U.S. May Retail Sales - Impressive resilience

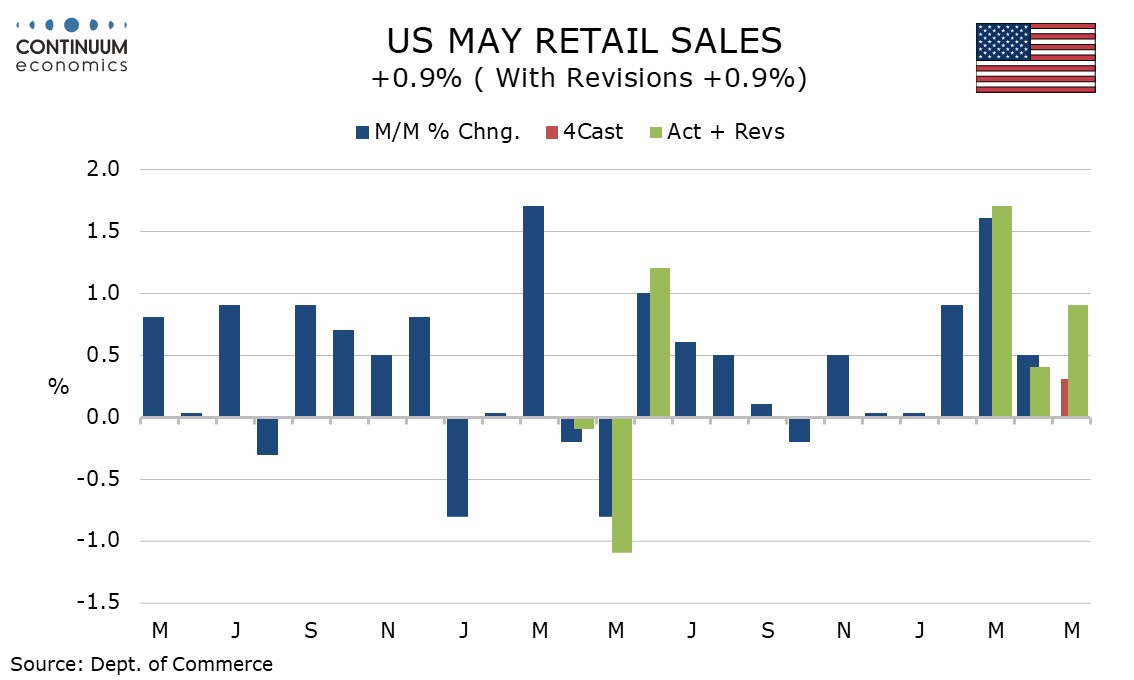

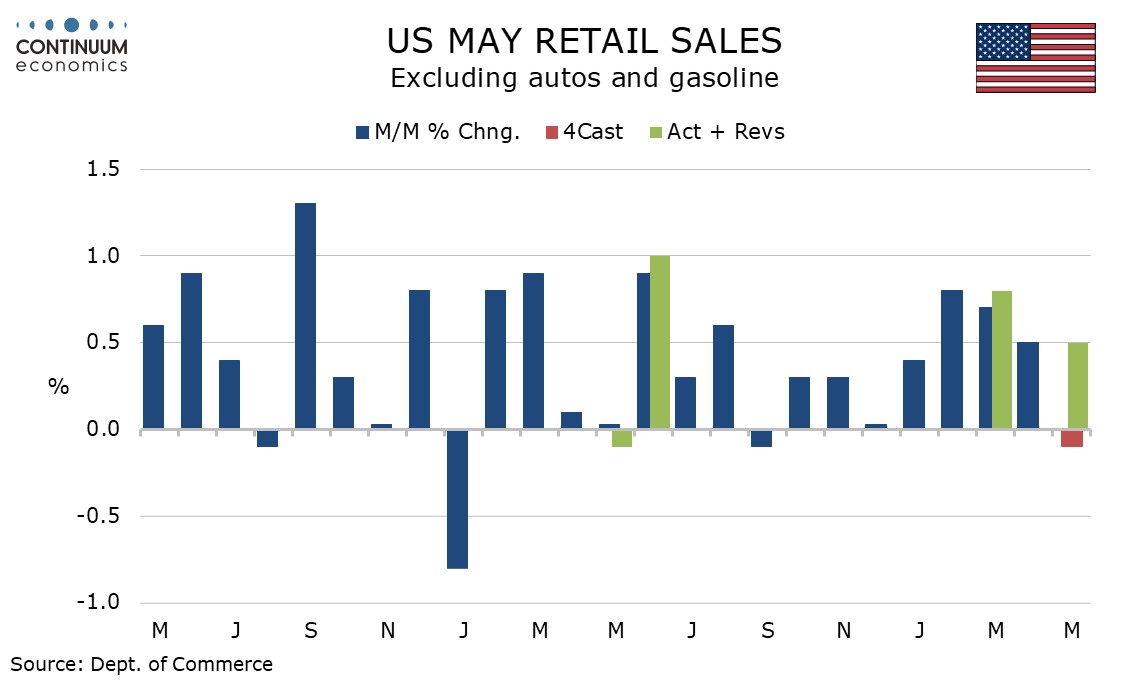

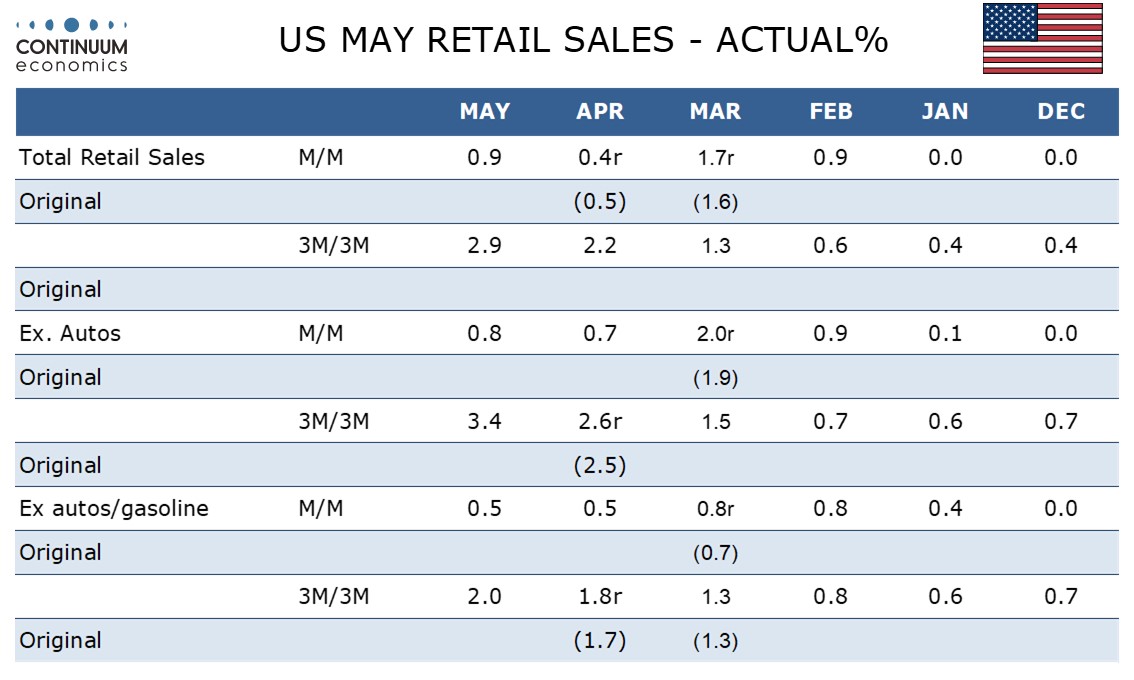

May retail sales continue to show impressive resilience to downward pressure on real disposable income from rising gasoline prices, with equity strength and lower taxes offsetting to the headwinds, as well as recent resilience in employment, Overall sales rose by 0.9%, with gains of 0.8% ex auto and 0.5% ex auto and gasoline.

The control group, which contributes to GDP, increased by 0.7%. Revisions were a net neutral with March revised up to 1.7% from 1.6% but April revised down to 0.4% from 0.5%. Both ex auto and ex auto and gasoline however the net revision was marginally positive with March revised up by 0.1% and April unrevised.

The recent strength in nominal terms is in part due to price gains, with the CPI having shown a 0.8% rise in commodity prices in, suggesting retail sales showed only modest growth in real terms, but with the CPI showing commodity prices ex food and energy falling by 0.1%, the 0.5% sales ex auto and gasoline is quite impressive.

A 3.4% rise in gasoline sales is likely to be fully explained by prices. Gains of 1.2% in autos and 1.0% in furniture and home furnishing corrected declines in April. Food at unchanged at food services and eating and drinking places at -0.1% both showed weak months. Most components showed moderate gains but miscellaneous at 2.3% and non-store retailers at 1.5% saw strong gains.

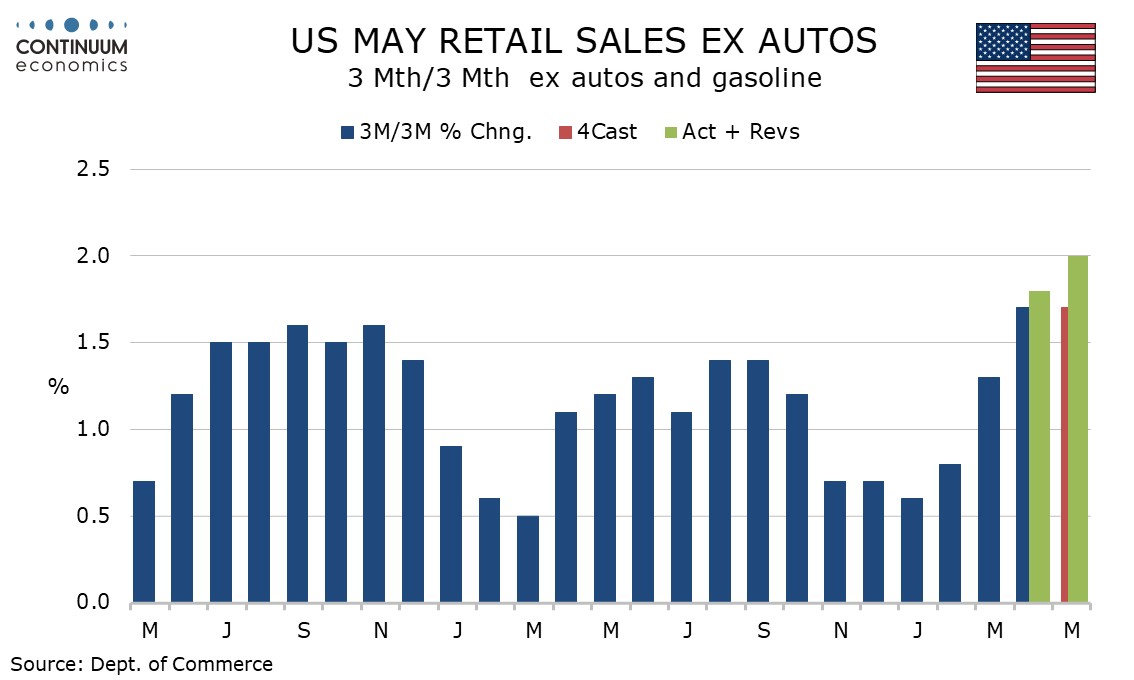

3 month/3 month changes both overall and ex autos are inflated by surging gasoline prices but even ex autos and gasoline there has been some recent acceleration. The 3 month/3 month change there is now at 2.0% (not annualized) and the highest since March 2023, impressive even when noting that Q1 data was restrained by weather.

Looking ahead downside risks remain unless gasoline prices stage a quick reversal in response to the Middle East peace deal, but for now the consumer remains impressively resilient. This further confirms that the Fed’s appropriate focus is on upside risks to inflation rather than downside risks to activity.