BOE: Gang of 6 and Steady 2026 Rates

Though Megan Greene joined Huw Pill in calling for a one off 25bps risk management hike, 6 MPC members feel that disinflation is showing through and a soft economy and labor market warrants waiting to see energy prices and potential 2nd round effects. This gang of 6 also feels that markets have tightened financial conditions and wage growth are consistent with the inflation target. With the U.S./Iran interim deal this all argues against a 2026 rate hike. Indeed, as further disinflation comes through, we see the MPC consensus becoming dovish again and delivering 50-75bps of 2027 rate cuts.

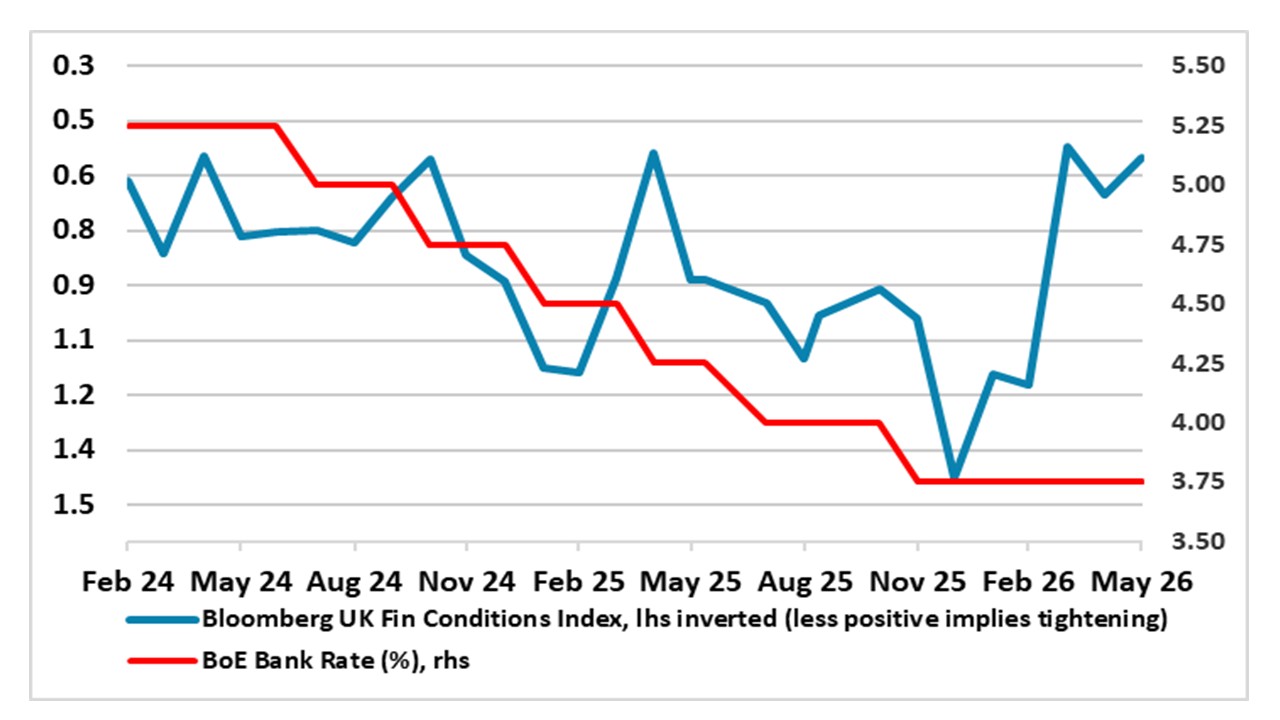

Figure 1: Official Rate Level Far From the Whole Story

Source: BoE, Bloomberg, CE

The MPC minutes show that 6 MPC members take the view that recent data outturns provided some further evidence that underlying disinflation had been on track pre-conflict. Secondly, that upside risks to energy prices had receded, although they remained higher than pre-war. Finally, that the higher interest rates facing households and businesses were already acting to reduce inflation over time and therefore a hold in Bank Rate at this meeting was appropriate. This all suggests that the gang of 6 are not for hiking in the coming meetings (Catherine Mann was between the two camps, but did not join Greene/Pill in calling for a rate hike). Splits in the individual MPC member statements remain evident and around the three scenarios that the BoE is now projections all based on modest hiking of around 50 bp over the coming year in the April monetary report. Even so, BOE governor Bailey showed only a mild tightening bias, though could fade by the time of the new forecasts scenarios in the July monetary policy report.

It is also notable that Governor Bailey has recently referenced the approach of the BoE in 2011, which kept rates on hold even as UK energy inflation soared to 20%, citing its mandate to tolerate deviations from target in a bid to avoid unnecessary harm to the economy and jobs. A BoE survey of senior executives released of late offered tentative support for Bailey’s implicit wait-and-see approach (or what he prefers is an ‘active hold’), with evidence that companies will resist inflation-fuelling pressure from workers for higher wages in response to the current crisis. The expected price growth reading in the regular BoE-compiled Decision Makers Survey is among the weakest since 2022 and we would also point to pay growth already broadly consistent with the BoE’s inflation target. The survey also showed expectations for employment growth remaining in clear negative territory. All of which adds to a picture of a UK economic backdrop vastly and increasingly different to four years ago.

Given ever tighter financial conditions, we still see at least two and probably three more 25 bp rate cuts ahead but now deferred to starting no sooner than Q1 2027 and then extending through 2027 (a moderate probability exists that the 1st cut could be Q4 2026). As for the three scenarios (A seeing energy prices follow market thinking while C sees not only higher energy costs but more persistently too) we are puzzled that the combination of the energy shock and more restrictive policy not only fails to deliver any kind of recession even in the most severe scenario but that all three outcomes see little variation in the growth outlook – i.e. just 0.1 ppt per year between each outlook. We await the new July 30 forecasts.