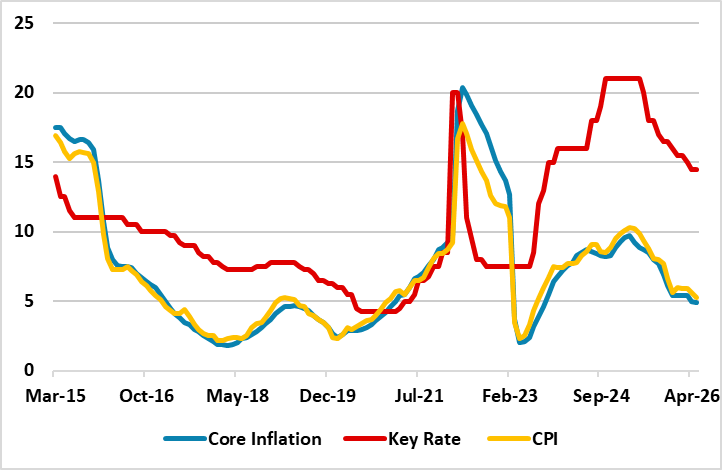

Russian Inflation Drops to 5.3% in May, Hitting Lowest Level Since August 2023

Bottom Line: Russia’s annual inflation continued its decreasing pattern moderately in May and slowed to 5.3% y/y. This deceleration was driven by the lagged effects of previous aggressive monetary tightening, a relatively resilient ruble, and softening core inflation. Marking the lowest level since August 2023, the May figure aligns with the Central Bank of Russia’s (CBR) projection that annual inflation will decline to 4.5–5.5% in 2026.

Figure 1: CPI, Core Inflation (YoY, % Change) and Policy Rate (%), January 2015 – May 2026

Source: Continuum Economics

After annual inflation edged down to 5.6% y/y in April, the decreasing trend continued moderately in May and inflation hit 5.3% y/y owing to lagged impacts of previous aggressive monetary tightening, relative resilience of RUB and softening core inflation. MoM inflation surged by 0.2% in May after a 0.1% rise the previous month. The core inflation eased to 4.9% in May from 5% in the previous month. Marking the lowest level since August 2023, the May figure aligns with the Central Bank of Russia’s (CBR) projection that annual inflation will decline to 4.5–5.5% in 2026.

According to Rosstat announcement on June 10, annual food inflation eased up, dropping from 4% in April to 2.9% in April, thanks to a bigger dive in fruit and vegetable prices (-10.4% in May vs -6.6% in April). Meanwhile, y/y non-food items got pricier (rising to 4.2% in May from 3.9% in April), and services climbed 1.6% compared to April m/m and 10.1% from the same period of last year.

Speaking about the inflation trajectory, President Putin recently said that "Inflation is falling — just over 5%. Therefore, I think we have every right to expect both a reduction in the key rate and the achievement of other necessary parameters."

The CBR projects annual inflation will decline to 4.5–5.5% in 2026, aiming for a return to its 4% target by 2027. Despite this, we still assess that meeting this target range could be challenging by the end of 2026 due to risks. Persistent sanctions, the fallout from the conflict in Iran, sustained military spending and excise taxes are likely to prolong the disinflationary process beyond the CBR's expectations as pro-inflationary risks still prevail over disinflationary ones.

We believe a peace deal in Ukraine remains the real key to ease pressure on inflation in the mid-term horizon and alleviate demand-supply imbalances in Russia.