Preview: Due June 5 - U.S. May Employment (Non-Farm Payrolls) - Slightly slower but still healthy

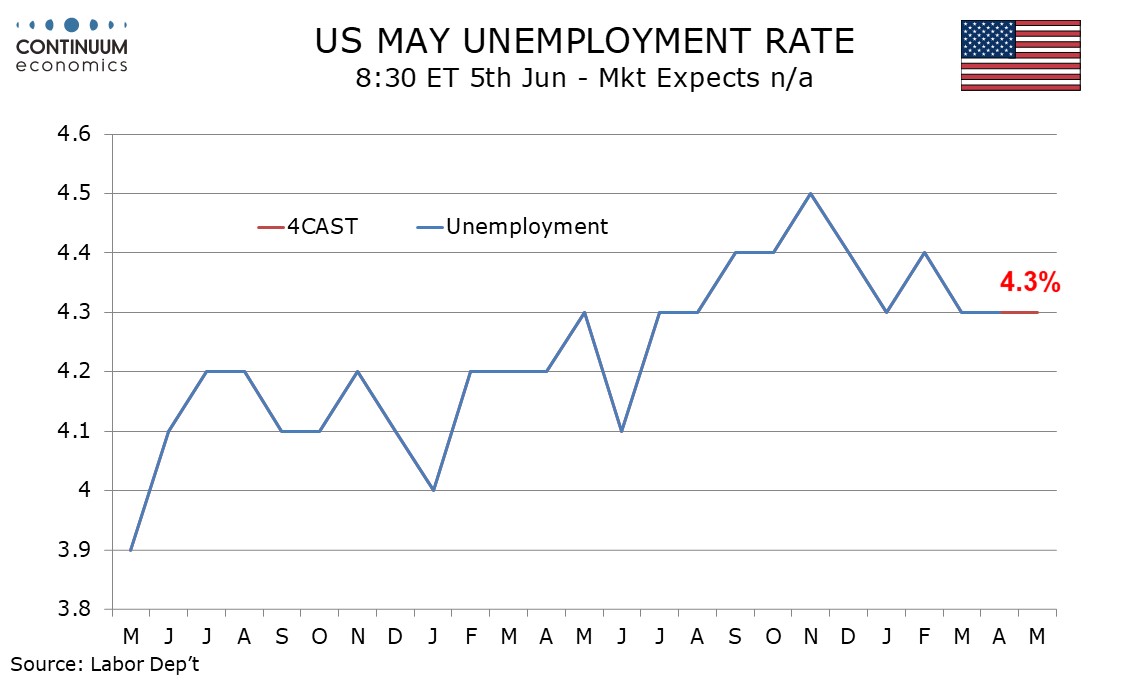

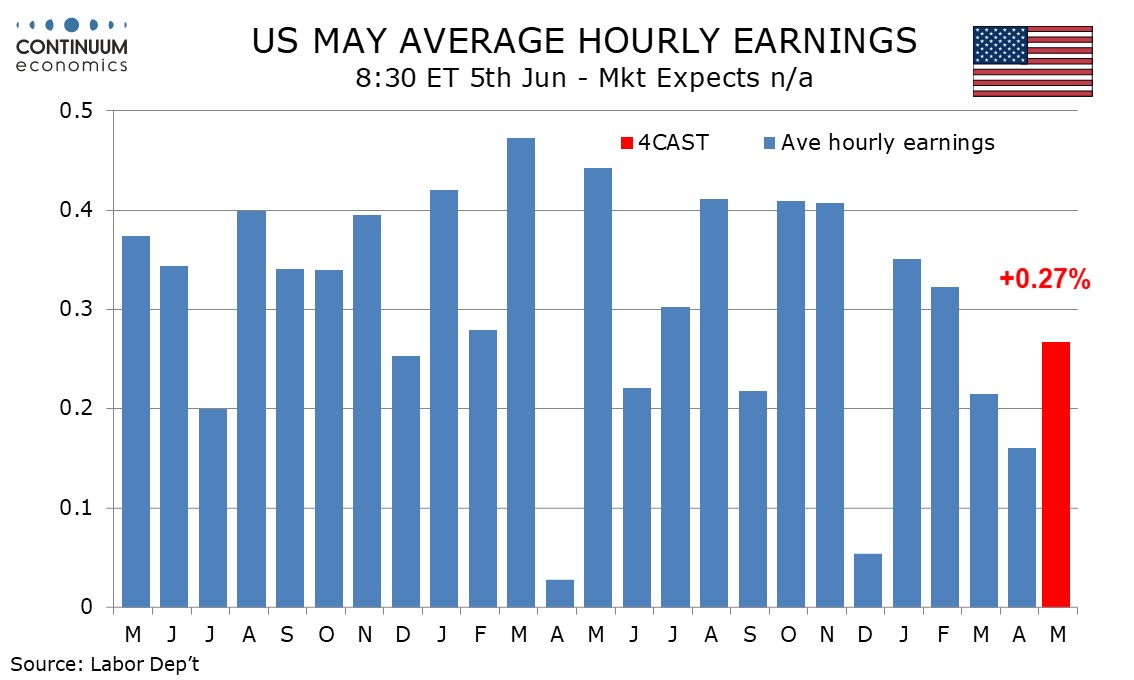

We expect May’s non-farm payroll to rise by 85k overall and by 90k in the private sector, less strong than in March and April but still showing a healthy labor market given a lack of growth in the labor force, leaving unemployment at 4.3% for a third straight month. We expect a 0.3% rise in in average hourly earnings, slightly firmer than two preceding gains of 0.2%.

A rise of 85k would still be stronger than April’s 3-month average of 48k and its 6-month average of 55k. For the private sector the 3-month average is 55k and the 6-month average 68k, with trend in government getting less negative now that the DOGE cuts are done.

March data was inflated by a rebound from a February decline that was depressed by bad weather and a strike in health care, and this rebound may have been extended into April. Weather is likely to be fairly neutral for May.

Initial claims suggest upside risk in May’s payroll, with the 4-week average depressed by two very low weeks. By the time of May's payroll survey week, claims had returned to trend, though were still low. Continued claims are not giving such a strong signal of upside risk.

The main downside risk we see in May by sector is trade, transport and utilities, where we expect a modest decline of 10k after two straight gains totaling over 100k. Retail is likely to lose some momentum as consumers are restrained by high gasoline prices. The closure of Spirit Airlines, causing 17k in job losses, will make it hard for transport to match March and April strength, which was led by couriers and messengers in a bounce from a weak February.

We expect most of a 60k increase in private services to come from education and health at 50k, and that largely in health. Information and finance are now trending negatively, possibly due to increased usage of AI. We expect a 30k rise in goods employment with improvement in manufacturing and construction while mining may get a lift from high energy prices.

We expect the labor force to be unchanged after two straight declines but this will fall short of employment, and see unemployment fall to 4.28% from 4.34% before rounding. We expect participation to fall before rounding, to 61.79% from 61.82%, but still rounding to 61.8%.

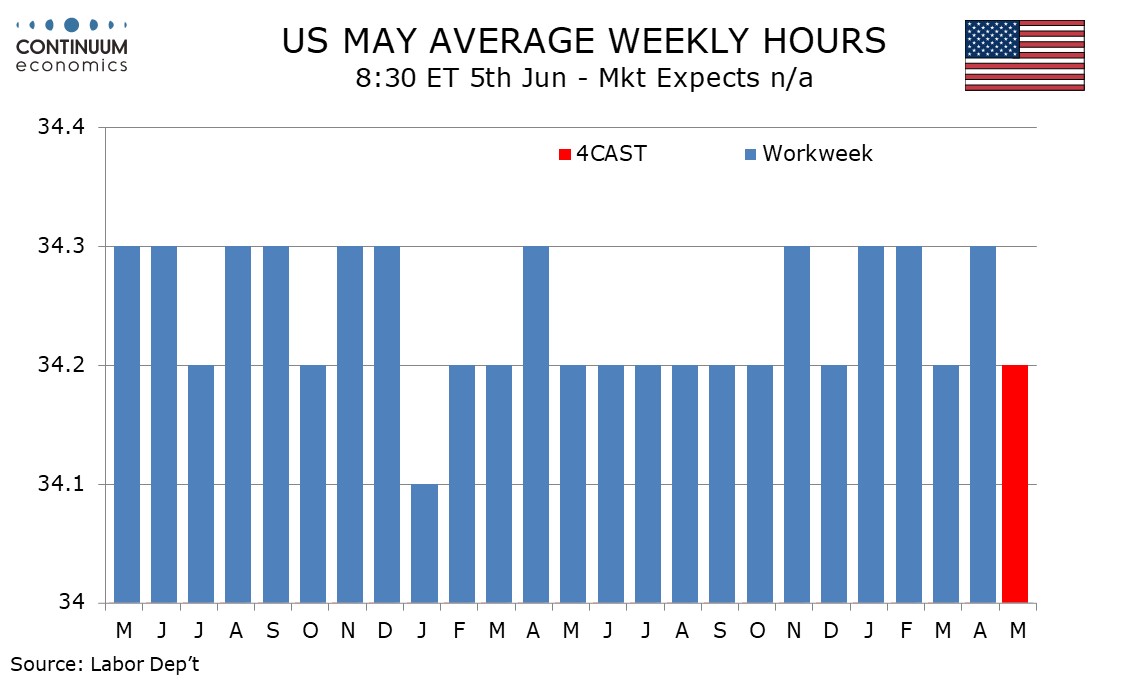

In the last six months the workweek has seen four at 34.3 and only two at 34.2, which is where it was in the six months to October, thus suggesting improvement in the economic picture since then. However risk for May is for a slippage back to 34.2, reversing a rise to 34.3 in April, as higher energy prices start to bite.

Average hourly earnings are showing signs of losing momentum, with the last two months seeing gains of only 0.2%, though a 3.6% April yr/yr rate implies a trend of 0.3%. For May we expect a stronger rise of 0.27% before rounding, though that would see yr/yr growth slip to 3.4%, matching March’s outcome that was the lowest since May 2021.