Australia Outlook: Steady

Australian CPI showed signs of moderation in recent read. It should be enough to persuade the RBA their previous hike to be enough.

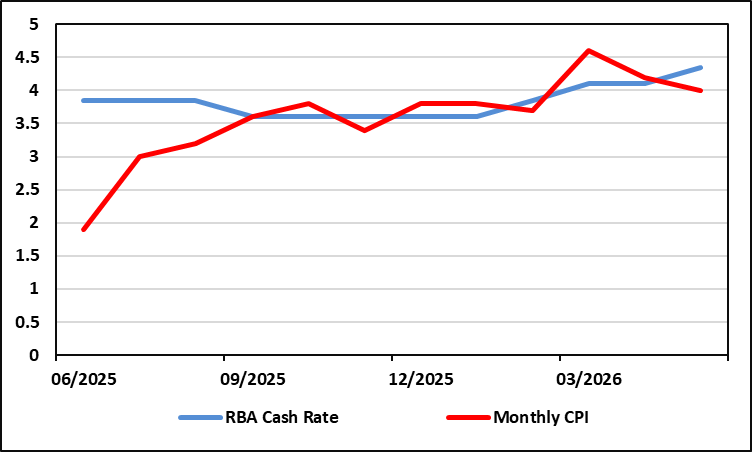

Figure: Australia CPI, Policy Rate (%)

The RBA hike rates to 4.35% in May with a majority 8–1 vote. The consecutive hike is driven by sticky underlying inflation and the persistent energy cost pressure. Followed by the June meeting when the Board unanimously held the rate steady and acknowledged tighter financial conditions while maintaining a "hawkish" bias. Headline CPI has begun to show moderation at 4.0% y/y in May and should keep the RBA comfortable at current cash rate. However, the trimmed mean CPI accelerated to 3.6%. This stickiness was heavily exacerbated by resilient housing costs and a massive spike in electricity prices following the expiration of government energy rebates, signaling that underlying inflation is deeply entrenched. Such should see the RBA on high alert as we forecast 2026 CPI to remain above target range at 3.5% y/y before moderating to 1.8% in 2027.

The domestic demand is bearing the weight of negative real wages and restrictive financial condition. Q1 2026 GDP slowed to a sluggish 0.3% q/q (2.5% y/y). Consumers are feeling the acute pinch of unavoidable utility costs, leading to entirely flat discretionary spending. Consequently, the household saving ratio plummeted to 6.2% as households rapidly drew down their financial buffers to cope with the cost of living, reflecting a significantly weakened consumer base. We have revised our 2026 GDP lower to 2.0%.

Investment has emerged as the lone pillar preventing a deeper economic contraction, specifically within the digital and green energy sectors. Business investment surged 5.7% in the first quarter, driven almost entirely by a massive wave of capital expenditure in AI-ready data centers, machinery, and equipment. This structural shift toward digital infrastructure is continually being paired with significant public investment in renewable energy zones and water infrastructure, cementing capital expenditure as the primary engine of current domestic growth.

Looking forward, the trade outlook remains volatile due to ongoing geopolitical tensions and physical supply chain disruptions. While LNG prices have been erratic alongside oil, net exports dragged GDP down by 0.8 percentage points in Q1 2026. This was primarily hampered by extreme weather disrupting coal and iron ore shipments, rather than a fundamental drop in Southeast Asian or Indian demand. This dynamic continues to create a complex environment, presenting both lucrative opportunities for exporters when physical constraints clear and sustained inflationary bane for Australian residents.

The RBA will maintain highly vigilant following their June meeting, noting that the labor market remains relatively tight with the unemployment rate at 4.4% in May. Given the persistent strength in services, housing, and energy costs, our 2026 CPI forecasts remain elevated to reflect the longer-than-expected tail of these shocks. With the cash rate now sitting restrictively at 4.35%, we expect the RBA to hold at these levels to allow tight financial conditions to further cool domestic demand, though the Board remains explicitly willing to deliver another hike in words only.