FOMC Minutes from April 29: Hawkish concerns appear broadly felt

FOMC minutes from April 29 show a hawkish leaning, confirming market perceptions that there was more interest in removing an easing bias from the language than revealed by the three hawkish dissents at the meeting. Should inflation remain persistent, tightening could come onto the agenda, though should the Middle East situation get resolved, talk could still move back towards easing.

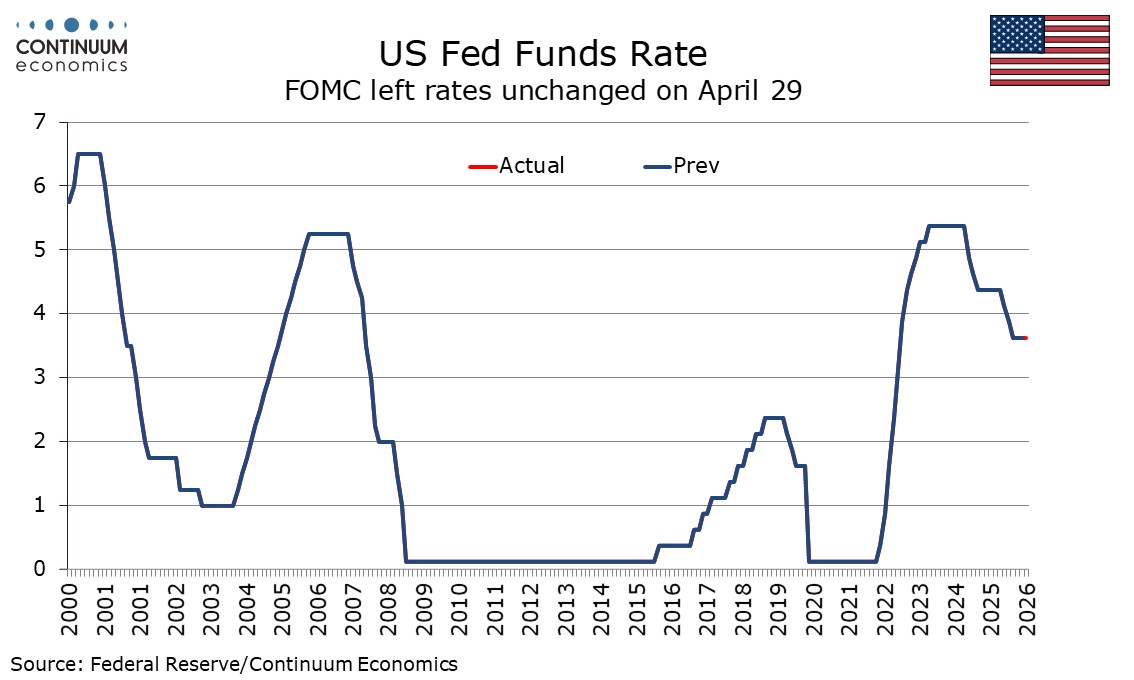

Almost all participants supported maintaining the Fed Funds target at 3.5-3.75%, and the one dovish dissenter, Stephen Miran, no longer sits on the FOMC. Several participants highlighted easing would likely be appropriate once there are clear indications that disinflation is firmly back on track or if solid signs emerge of greater weakness in the labor market. Neither of those conditions look likely to be met in the near term, though several looked to a scenario where rate cuts would be warranted later in the year if the Middle East conflict was resolved soon. Soon on April 29 may mean very soon today.

A majority felt that some policy firming would likely become appropriate if inflation were to continue to run persistently above 2%. This looks likely if flows through the Strait of Hormuz are not resumed. To address this possibility many participants stated that they would have preferred removing the language that suggested an easing bias. It looks clear that the concerns of the three hawkish dissenters who voted to change the language were more widely shared, as was suggested by outgoing Chairman Powell in his post-meeting press conference.

Discussion on the economy shows concerns about inflation went beyond the implications of the Middle East conflict, and even these went beyond energy, with shipping costs, air fares, fertilizer and other non-energy commodities noted. Some noted that recent price increases in the IT sector had contributed to higher inflation. Several anticipated that higher productivity increases would put downward pressure on inflation but several also highlighted the risk that several years of above target inflation could have an increased effect on wage and price-setting decisions. While a fall in labor demand pushing unemployment sharply higher was noted as a risk by several, participants generally agreed that labor market conditions would remain stable in the near term, consumer spending had been resilient and that the pace of real GDP growth would remain solid this year.

After the meeting we pushed our forecast for easing back to December from September, seeing only one ease this year rather than two. Without a swift resolution to the Middle East conflict we may have to push easing into 2027, and under a persistent closure of the Strait of Hormuz tightening before the end of the year may become the majority view at the FOMC. Resisting the will of the majority would be difficult for incoming Chair Kevin Warsh to do.