Preview: Due July 2 - U.S. June Employment (Non-Farm Payrolls) - World Cup boost versus underlying slowing

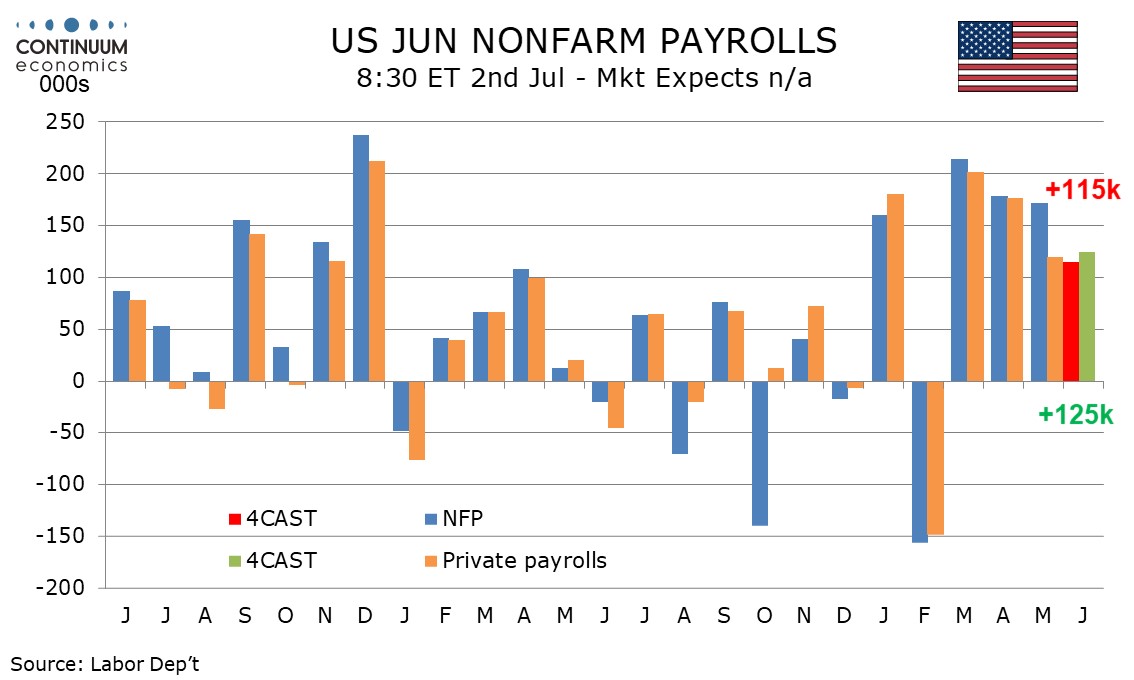

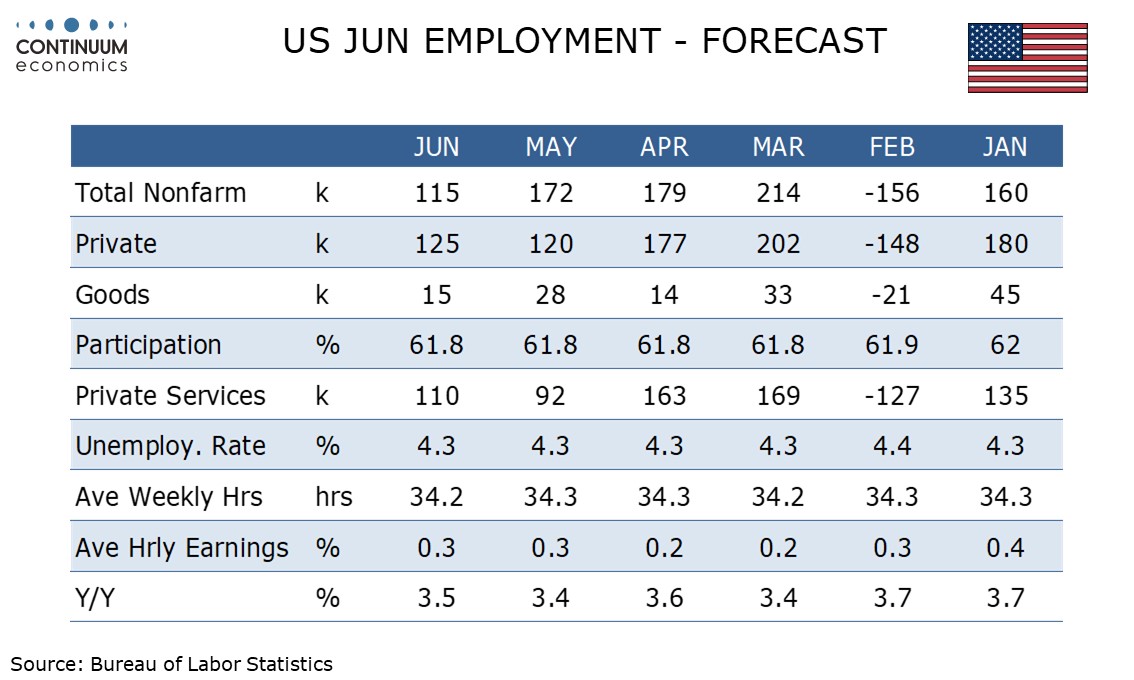

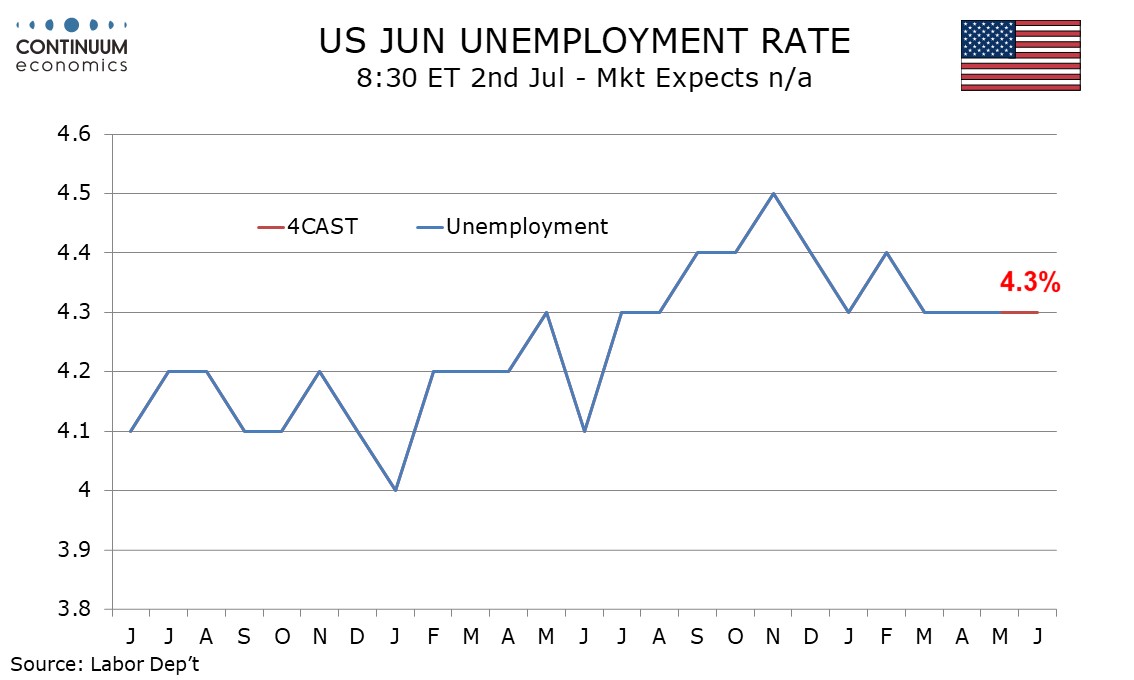

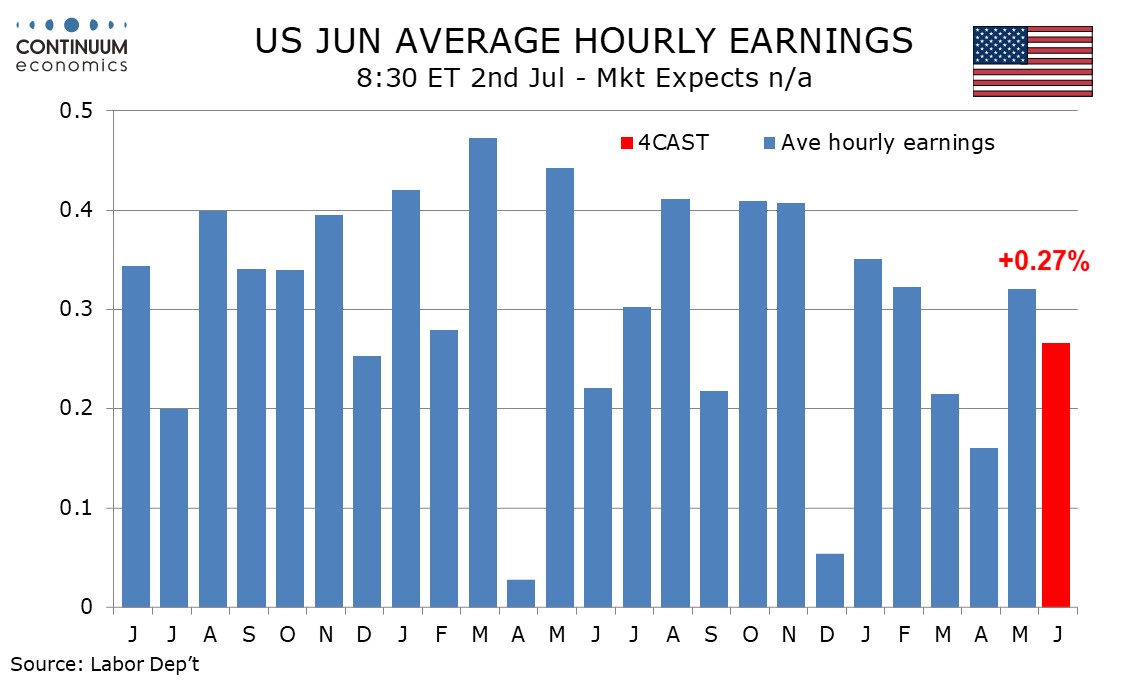

We expect June’s non-farm payroll to rise by 115k overall and by 125k in the private sector, the former a slowing from 172k in May but the latter marginally stronger than May’s 120k increase. We expect the unemployment rate to remain at 4.3% for a fourth straight month and an in line with trend 0.3% rise in average hourly earnings.

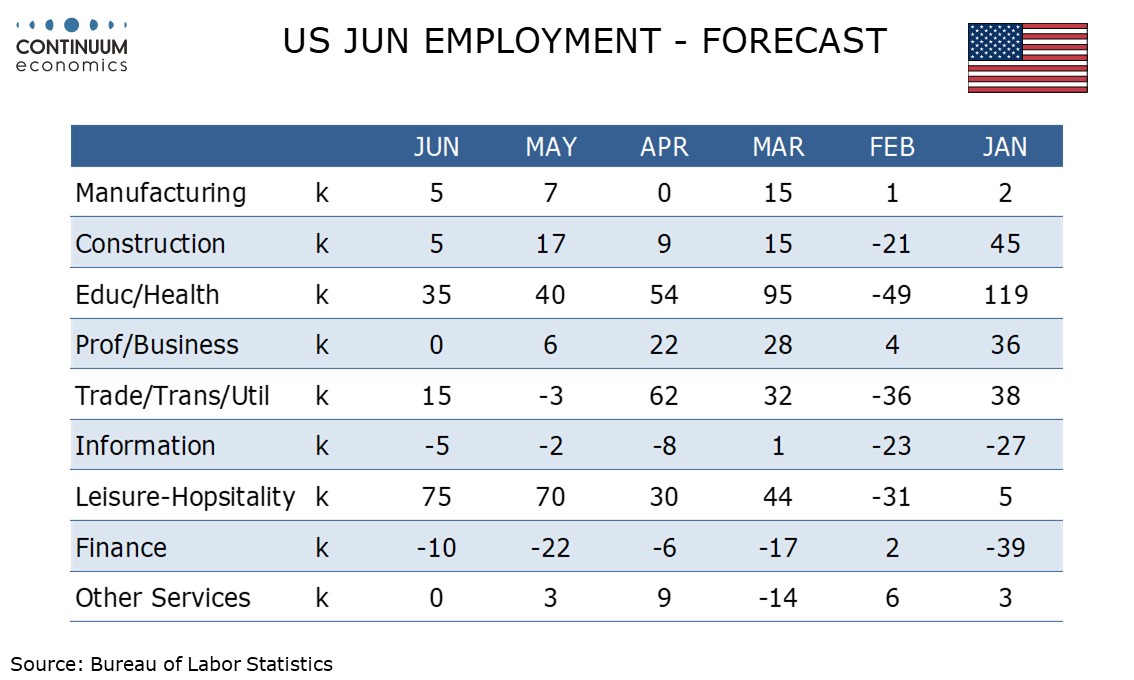

May’s gain was less impressive than the strong headline implied. 55k came from local government which looks unlikely to be repeated. 70k came in leisure and hospitality which looks inflated by the approach of the World Cup, and while likely to be extended in June is still temporary. 47k came in health care and social assistance, a below trend gain from a sector that has led most recent payroll gains. Excluding these three sectors payrolls were unchanged.

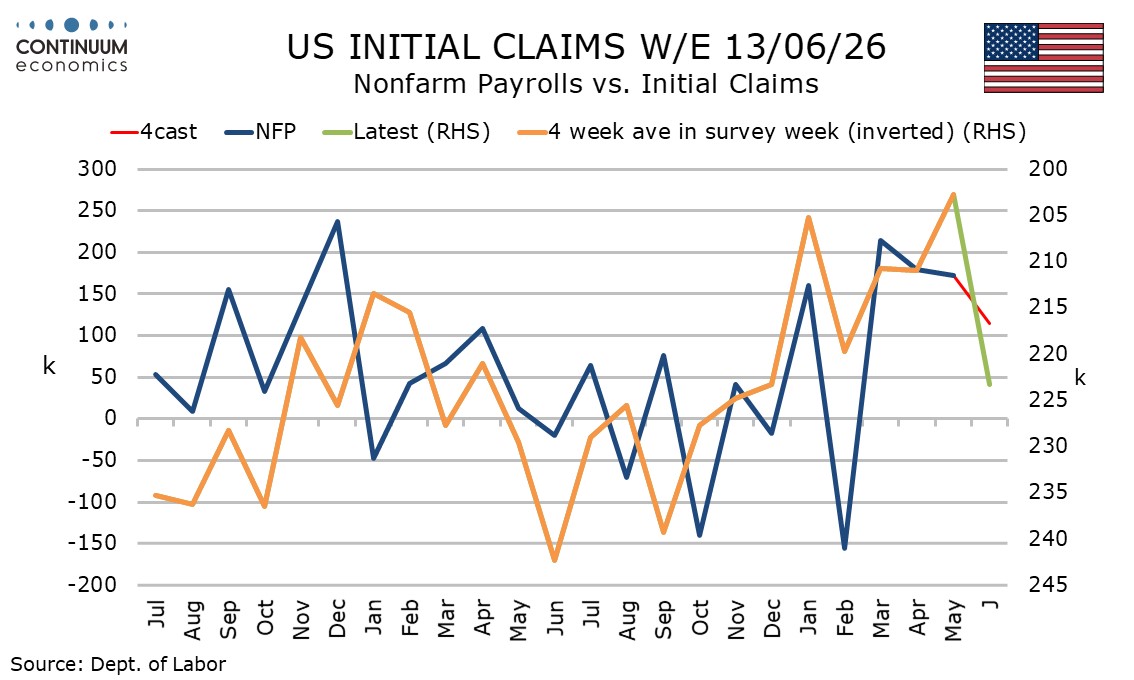

We expect a stronger gain still from leisure and hospitality of 75k in June, but elsewhere we expect a subdued payroll gain, with initial and continued claims looking consistent with a loss of labor market momentum.

We expect government payrolls to correct lower by 10k. Our forecast for private payrolls ex leisure and hospitality is 50k, which would match May’s increase, but be considerably slower than gains of near 150k in both March and April.

We expect a modest slowing in goods, largely due to construction with manufacturing sustaining a recent move in trend above neutral, while private services may see support from retail where resilient May sales contrasted a marginal dip in employment. Information and finance are now trending negatively, and that looks connected to adoption of AI.

While we expect a fourth straight month of unemployment at 4.3%, we expect the gain in employment to exceed that in the labor force, seeing the rate falling to 4.27% from 4.34% before rounding.

Average hourly earnings rose by 0.3% in May, and a little above 0.3% before rounding, after two straight gains of only 0.2%. We expect another increase of 0.3% in June, though a slightly slower 0.27% before rounding. This would still lift yr/yr growth to 3.5% from 3.5% in May, but trend has slowed from around 4.0% in mid-2025.

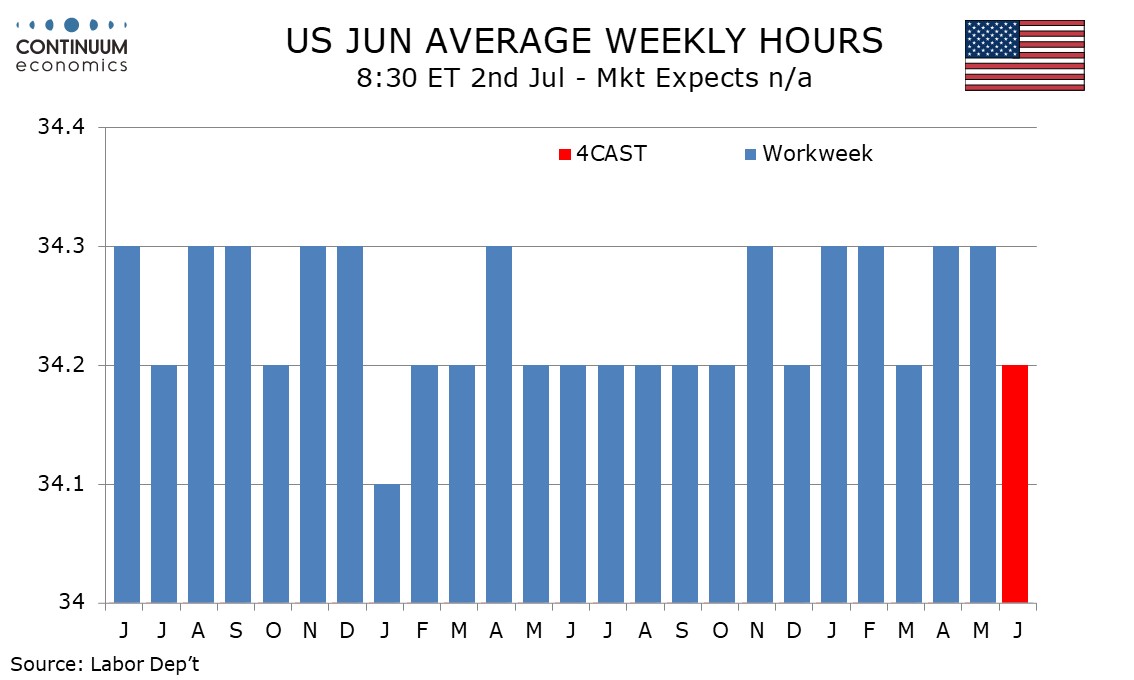

We lean to a decline in the workweek to 34.2 hours after two straight months at 34.3, given that three straight gains of 34.3 would be unusual, and it is over two years since outcome above 34.3 was seen. This would still leave aggregate hours up by 1.6% annualized in Q2, which would be the strongest quarter since March 2023.