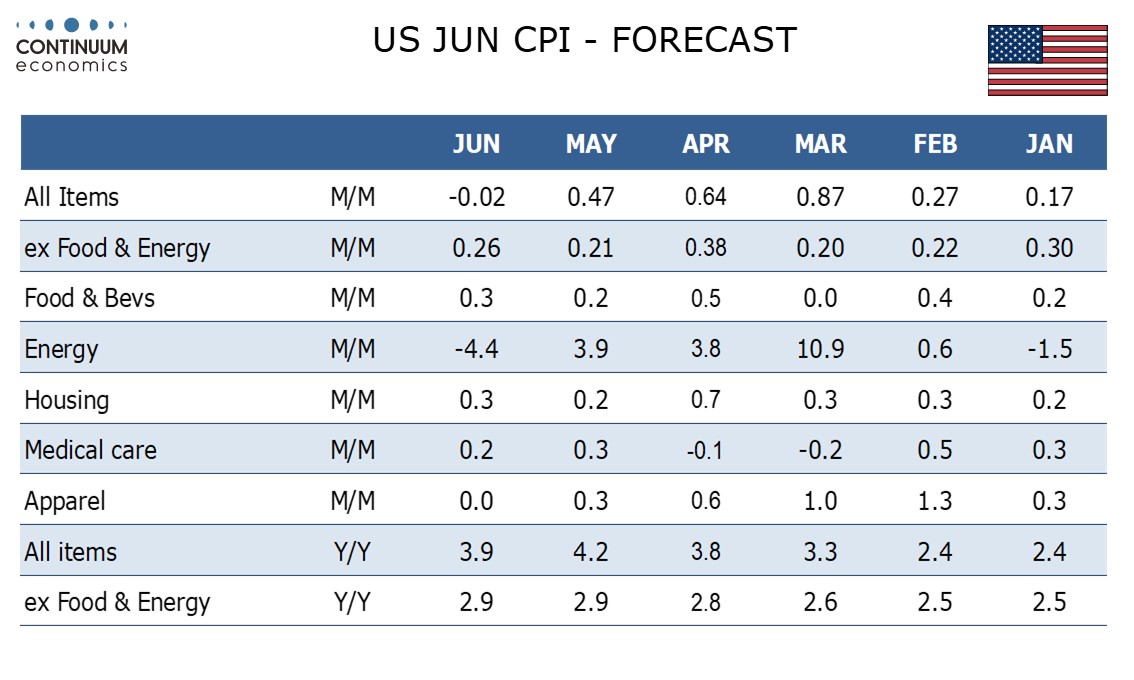

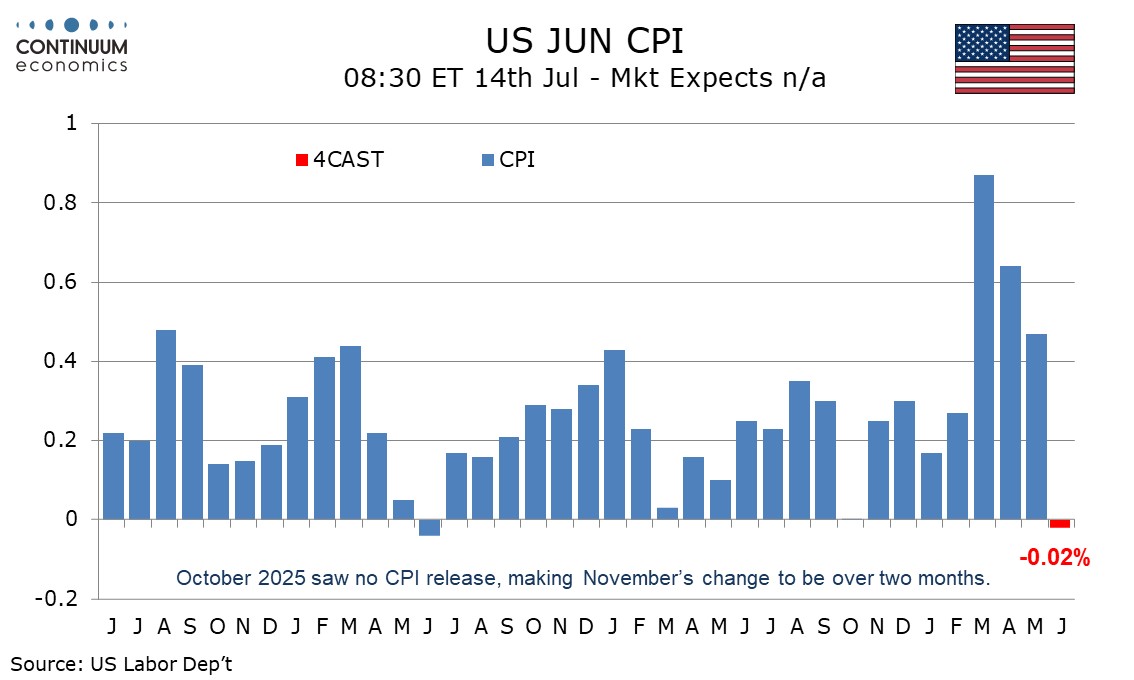

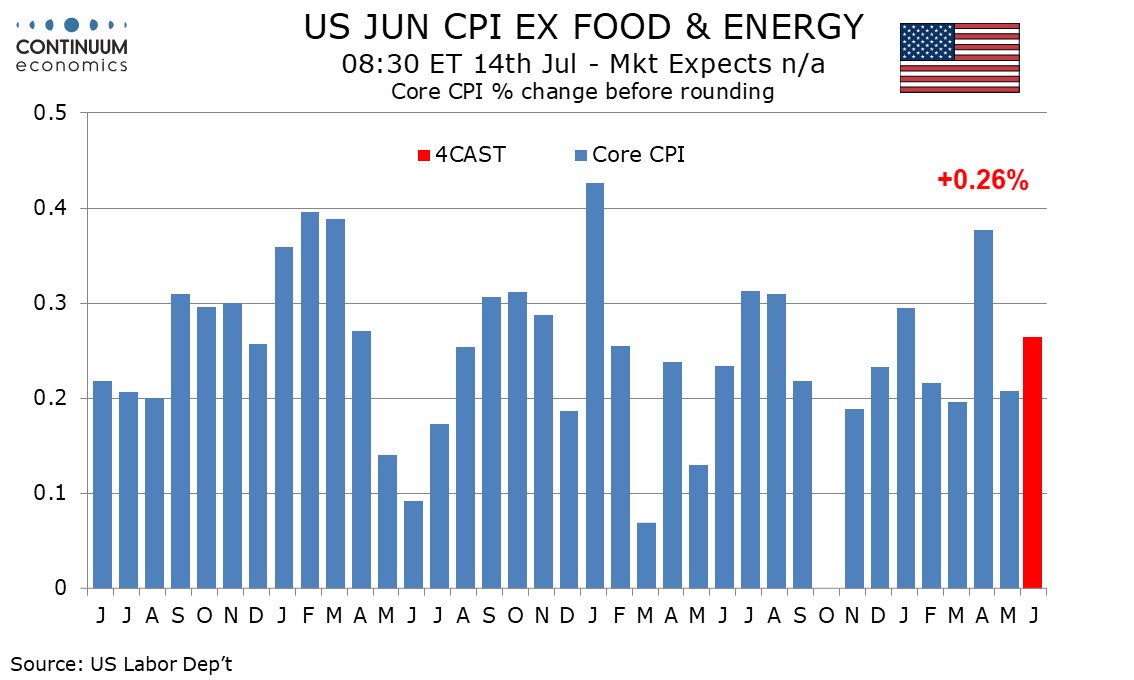

Preview: Due July 14 - U.S. June CPI - Energy to correct lower, World Cup to support core

We expect June CPI to be unchanged overall as energy corrects from three straight strong gains while the core rate ex food and energy sees a slightly firmer 0.3% increase. Before rounding we expect respective outcomes of -0.02% and up 0.26%, with the World Cup having just enough impact to nudge the core rate to 0.3% before rounding.

Gasoline prices peaked in mid-May and have since been moving lower in weekly data, though remain well above pre-war levels. We expect a 9.2% decline in gasoline to lead a 4.4% decline in energy, following energy gains of 3.9% in May, 3.8% in April and 10.9% in March. We expect a 0.3% rise in food after a 0.2% increase in May.

Core rates have generally been moderate since a 0.3% rise in January, apart from a 0.4% increase in April which was inflated by housing price gains recorded every six months having been missed in October when the government shutdown meant no survey was conducted. February, March and May all saw gains of 0.2% meaning that our 0.3% June forecast represents a modest acceleration.

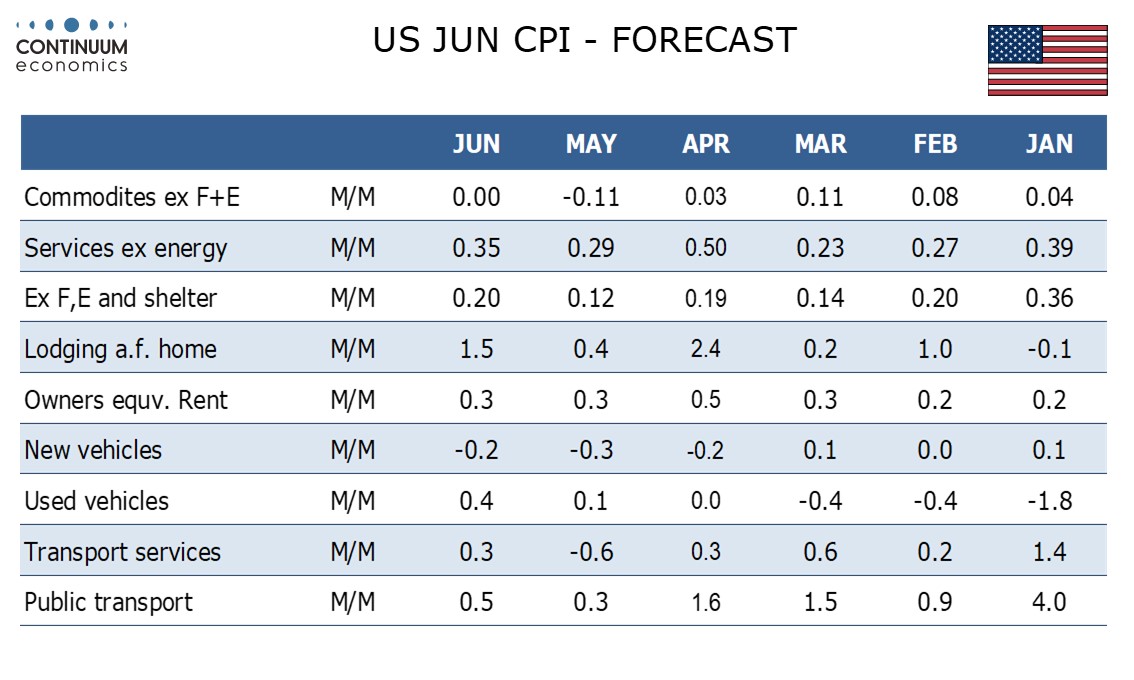

There are two sources of upside risk. Firstly the World Cup is likely to cause a temporary lift to prices, particularly in hotels but also in some other consumer-facing services. Secondly CPI ex food, energy and shelter at 0.12% in May was unusually soft and may see a correction higher, we expect by a moderate 0.2%. A 1.7% May decline in motor vehicle insurance in particular looks unlikely to be repeated. We expect goods ex food and energy to be unchanged but services ex energy, lifted by hotels which are included in shelter, to rise by 0.35%.

We expect yr/yr CPI to slip to 3.9% from May’s 4.2% that was the highest since April 2023. We expect the yr/yr ex food and energy rate to be unchanged at 2.9%, matching May’s pace that was the highest since the September 2025 survey, before the government shutdown prevented an October survey.