U.S. June Retail Sales - Underlying resilience persists, Initial Claims fall and Philly Fed surges

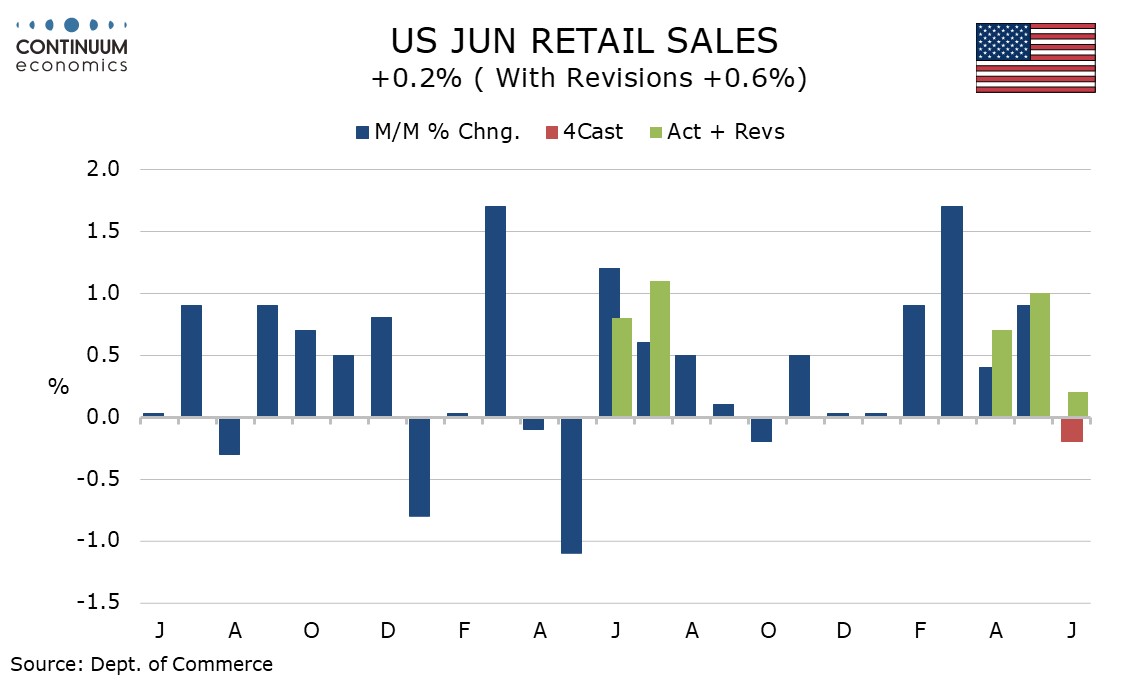

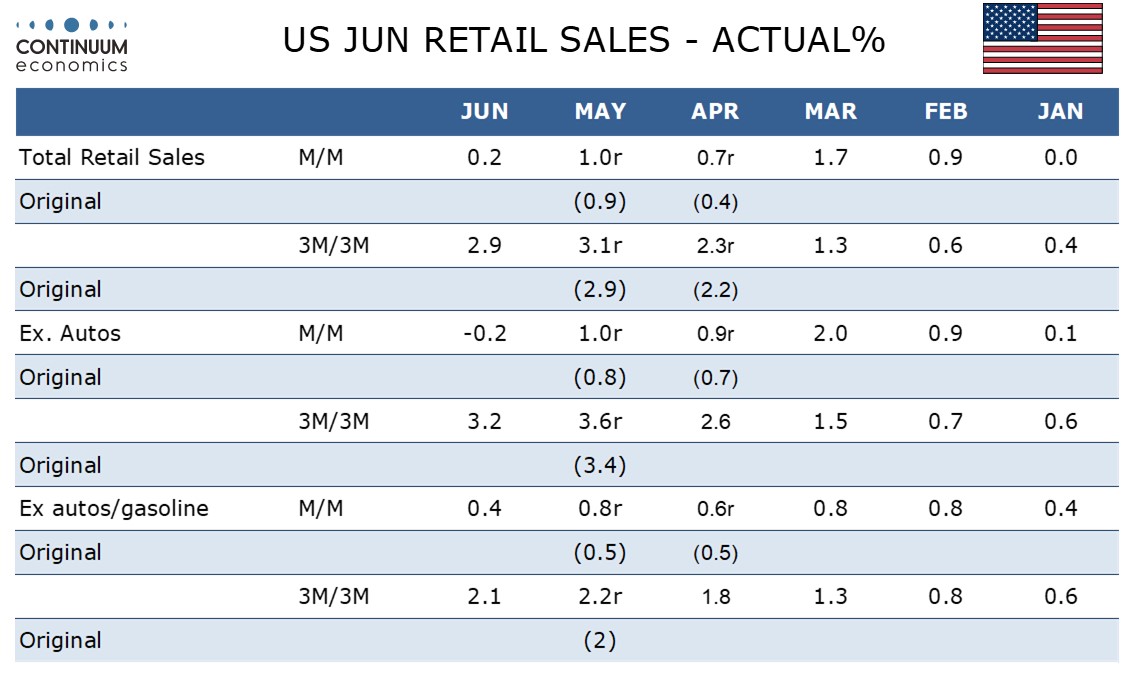

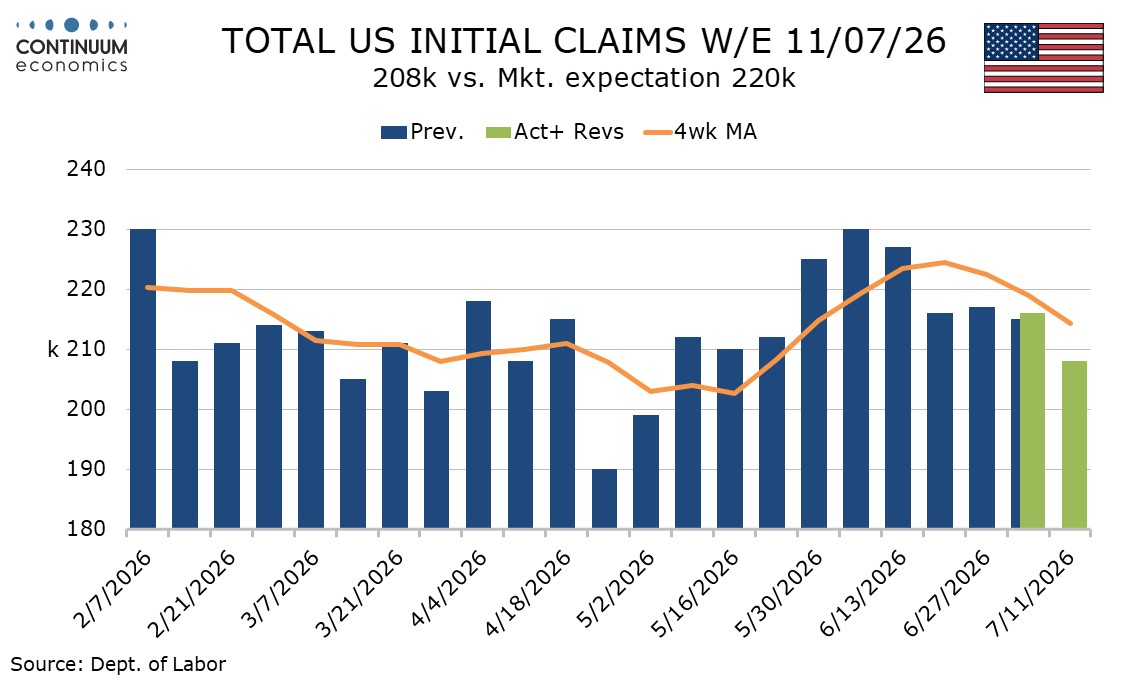

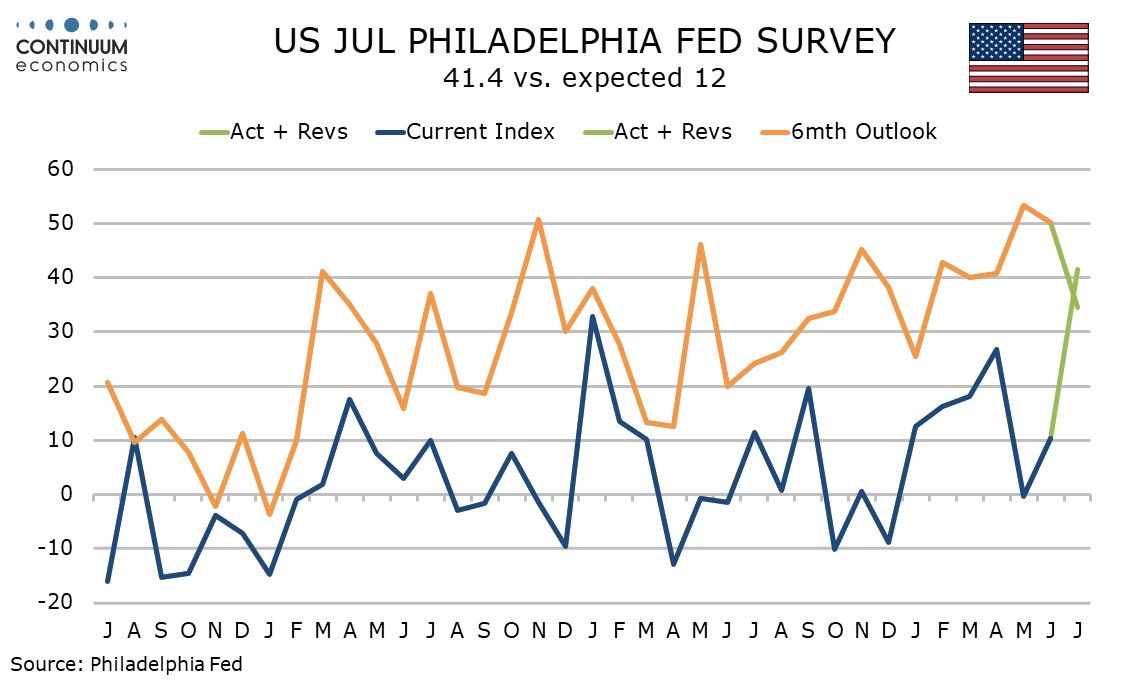

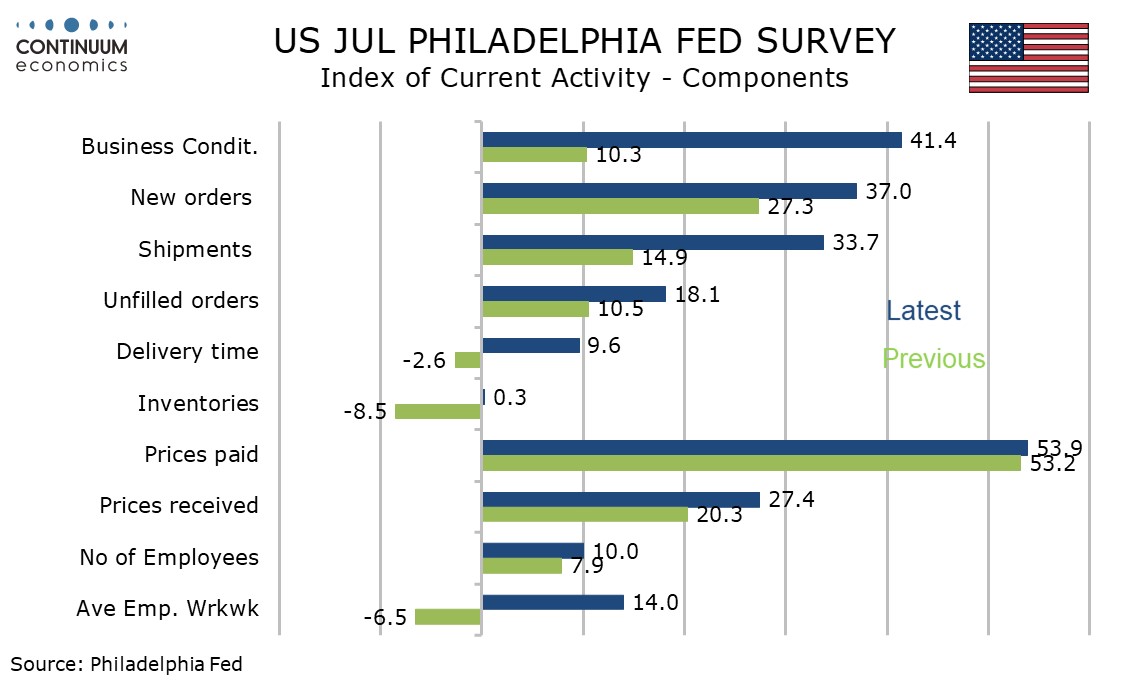

The latest US data is on the firm side of expectations. June retail sales are in line with expectations with a 0.2% increase and a gasoline-led 0.2% decline ex autos., but the control group that contributes to GDP maintains underlying strength with a rise of 0.5%. Weekly initial claims at 208k from 216k are the lowest since May 6 while July’s Philly Fed manufacturing index of 41.4 from 10.3 is the highest since April 2021.

A 5.3% fall in gasoline sales appears to be slightly more than fully explained by price declines and gasoline sales are still up 19.8% yr/yr, also largely on price changes. A second straight positive contribution from autos is in line with the signals from industry sales data.

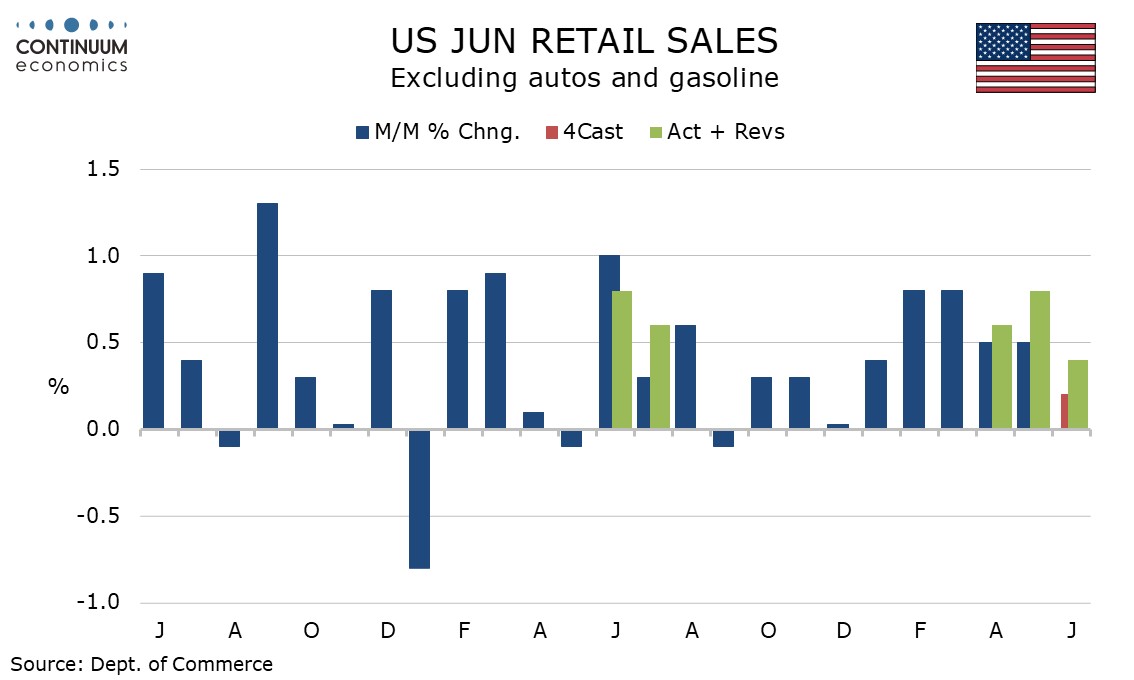

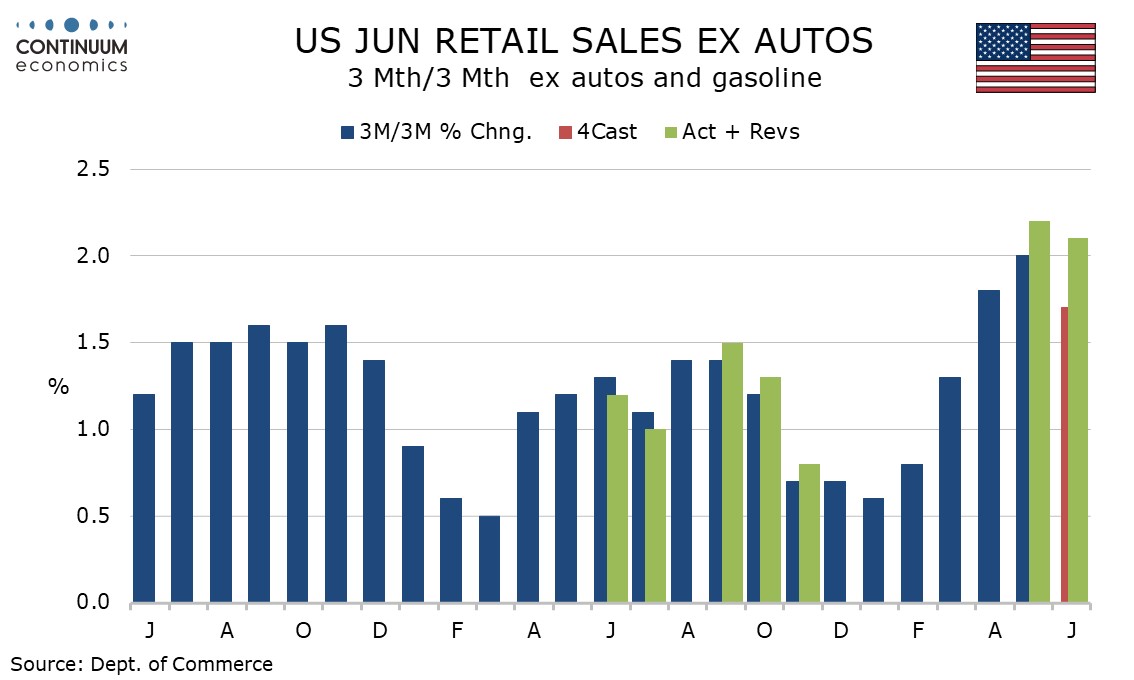

Ex auto and gasoline sales rose by 0.4% with May revised to 0.8% from 0.5% and April revised to 0.6% from 0.5%. The series has posted respectable gains in every month of the year to date and the Q2 gain of 2.1% (not annualized) is the strongest quarterly increase since a matching Q1 of 2023.

The resilience of consumer spending contrasts with weakness in real disposable income. Supportive factors for consumers are equity strength and lower taxes (though the latter as not been sufficient to prevent real disposable income weakness). Consumers have been dipping into savings to compensate for strength in gasoline prices.

The ex auto and gasoline gain is not broadly based, with little strength outside gains of over 1.0% in sporting goods and non-store retailers, and a 0.8% rise in electronics and appliances.

Initial claims slippage should be treated cautiously with non-seasonally adjusted claims up to 245k from 226k. The seasonals assume layoffs from summer retooling in auto plants, which gave probably been more limited than usual this year. The survey week for July’s non-farm payroll comes next week and is less at risk from seasonal adjustment issues.

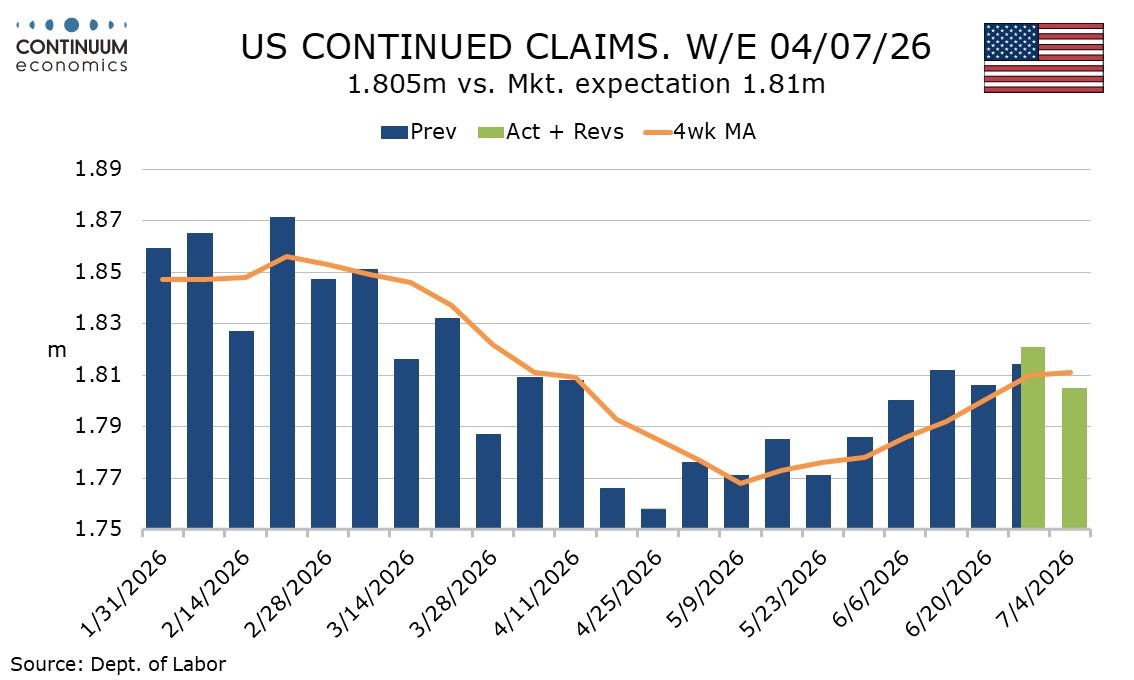

Continued claims cover the week before initial claims. They also fell, to a 4-week low of 1.805m from 1.821m, though the 4-week average has reached its highest since April 4.

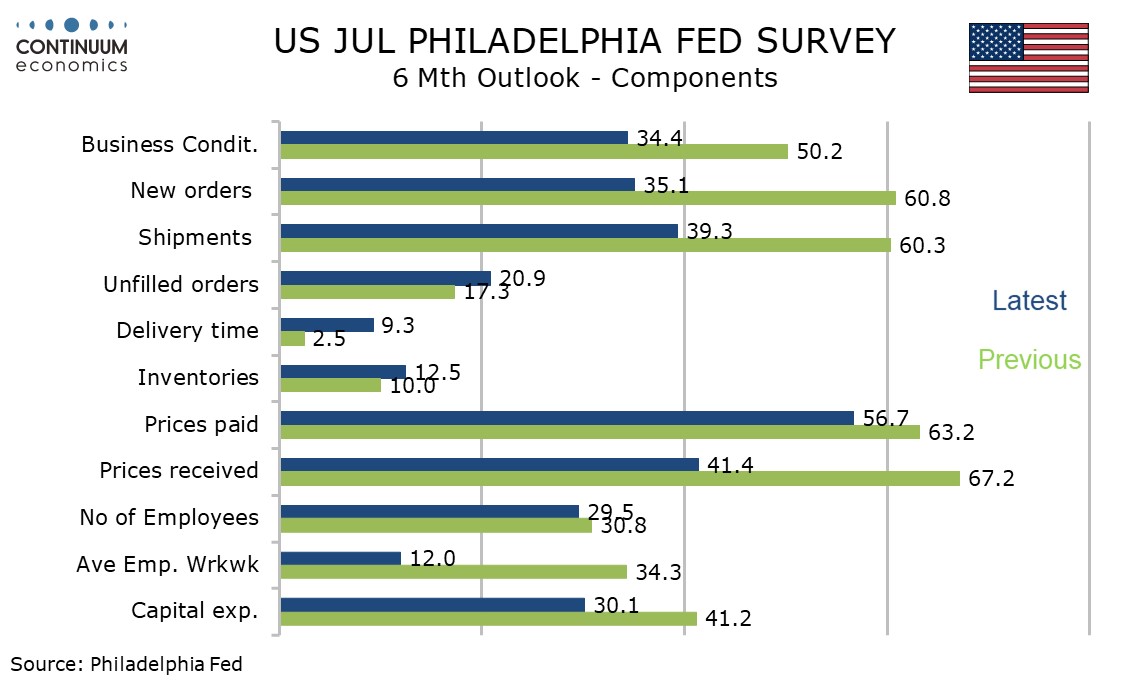

July’s Philly Fed is more impressive, though the detail is not quite so, new orders at 37.0 from 27.3, employment at 10.0 from 7.9 and the workweek at 14.0 from -6.5, all up but less sharply than the headline. 6-month expectations at 34.4 from 50.2 are the lowest since January.

Despite easing in oil, price expectations are actually higher, paid at 53.9 from 53.2 and received at 27.4 from 20.3, though 6-month price expectations are lower, paid at a 3-month low of 56.7 from 63.2 and received at 4-month low of 41.4 from 67.2.

The Philly Fed probably overstates manufacturing strength with yesterday’s Empire State survey of 15.6 not so impressive, but even that was up from 5.7 in June. The manufacturing sector is being supported by heavy investment in AI.