SNB: Holding Steady on Rates

The June quarterly assessment saw little shift in the forecasts for either growth or inflation (Figure 1), with the tone of the economic outlook remained guarded due to concerns over the Iran war on the global economy (forecasts though look to have been completed before the U.S. Iran deal). With inflation forecast within the confines of its target range (defined officially as less than 2%), this will be enough to justify stable policy now and for some time. We still see policy remaining on hold until at least mid-2027, with only a slight possibility of a return to sub-zero rates given the high(er) bar seen by the SNB for this to occur. The strong Swiss Franc was also mentioned but its current strength needs the context of a still competitive Switzerland.

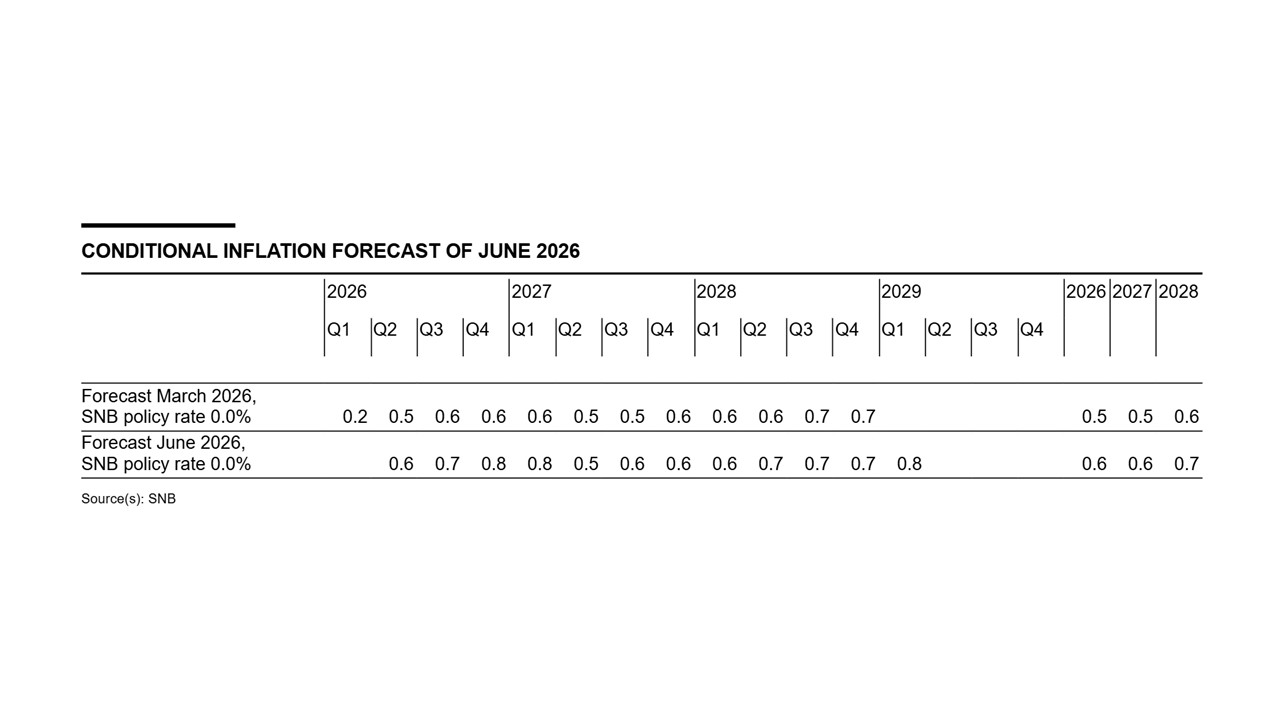

Figure 1: SNB Inflation Outlook Little Changed

Source: SNB

The SNB noted that CPI has rotated higher with the increase in energy prices and this has marginally pushed the CPI projections higher. Even so, the forecasts appear to have been completed before this week’s U.S./Iran war interim agreement and the near-term multi quarter inflation outlook could be revised down in September. As we have previously noted though the Swiss Franc strength has played a part in keeping inflation under control, weak domestic price pressures is also a disinflation force. Additionally, with a still soft 2026 GDP growth of around 1%, the sports adjusted GDP growth this year may be below 1% and thus some 0.5% below potential. This helps restrains domestic prices.

For policy the guidance is for stable policy rates, with inflation projections consistent with target and domestic disinflation counterbalancing risks noted in the statement of a renewed surge in energy prices (probability of the latter is lower after the U.S./Iran deal).

The strong Franc, more recently against the USD, did not have major policy impact. While still pointing to possible FX intervention and a continued willingness to adjust policy accordingly, the SNB was keen to suggest its currency aspirations and actions are not designed to boost Swiss competitiveness. But this seems more talk than action as any overt attempt to weaken the current via intervention or lower/negative rates may be shunned by the SNB for fear it would court U.S criticism and possibly fresh tariff retaliation. A high bar also exists for any return to negative borrowing costs the SNB has been clear this is because of the adverse impact on savers and pension funds (SNB President Schlegel stressed this in a recent interview).