already slightly above target, but still have about 4.1pp of room to the upper band, or roughly JPY 12.3tn. Domestic equities have more room: about 7.2pp, or roughly JPY 21.6tn. The headroom is therefore reasonably chunky: about JPY 30.8tn of foreign-to-domestic room (the small gap versus the sum of the domestic upside reflects the tighter constraint on how much foreign bonds and equities can be reduced within band).

GPIF is a slow public balance sheet of course (and managed across a diversified number of external fund managers), not a spot-market intervention. The within-band room is nonetheless large enough to treat as more than symbolic, and large enough to matter if it actually changes the expected direction of domestic institutional capital.

Figure 5: Breakdown of significant wiggle room within existing flexibility

Source: GPIF annual reports and performance disclosures, CE

The constraint is fiduciary language

The bands are wide, but using them directionally still requires a pension-risk story. GPIF is not a Ministry of Finance trading account but sits within the current public pension reserve framework: MHLW objectives, GPIF medium-term plan, and an explicit requirement to secure pension returns with minimum risk for the sole benefit of insureds.

With the FY2025-FY2029 framework just signed off, the immediate route is less likely to be a new target and governance overhaul than a stronger risk interpretation inside the current bands. Indeed, newswire sources seem to confirm as much that re-write is not being considered.

Figure 6: ‘Scenarios’: From flexibility (likely) to illustrative re-write (very unlikely)

Source: GPIF annual reports and performance disclosures, CE

Such a shift could come from formal, agenda-driven MHLW/GPIF risk work, or softer official pressure around the same themes. The more explicit and durable the move, the more it would need to look like a genuine pension-risk reassessment rather than informal window guidance.

The cleanest ‘excuse’ is probably one presented around portfolio risk. The post-2014 foreign allocation has built a larger stock of FX asset exposure against yen liabilities, with large accumulated currency returns at increasingly out of sample and trend divergent yen levels. In fund language, the question is whether the accumulated gain now comes with too much currency value at risk and risk concentration for the point in the cycle, especially after an extraordinary yen divergence and with domestic yields to a degree reset. (Foreign bonds are benchmarked on an unhedged yen basis; yen-hedged foreign bonds are classified with domestic bonds for allocation purposes; and there is no disclosed strategic hedge ratio, as far as aware, for foreign equities).

The 2014 reform made global diversification the legitimate fiduciary answer. Any partial row-back has to credibly suggest that the risk-reward facts have changed.

Market: Flow non-negligible; Multiplier, script break more critical

The direct flow is large enough to matter, but not as a substitute for FX intervention. The within-band maximum is about JPY 30.8tn is a few multiplies larger than recent intervention but slower delivery and also not enough in isolation to dominant global (especially dollar driven) flows.

Market relevance depends on whether the flow is read as the start of a broader balance-sheet turn, akin to 2014 but in more nuanced and less revolutionary fashion, influencing broader domestic institutional position and risk assessments, especially from those that implicitly benchmark to GPIF.

One route then is the domestic institutional multiplier: GPIF does not force life insurers, Japan Post or other balance sheets to follow, but it can change the language and decisions around what counts as prudent allocation.

The other route is a narrative break. A credible public-sector return-home signal could make investors question whether the post-Abenomics flow-of-funds regime is still one-way and thus at least add some two-way sentiment into the one way carry dynamic. The NISA investment vehicle for domestic investors has already created extra flows towards domestic equities. This isn’t a story then that will settle overnight but it is a relevant theme to monitor as it plays out over the next few months.