Fuel and Transportation Costs Pushed South African Inflation to 4.5% in May

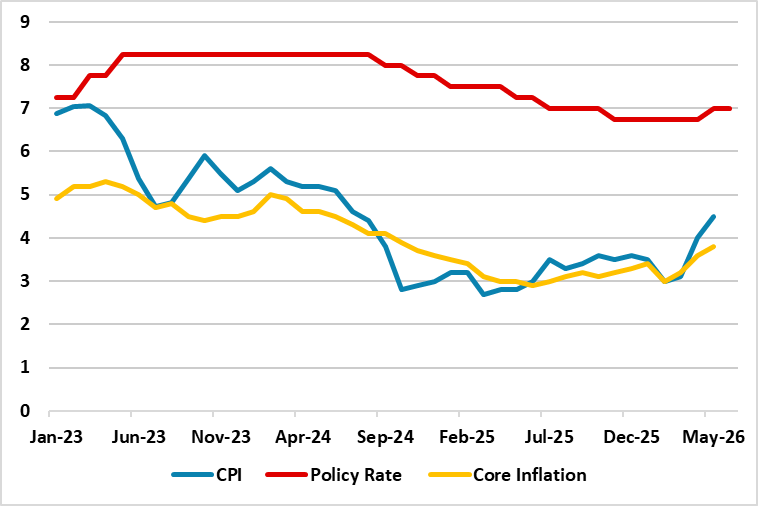

Bottom Line: South Africa’s annual inflation climbed to 4.5% in May driven by surging fuel and transport costs, according to StatsSA's announcement. The core inflation surged to 3.8% y/y in May from 3.6% in the previous month, marking the highest reading since October 2024. While we anticipate that inflation will begin to ease in late H2 as Iran tension subsides, the recovery will likely be gradual. Returning to the 3% inflation target range will be a slow process due to the lagged secondary impacts of the conflict.

Figure 1: CPI, Core Inflation (YoY, % Change) and Policy Rate (%), January 2023 – June 2026

Source: Continuum Economics

After surging to 4.0% y/y in April, South Africa’s inflation edged up to 4.5% y/y in May reaching its highest level since July 2024, which was driven by increases in fuel prices. Inflation was ignited by a second consecutive surge in fuel prices, which jumped 14.3% in May to hit an annual increase of 28.7%. This upward momentum was further fueled by rising costs in transportation—which climbed 9.4% y/y compared to 4.9% in April—and housing and utilities, which edged up slightly to 5.3% y/y from 5.2% in April. Inflation for food and non-alcoholic beverages continued to subside, declining to 1.9% in May from 2.9% in April, which marked a down from the peak of 5.7% recorded in July 2025.

According to the StatsSA announcement, m/m prices increased by 0.7% in May when compared to April. The core inflation surged to 3.8% y/y in May from 3.6% in the previous month, marking the highest reading since October 2024.

Despite concerns due to the outbreak of war in Iran, South Africa’s national utility, Eskom, announced on June 5 that the country has achieved 385 consecutive days without power interruptions. With only 26 hours of load-shedding recorded across April and May 2025, the stabilized power supply remained a positive buffer against inflationary risks.

The conflict in Iran continued to pressure South Africa's inflationary outlook in May. Because the country imports the majority of its petroleum products, it remained vulnerable to swings in global energy prices. While we anticipate that inflation will begin to ease in late H2 as Iran tension subsides, the recovery will likely be gradual. Returning to the 3% inflation target range will be a slow process due to the lagged secondary impacts of the conflict.