FOMC - Policy may prove less hawkish than the dots, assuming slowing in data

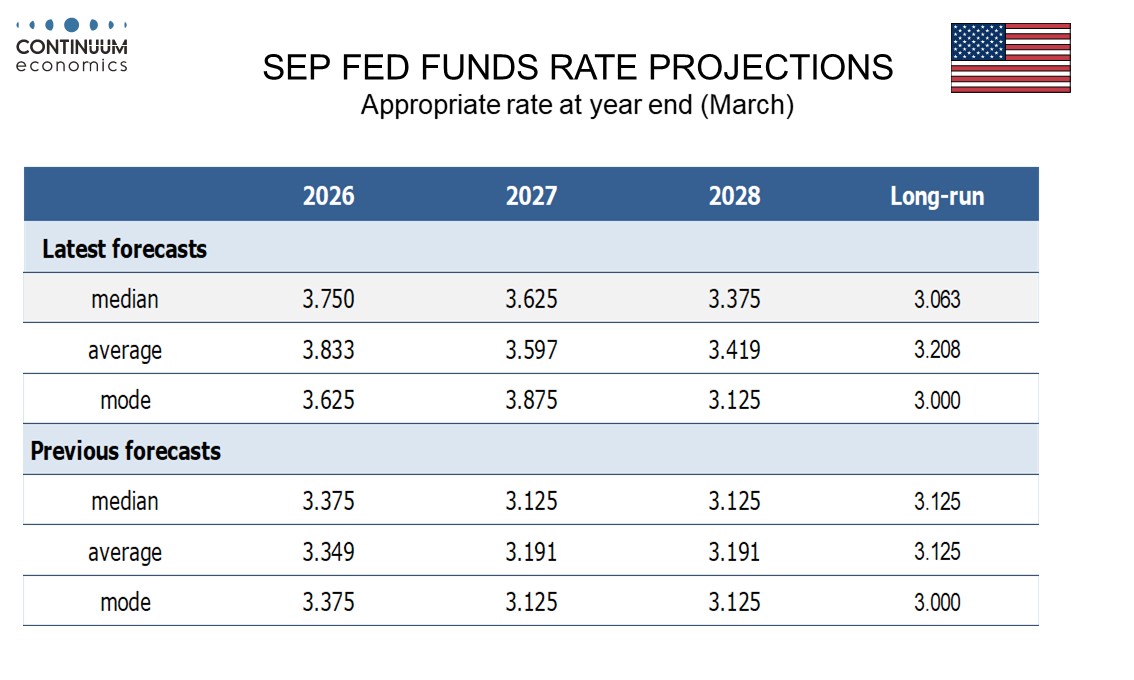

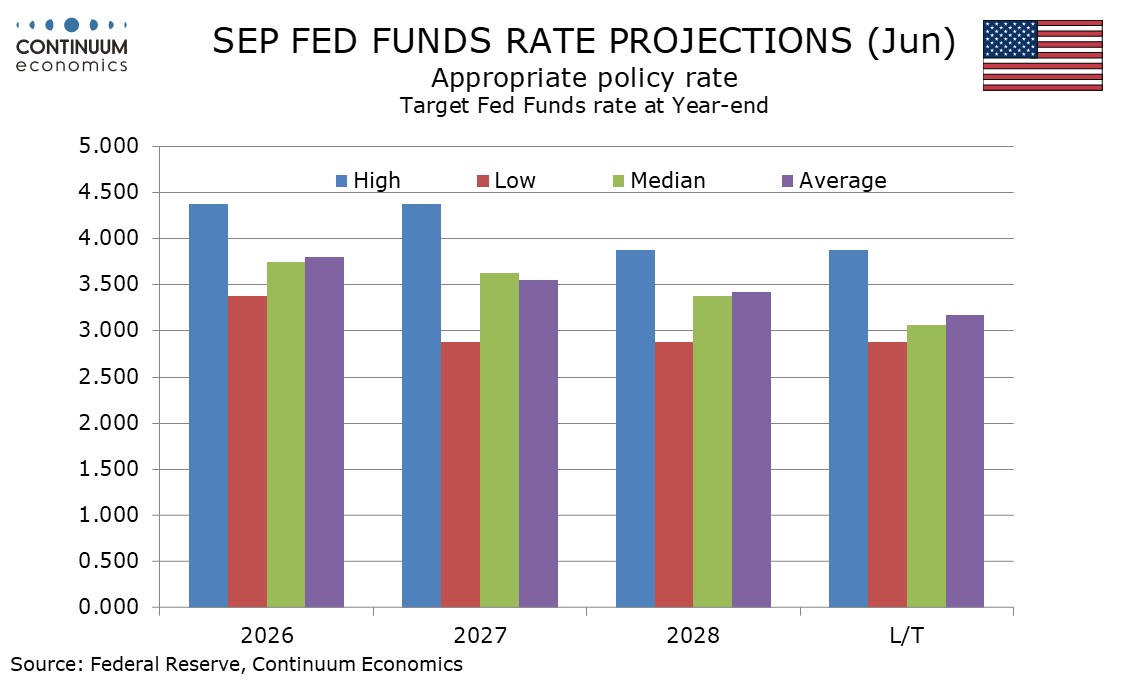

The Fed dots show a clearly divided Fed with only a minority on the median rates view for 2026, for a 25bps hike, 2027, which sees a 25bps reversal, and 2027, which sees a further 25bps easing. There are several respondents on either side of the median but we believe the voters lean towards the dovish side. That suggests that under our view of a softening in data in the second half of the year, a rate hike can still be avoided, with 2027 seeing some easing, though it will be a heated debate at the Fed.

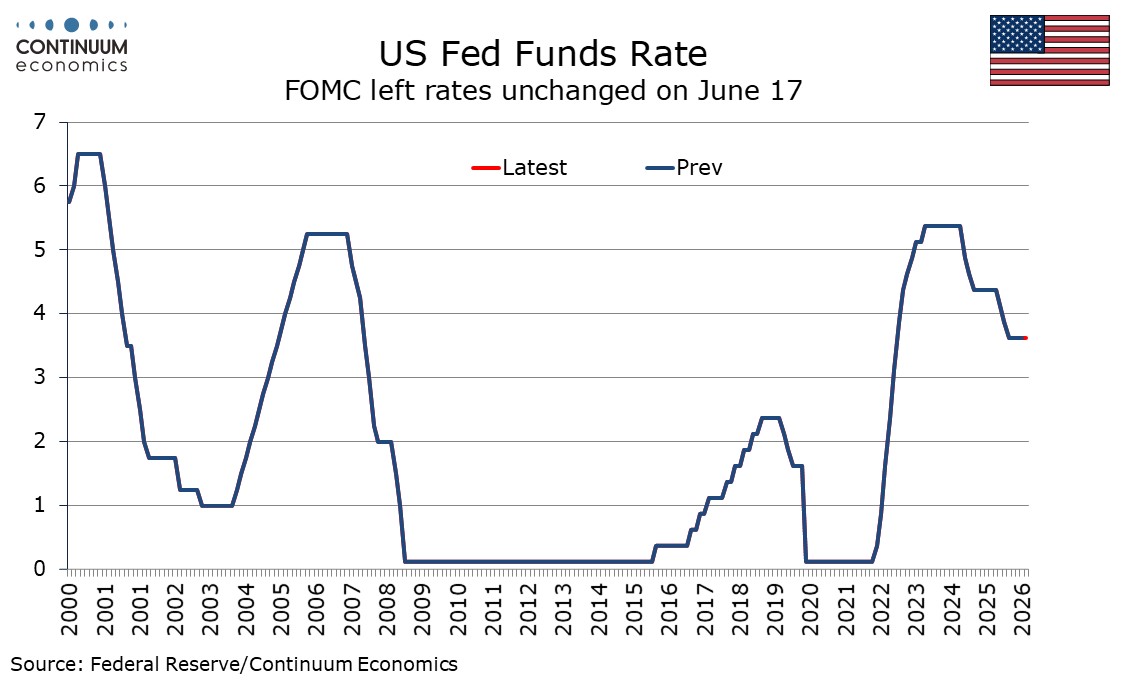

Incoming Chair Kevin Warsh has put his stamp on the statement which offers little forward guidance, which left rates unchanged with a unanimous vote. There was some discussion over whether a likely dropping of an easing bias would be replaced with a neutral one or one for tightening. The lack of forward guidance was confirmed by Warsh as a decision the Fed had taken, and one that he had earlier advocated. It is also somewhat convenient for a clearly divided Fed. Getting a reference to productivity growth and capital investment being strong into the statement is also likely to have been at Warsh’s suggestion. Inflation is described as elevated though in stating this is in part due to supply shocks, including for energy, it is not a particularly hawkish take. Activity is described as expanding at a solid pace despite elevated uncertainty. Job growth as keeping pace with the labor force and unemployment as having changed little.

There are 19 participants in FOMC meetings with 12 voters, but there are only 18 dots for 2026, 2027 and the long term view, and only 17 for 2028. Warsh confirmed that he was the absent dot, and he is probably on the dovish side of the median, despite stressing his commitment to the inflation target in the press conference. The voters are also likely to have a more dovish lean than the median with many non-voting district presidents leaning hawkish. For 2026 only three dots are on the new median for one 25bps hike, and in fact the median is 3.75% rather than 3.875%, technically putting those three on the firm side of the median and suggesting whether the Fed will tighten is a close call. Six are further above, one of them by 50bps. Eight see no rate change this year, and only one is on March’s median seeing a 25bps easing. For 2027 only two are on the median, with a neutral skew, eight above and eight below. 2028 also sees two on the median, with eight above and seven below.

Warsh in his press conference refused to be led into providing forward guidance, and instead focused on the announcement of five major task forces, on communication, the balance sheet (something Warsh has made it clear he wants to cut), data sources, technology and jobs and finally the inflation framework. He did state he was committed to the 2% inflation target until it has been reached, which is crucial for credibility. It is clear that the Warsh Fed will see many changes, and may become one that is harder to forecast given the lack of forward guidance and also what is likely to be a downgrading of the significance of the dots, or even their eventual abandonment.

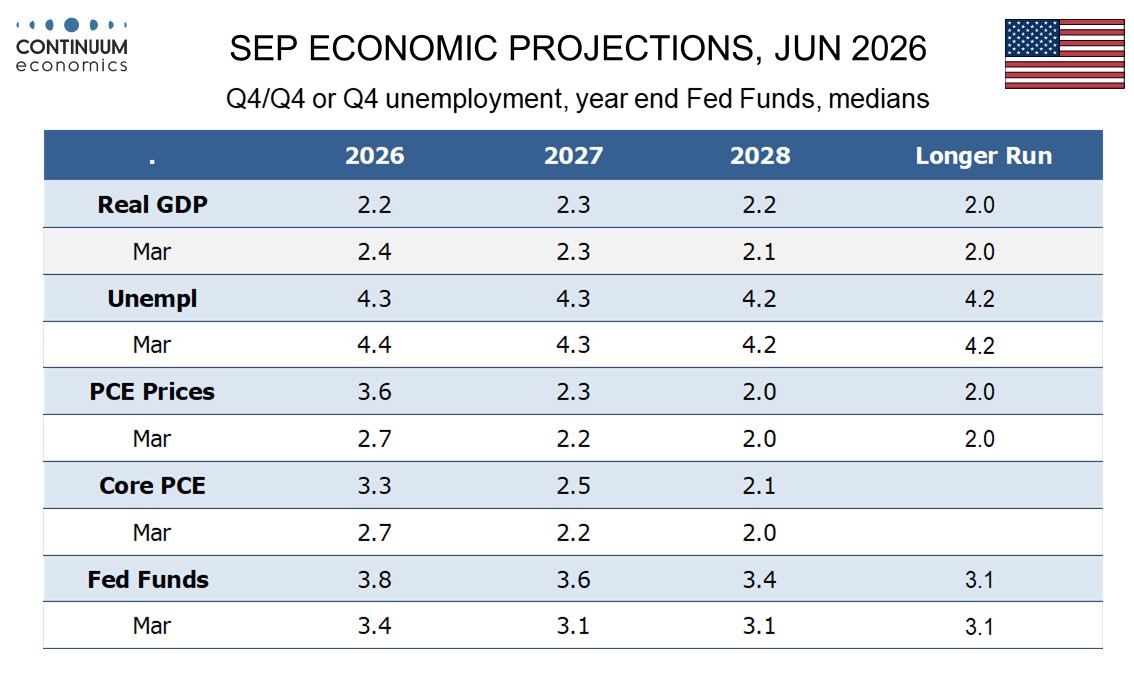

Given all of the above, we would be cautious about predicting Fed policy based on the latest dots. Our view is that the economy is likely to lose momentum in the second half of the year, with consumer spending looking inflated relative real disposable income, though consumers remained surprisingly resilient in May’s retail sales release. Inflation is also likely to lose some momentum if the Middle East peace deal holds. Slowing in the core rate is likely to be slow, though an upgraded forecast of 3.3% for yr/yr core PCE prices in Q4 2026 (from 2.7% in March) may be a touch too high, seeing the pace remaining at April’s. We expect rates to remain on hold until Q2 2027. We expect an easing in that quarter after core inflation sees a significant drop in Q1 as a strong Q1 2026 drops out of the yr/yr comparison. If inflation then stabilizes near target, a second 25bps easing looks plausible in Q3 2027, returning the Fed Funds target to a neutral 3.0-3.25%. A move below neutral however is unlikely without a significant rise in unemployment. We are assuming that the tariff impact on inflation will have faded by 2027. Even if Trump is able to replace the tariffs that the Supreme Court ruled against, the tariff shock will fade from the yr/yr comparison. Our forecast for a more dovish rates trajectory than the median dots is of course data-dependent.