GBP flows: GBP marginally softer after UK data

UK retail sales soft and borrowing higher but GBP only slightly softer. But medium term risks on the downside

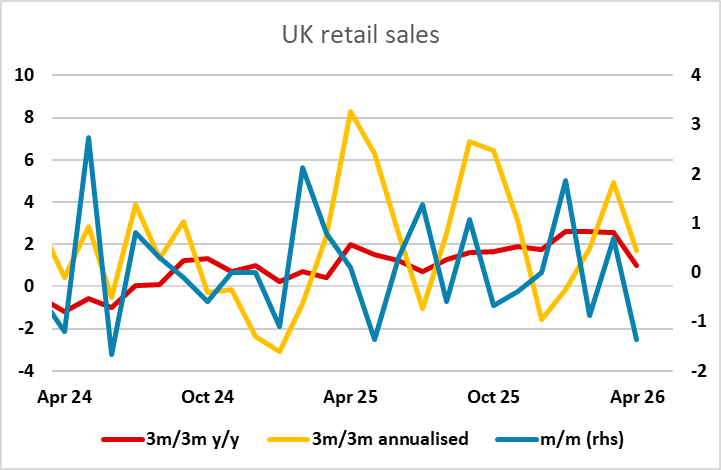

UK retail sales for April have come in much weaker than expected at -1.3% m/m, but the core was only marginally weaker than anticipated at -0.4% m/m, with fuel sales weak following a strong March when consumers tried to stock up. While the latest data was on the weak side, the last 3 months have still been positive because of the base effect of a strong January, and with core less weak than the headline, the data is no major cause for concern at this stage.

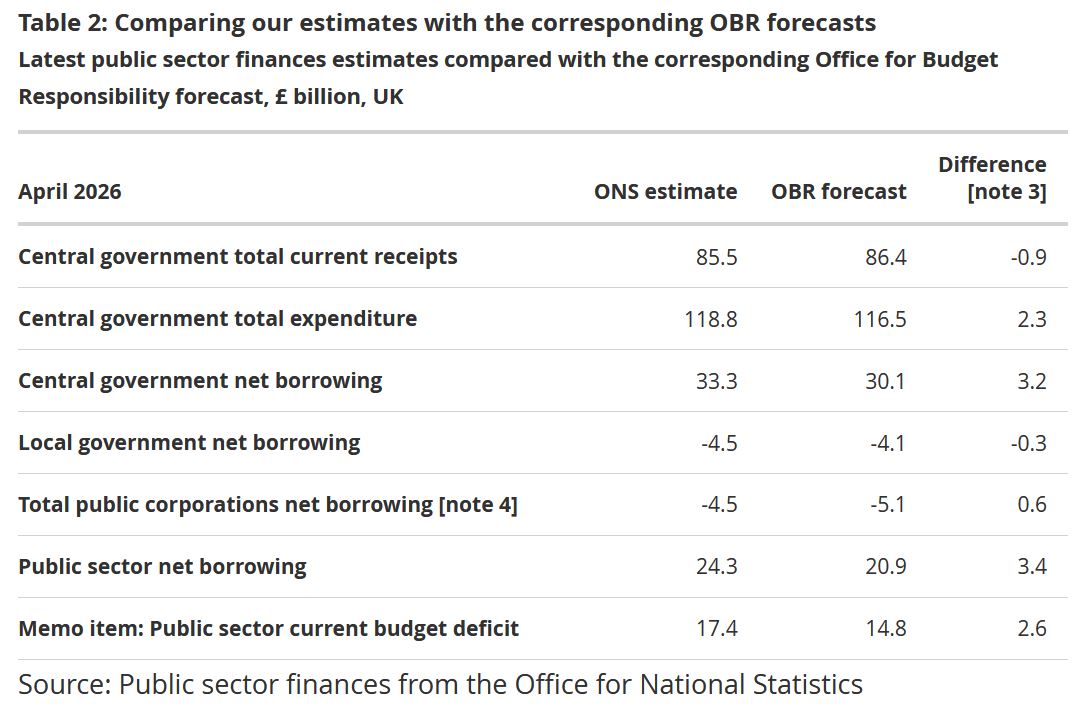

Perhaps more important is the public sector borrowing data, which showed a larger than expected net requirement of £24.7bn in April. Given the political uncertainty in the UK and the potential for Starmer to be replaced by a more fiscally loose administration, rising borrowing levels could further unsettle the gilt market.

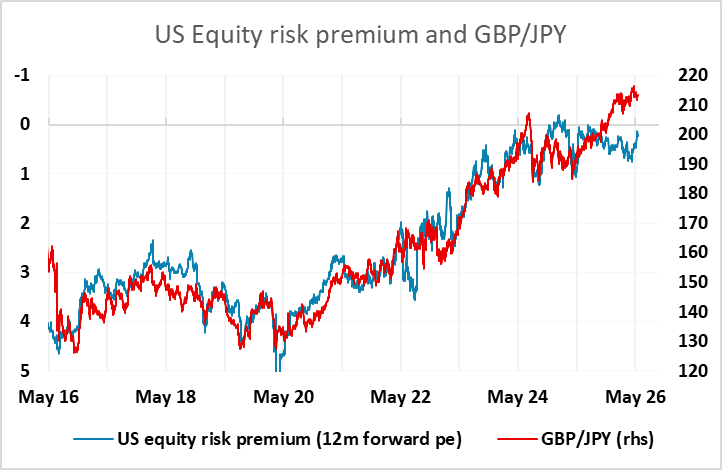

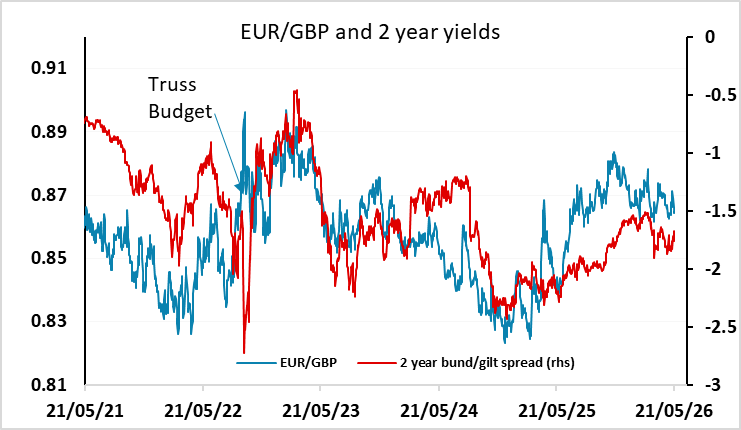

GBP has only edged slightly lower in response to the data, but still looks toppy against a range of currencies, notably the JPY, but EUR/GBP also still looks unlikely to trade consistently below 0.86 as long as the political uncertainty continues, and this looks likely to last through the summer at least. Nevertheless, with both the UK and the Eurozone PMIs yesterday showing weakness in May, we would still see more potential for GBP to weaken against the USD and JPY than the EUR.